## [# VOO Nears Record, TLT Jumps as Powell Hints at September Fed Cut](/sections/features/voo-nears-record-tlt-jumps-powell-hints-september-fed-cut)

# VOO Nears Record, TLT Jumps as Powell Hints at September Fed Cut

Stocks and bonds surged Friday after Fed Chair Jerome Powell hinted the central bank may cut rates at the September FOMC meeting.

[](/authors/sumit-roy)

[By Sumit Roy ](/authors/sumit-roy)

Aug 22, 2025

Edited by: ETF.com Staff

[ + Follow ](/etf/login)

Share Email LinkedIn Facebook X (Twitter)

googletag.cmd.push(function() {

googletag.display('js-dfp-tag-article_page_302x26');

});

Loading

U.S. stocks and bonds rallied Friday after Federal Reserve Chair Jerome Powell signaled that the central bank may be prepared to cut interest rates as soon as next month.

The [**iShares 20+ Year Treasury Bond ETF (TLT)**](/tlt) rose 0.7%, while the [**Vanguard S&P 500 ETF (VOO)**](/voo) jumped 1.5% on the back of Powell’s remark that “the shifting balance of risks may warrant adjusting our policy stance.”

The S&P 500 finished around 6,467, just a hair below its all-time high of 6,469 set on Aug. 14. The [**Invesco QQQ Trust (QQQ)**](/qqq), which tracks the Nasdaq-100, also added 1.5% on the day and sits roughly 1.5% below its own record from last week.

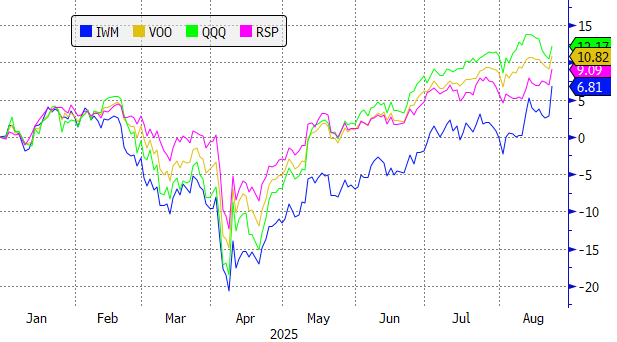

While the rally was broad-based, smaller companies led the charge. The [**iShares Russell 2000 ETF (IWM)**](/iwm) surged 3.9%, while the [**Invesco S&P 500 Equal Weight ETF (RSP)**](/rsp), which reduces the influence of mega-cap tech stocks by weighting all S&P 500 companies equally, climbed 2%.

Year to date, VOO is up 11%, QQQ 12%, RSP 9% and IWM 7%.

## Futures Show Little Change

Fed funds futures now imply an 85% probability of a rate cut at the September policy meeting, up from 75% a day earlier but right in line with where it was a week ago.

That limited shift in expectations helps explain why the bond market’s reaction was more muted than stocks’. Treasury yields for the 2-year, 10-year, and 30-year maturities remain stuck in the same ranges they’ve traded in for much of the year, and the ETFs that hold them—TLT, the [**iShares 7-10 Year Treasury Bond ETF (IEF)**](/ief), and the [**iShares 1-3 Year Treasury Bond ETF (SHY)**](/shy)—have also stayed rangebound.

Stock investors, however, seized on Powell’s words as a green light, using them as an excuse to bid prices higher on hopes that easier monetary policy is finally around the corner.

googletag.cmd.push(function() {

googletag.display('js-dfp-tag-in_article_unit');

});

## A Measured Powell

Still, Powell himself struck a more cautious tone than the price action suggested. His Jackson Hole speech emphasized the elevated uncertainty facing the U.S. economy, shaped by multiple forces.

Among them are “significantly higher tariffs,” “tighter immigration policy that has led to an abrupt slowdown in labor force growth,” and “changes in tax, spending and regulatory policies” from the federal government. These, he noted, make it difficult to disentangle what’s structural and what’s cyclical.

“Monetary policy can work to stabilize cyclical fluctuations but can do little to alter structural changes,” Powell said.

He acknowledged the steep slowdown in the labor market reflected in recent jobs reports. But rather than a simple weakening in demand, Powell highlighted how both supply and demand for labor have slowed in tandem.

With labor supply softening, lower payroll numbers are to be expected, he explained.

“Labor supply has softened in line with demand, sharply lowering the breakeven rate of job creation needed to hold the unemployment rate constant,” he said.

That dynamic, Powell warned, is precarious.

“This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.”

## Tariffs & Inflation Uncertainty

On the inflation front, Powell struck a similar note of caution. He pointed out that tariff effects are now plainly visible in consumer prices.

“The effects of tariffs on consumer prices are now clearly visible. We expect those effects to accumulate over coming months, with high uncertainty about timing and amounts. The question that matters for monetary policy is whether these price increases are likely to materially raise the risk of an ongoing inflation problem.”

The Fed’s base case is that tariff-driven inflation will be relatively short-lived—a one-time upward adjustment in price levels rather than a persistent trend. But Powell admitted that isn’t guaranteed.

“It is also possible…that the upward pressure on prices from tariffs could spur a more lasting inflation dynamic, and that is a risk to be assessed and managed.”

## Walking The Tightrope

Powell summed up the Fed’s dilemma by stating that in the near term, risks to inflation tilt to the upside, while risks to employment tilt to the downside. That tension puts the Fed in a difficult spot, forcing it to move cautiously as the outlook evolves.

“Our policy rate is now 100 basis points closer to neutral than it was a year ago \[after the rate cuts in 2024\], and the stability of the unemployment rate and other labor market measures allows us to proceed carefully as we consider changes to our policy stance," Powell explained.

He reiterated that monetary policy is not on a preset course and that every decision will depend on the incoming data and its implications for the outlook.

Nonetheless, "with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance,” Powell said.

## Market Outlook

Put together, Powell’s comments reinforced the idea that the Fed could cut rates next month. But they fell well short of a dramatic policy pivot.

Markets are currently pricing in two cuts for the remainder of the year—one in September and another in December—but without much conviction. Inflation uncertainty lingers, and Powell’s tone was careful, not dovish.

For equity investors, though, that was good enough. Friday’s surge reflects a market eager to embrace any hint of easing, even if Powell himself is still weighing risks on both sides of the mandate.

[ + Follow ](/etf/login)

[ Sumit Roy Senior ETF Analyst ](/authors/sumit-roy)

Sumit Roy is the senior ETF analyst for etf.com and author of (Don't) Invest Like a Pro. He creates a variety of content for the platform, including… [View Bio](/authors/sumit-roy)

Related Topics [Fixed Income](http://www.etf.com/topics/fixed-income)

[Bond](http://www.etf.com/topics/bond)

[Equity](http://www.etf.com/topics/equity)