Swedroe: Don’t Underestimate Emerging Markets

Your portfolio could miss out on added returns if you do.

Thirty years ago, emerging markets made up about 1% of world equity market capitalization and just 18% of GDP. As such, there was a very limited ability to invest in emerging markets—the few funds that were available were high cost, actively managed funds.

Today, the world looks very different. Emerging markets represent about 13% of global equity capitalization and more than half of the global GDP. And the costs of obtaining exposure to emerging markets has significantly decreased. For example, the expense ratio of Vanguard’s Emerging Markets Stock Index Fund (VWO) is just 0.14%.

Yet despite representing about one-eighth of global equity market capitalization, the vast majority of investors have much smaller allocations (they dramatically underweight) to emerging market stocks. The underweighting often is a result of two mistakes. The first, and most prominent, is the well-known home country bias, which causes investors all around the globe to confuse familiar investments with safe investments.

Unfortunately, Lake Wobegon exists only in fiction. It cannot be that every developed country is safer than the others. Compounding the problem, investors tend to believe that not only is their home country a safer place to invest, but that it will produce higher returns, defying the basic financial concept that risk and expected return are related.

The second mistake is that investors are subject to recency—allowing more recent returns to dominate their decision-making. From 2008 through 2016, the S&P 500 Index returned 7.1% per year, providing a total return of 85.5%.

During the same period, the MSCI Emerging Markets Index lost 1.3% a year, providing a total return of -11.3%. It managed to underperform the S&P 500 Index by 8.4 percentage points per year and posted a total return underperformance gap of 96.8 percentage points.

Compounding the problem was that not only were investors earning much lower returns from emerging market stocks but that they were experiencing much greater volatility. While the annual standard deviation of the S&P 500 Index was about 16% per year, that of the MSCI Emerging Markets Index was about 24% per year. Not exactly a great combination—lower returns with 50% greater volatility. What’s to like?

Investors’ Self-Destructive Tendencies

Unfortunately, it’s well-documented that individuals have a strong tendency to invest in a manner destructive to their returns. The illustration below depicts the difference between “convex” and “concave” investing behavior.

While investors know that buying high and selling low isn’t a good strategy, the research shows that individual investors tend to buy after periods of strong performance (when valuations are higher and expected returns are thus lower) and sell after periods of poor performance (when valuations are lower and expected returns are thus higher). Research has found this destructive behavior has led to investors underperforming the very funds in which they invest.

Further compounding the problem is that investors tend to have short memories. For example, it wasn’t long ago that investors were piling into emerging market equities due to their strong performance.

For the five-year period 2003 through 2007, while the S&P 500 Index provided a total return of 83%, the MSCI Emerging Markets Index returned 391% and Dimensional Fund Advisors’ (DFA) Emerging Market Value Fund (DFEVX) returned 546%. (Full disclosure: My firm, Buckingham Strategic Wealth, recommends DFA funds in constructing client portfolios.) How quickly investors forget!

Current Valuations And Expected Returns

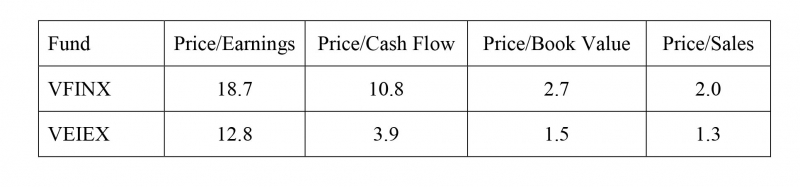

The best predictors we have of future returns are current valuations. With that in mind, the table below provides the valuation metrics of Vanguard’s 500 Index Investor (VFINX) and its Emerging Markets Index Fund (VEIEX). Data is from Morningstar as of Jan. 31, 2017.

As you can see, regardless of which value metric we look at, U.S. valuations are now much higher than emerging market valuations. Now, it’s important to understand that doesn’t make international investments a better choice. Their higher valuations simply reflect the fact that investors view the U.S. as a safer place to invest. And as you know, there’s an inverse relationship between risk and expected returns (at least there should be).

Looking Forward: Expected Returns

To estimate future real expected returns, a common method used by financial economists (as opposed to the crystal ball method used by “gurus”) is the earnings yield, or E/P, the inverse of the more commonly used price-to-earnings (P/E) ratio. The E/P produces an expected real return for U.S. stocks of about 5.3% compared with an expected real return for emerging market stocks of 7.8%.

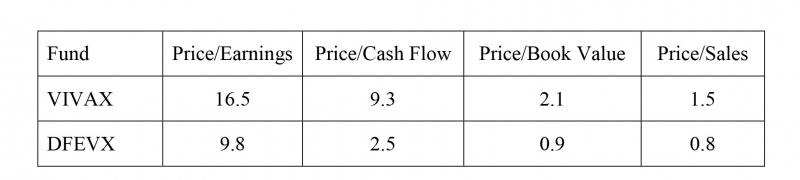

For value investors, the case for emerging market investing is even more compelling. The table below shows the same metrics for Vanguard’s Value Index Fund (VIVAX) and DFA’s Emerging Markets Value Fund (DFEVX).

Shiller’s CAPE 10

Another commonly used metric to forecast returns is the Shiller cyclically adjusted price-to-earnings, or CAPE 10, ratio. This metric uses the last 10 years of earnings and adjusts them for cumulative inflation. The S&P 500 Index currently has a CAPE 10 of about 29.2, producing an earnings yield of 3.4%. At year-end 2016, the CAPE 10 for the emerging markets was just 12.5, producing an earnings yield of 8.0%.

We’ll pick up this discussion later in the week by looking at the importance of book-to-market ratio with a new study from Michael Keppler and Peter Encinosa, and making a case for global diversification.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.