Best Of 2016: Swedroe On The Mystery Of Vanishing Premiums

Make sure your portfolio has factor diversification.

[Editor's Note: We are rerunning some of our best stories of the year.]

Given that it’s been both well-documented and well-known that value stocks—in particular small value stocks—have provided higher returns for investors over time, it’s no surprise that as director of research for The BAM Alliance, I’ve been getting a lot of questions about the disappearance of the value premium.

The following table shows the returns of five value and five blend funds from the same major asset classes (large and small stocks from the U.S., developed and emerging markets). The funds are managed by Dimensional Fund Advisors (DFA) and the data covers the 10-year period ending Feb. 11, 2016. Using these funds allows us to view the returns of live funds, which include costs, as opposed to looking at index returns. (Full disclosure: My firm, Buckingham, recommends DFA funds in constructing client portfolios.)

As you can see, in terms of annualized returns, an equal-weighted portfolio of the five value funds underperformed an equal-weighted portfolio of the five blend funds by 0.9 percentage points per year for the last 10 years. And as further evidence, for the 10 years, from 2006 through 2015, the annual average global value premium was -1.4%, while the annual average U.S. value premium was -1.5%. This type of underperformance comes as a surprise to many investors given the longer-term evidence.

A Long-Term View

The following table provides annualized returns for various equity classes over the 89-year period of 1927 through 2015 It shows why the lack of a value premium over the recent 10-year period might catch many investors off guard and cause them to question their asset allocation decision. The data is based on the Fama-French Indexes.

Despite disappointing recent results, investors who know their financial history understand that the underperformance of value stocks for the last 10-year period, while perhaps not “expected” (meaning it wasn’t the most likely outcome), shouldn’t have been “unexpected” either (meaning there was a reasonable chance this outcome was going to happen).

Consider the following evidence when we break down the full 89-year period into 17-consecutive (nonoverlapping) five-year periods from 1927 through 2011:

- Small value stocks outperformed large growth stocks in 11, or 64%, of those periods.

- Small value stocks outperformed the S&P 500 Index in 10, or 59%, of those periods.

- Small value stocks outperformed small growth stocks in 10, or 59%, of those periods.

While there was persistence in outperformance, overall, approximately 40% of the five-year periods saw underperformance for small value stocks. Unfortunately, too few investors are willing and able to stay disciplined over such periods and adhere to their long-term financial plan.

Looking At Large-Caps

We will now turn to the data comparing the returns of large value stocks to large growth stocks and the S&P 500 Index. Large value stocks outperformed large growth stocks and the S&P 500 Index in 10—or 59%—of the 17 five-year periods. Note that whenever large value stocks outperformed large growth stocks, they also outperformed the S&P 500 Index. The reverse was also true.

In addition, the data provides us with eight nonoverlapping, 10-year periods that we can examine:

- Small value stocks outperformed large growth stocks in seven of the eight periods. The only exception was for the period 1987 through 1996, when small value underperformed by 0.31% per year.

- Small value stocks outperformed the S&P 500 Index in all eight periods.

- Small value stocks outperformed small growth stocks in all eight periods.

- Large value stocks outperformed large growth stocks in six of the eight periods, or 75% of the time.

- Large value stocks outperformed the S&P 500 Index in six of the eight periods, or 75% of the time. Large value underperformed once, and there was one tie (from 1987 through 1996, when they both returned 15.29% per year).

Even these high rates of persistence demonstrate it’s still possible you could wait out a 10-year investment horizon and have a chance that small and large value stocks won’t outperform other asset classes. If there was no possibility of this occurring, then there wouldn’t be any risk in allocating to value over growth. Knowledgeable investors shouldn’t be surprised that we’ve just experienced a 10-year period when value stocks didn’t outperform growth stocks.

The Probability Of Underperformance

With this in mind, my colleague, Jared Kizer, examined the likelihood of underperformance across various time horizons for the equity, size, value and momentum premiums. He begins with a demonstration of the observed historical, mean and standard deviation measures for each premium.

The data in the table above contains everything necessary to calculate probabilities of underperformance over any horizon for each of the four premiums. Of course, this all depends upon a normal distribution assumption, which is reasonable for multi-annual returns data because annual returns data is approximately normally distributed for diversified portfolios (and certainly factor portfolios meet the diversification requirement).

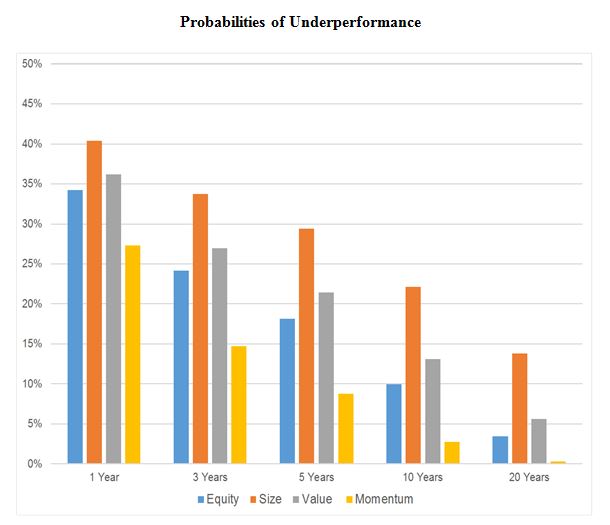

The graph below reports the probability of factor returns below zero for each of the four factor premiums over the one-year, three-year, five-year, 10-year and 20-year time horizons:

The graph above shows that the probabilities of underperformance are significant and positive all the way out to five years. And even beyond five years, three of the four premiums have a greater than 10% chance of underperforming over a 10-year horizon.

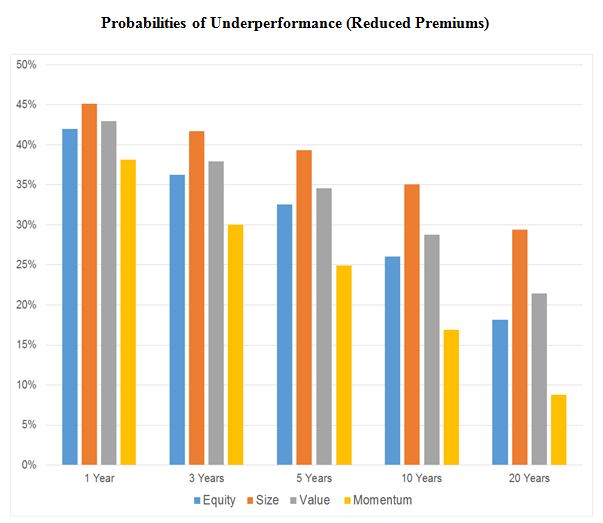

Kizer then looked at the same data, but cut his estimates regarding the size of each premium in half. He kept the volatilities the same. This is reasonable to look at, since one could argue all of these premiums may be lower in the future than they have been in the past due to post-publication effects (and various other considerations, like trading costs and investment management expenses). His results are shown in the graph below.

Here there is a significant jump in the probabilities of underperformance. Out to five years, there are now roughly 25%-plus probabilities of underperformance. At the 10-year horizon, the probabilities are all in excess of 15%. While some could certainly argue that a 50% reduction in each premium is severe, this nevertheless illustrates how sensitive the probabilities are to the assumed size of each premium.

Role Of Diversification

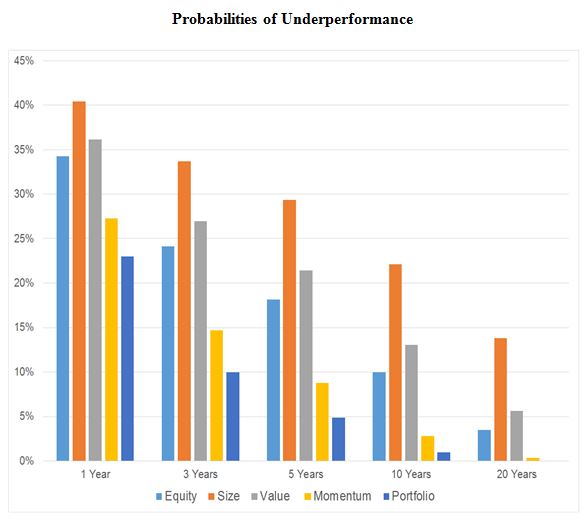

Finally, Kizer examined the importance of diversification in helping to limit the probability of underperformance. As a rough illustration, he built a portfolio allocated 25% to each of the four premiums, then replicated the probability of underperformance from his first graph (keeping the size of each premium at its historical value).

As you can observe in the graph above, diversification across each of the four factors greatly reduces the probability of underperformance, which perhaps is not surprising given the low correlation across each of these factor premiums.

The evidence presented does make a strong case for diversifying across the various investment factors that have been shown to explain the vast majority of the differences in returns of diversified portfolios. Each of these factors is supported by evidence that is:

- Persistent—across long periods of time and various economic regimes.

- Pervasive—holds across countries, regions, sectors and even asset classes.

- Robust—holds for various definitions (for example, there’s a value premium whether we measure value by price-to-book, earnings, cash flow or sales).

- Investable—holds up not just on paper, but also after considering trading costs.

- Intuitive—there are logical risk-based (economic) or behavioral-based explanations for the premium and why it should continue to exist.

- Not subsumed by other well-known factors.

My almost 20 years of experience as a financial advisor has taught me that even the most disciplined investors can have their patience sorely tested by as little as even a few years of underperformance, let alone a 10-year period without higher returns for value (or small, or international, or emerging market) stocks.

A dramatic example of the potential for underperformance, or what’s referred to as negative tracking error, is the five-year period ending in 1999. During that time, small value stocks underperformed the S&P 500 Index—which returned 28.6%—by 13.8 percentage points, as Fama-French small value stocks, ex-utilities, returned 14.8%. The longest period when small value stocks underperformed the S&P 500, at least based on calendar years, was the 19-year period 1984 through 2002, when small value stocks returned 12.1% versus the 12.2% return of S&P 500 Index.

No Regrets!

Given the above, those who know their investment history certainly shouldn’t then be surprised when we have a 10-year period without outperformance. Such periods, however, create risk for investors who fall prey to a dreaded disease known as “tracking error regret.” These are investors who regret their decision to maintain a portfolio that performs differently than the market. Tracking error regret causes many investors to abandon their well-thought-out, long-term plans.

As a footnote, for the 15-year period ending Feb. 11, 2016, the DFA Small Value Fund (DFSVX) returned 8.5% per year and outperformed the Vanguard 500 Index Fund (VFINX), which returned 4.2% per year, by 4.3 percentage points per year. That’s called positive tracking error. And I’ve yet to hear an investor complain about positive tracking error.

Of course, the likelihood of periods, even very long ones, of negative tracking error is the price you must pay to earn above-market returns in the long term. And that’s why so few individual investors actually earn the premiums available. They don’t have the discipline to stay the course. Their greatest enemy tends to be themselves.

One of my favorite expressions is that diversification is the only free lunch in investing, so you might as well eat as much of it as you can. But to enjoy the benefits of diversification, you must be patient. Warren Buffett, for instance, has stated his favorite time frame for investing is forever.

If you aren’t patient and disciplined, you are likely to catch that tracking error disease and abandon your plan. It’s that stop-and-start approach to investing that dooms many investors to poor returns. Though they own stocks, they often end up with bondlike returns.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.