## [# ETFs 2025: Cheap, Fat, Starving for Attention](/sections/conferences/etfs-2025-cheap-fat-starving-attention)

# ETFs 2025: Cheap, Fat, Starving for Attention

At FutureProof two weeks ago, I gave a brief summary of the state of the ETF industry. Be careful out there.

[](/contributors/dave-nadig)

[By Dave Nadig ](/contributors/dave-nadig)

Sep 22, 2025

Edited by: ETF.com Staff

[ + Follow ](/etf/login)

Share Email LinkedIn Facebook X (Twitter)

googletag.cmd.push(function() {

googletag.display('js-dfp-tag-article_page_302x26');

});

Loading

let duration = 0, percent = '0', new_percent = '';

jwplayer("etfVideo").setup({

playlist: "https://cdn.jwplayer.com/v2/media/GE9ehEvJ",

aspectratio: "16:9",

autostart: "viewable",

ga: {}

});

jwplayer().on('time', function(e) {

duration = e.duration

if (e.position >= duration * 0.25){

percent = '25';

}

if (e.position >= duration * 0.50){

percent = '50';

}

if (e.position >= duration * 0.75){

percent = '75';

}

if (e.position == duration){

percent = '100';

}

if (new_percent != percent){

// GTM Datalayer - Video Event

dataLayer.push({

'event': 'video',

'video_id': 'GE9ehEvJ',

'video_percent': percent,

'video_url': 'http://www.etf.com/markdownify/node/133178'

});

new_percent = percent;

}

});

Future Proof is an incredible event. 5,000 attendees spread across a half-mile of beach, 50,000 one on one breakthru meetings, and 4 stages of non-stop content. While I spent most of my time in Huntington Beach talking to advisors and ETF issuers, I took 20 minutes to give my honest thoughts on what's really going on in the ETF industry. You can see the whole presentation with transcript [**here**](https://www.etf.com/sections/conferences/dave-nadig-future-proof-video-transcript), but here's the Tl;DR:

- Most ETF assets are in, and will continue to be in, cheap index-based products. This is, in many ways, the ETF's great legacy for all investors: low cost beta.

- Despite that, new products are at such insanely high fees that the big revenue winners are likely not the firms you think of when someone says "ETF" at a cocktail party. Massive profits are being made.

- The incredibly permissive launch environment combined with coming share-class relief suggest we're headed for an even bigger flood of new ETFs than the 600 new funds already launched in 2025.

### Active's Big Year

The story of the year has been the rise of active management, and indeed, 37% of flows this year have been into "active" ETFs.

But when people hear this, they tend to think of stock pickers in the classic mold: someone sitting at around a table with a group of analysts on a Monday morning making hard, human decisions about whether to sell NVDA or buy CAT. But that’s not what the numbers show. Almost all of this giant flow has been in derivative overlays, defined outcome structures, and income engineering.

Most of these funds are often **active in name only** — the real “activity” is in rolling options or resetting exposures, not in hand-selecting securities. For investors, that means the return and tax profile looks nothing like what you’d expect from stock-picking active. No, this is all "non-traditional." It's more like 100-Gecs [Hyperpop](https://open.spotify.com/track/0qMZXgcLfkl5RI3q50KHMH?si=12809abb19364ed2) than the [Rolling Stones](https://open.spotify.com/track/6H3kDe7CGoWYBabAeVWGiD?si=b6e68abf9553455a).

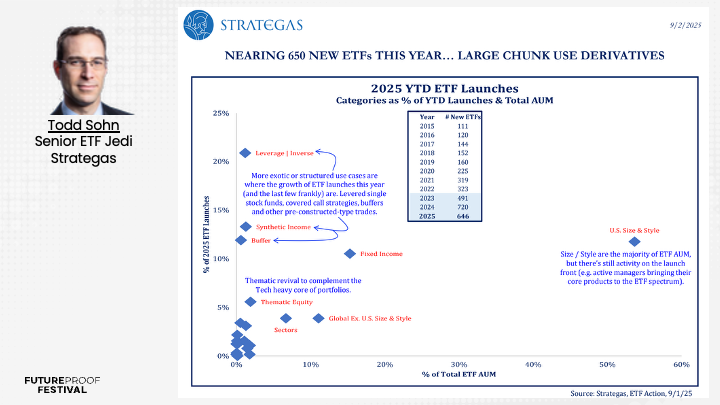

Not only are these responsible for the pseudo-mirage of "active" dominance, these categories also represent nearly all the products launched this year, as Todd Sohn of Strategas pointed out in a recent note:

###

### Cheap still wins ...

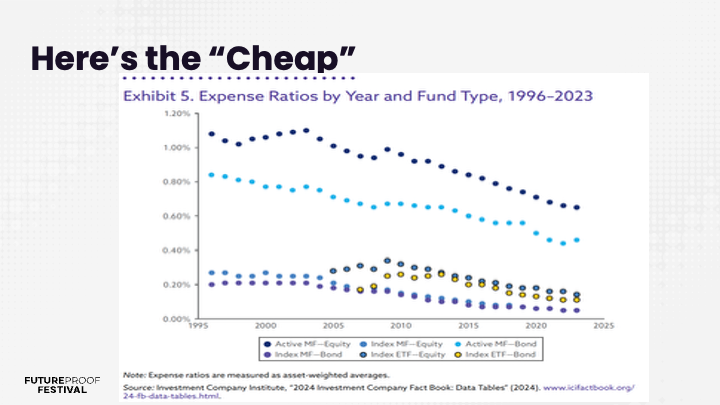

Despite all the "innovation," in these sexy non-traditional categories, "Cheap" remains the key insight for actual end investors. The bulk of actual new money still flows to broad, ultra-low-cost beta (even if less than it used to). Sub-10 basis points wins the day, every day. That’s great for investors, but it leaves issuers gasping for margin in traditional categories. Even in fixed income — where fees ticked up slightly post-pandemic — the gravitational pull is down. Scale and distribution matter more than ever.

Click any heading in that chart, and you'll see the same story told over and over: The bulk of the flows, and the bulk of the assets still live in the the cheapest buckets, no matter how many expensive products the industry launches. And this is part of the endless slide in fees Morningstar has been documenting across ETFs and Mutual Funds for decades:

### ... but the Goose is Getting Fat

Yes, asset weighted fees are really low, and while the bottom may be in (see how the active bond MF line is kicking back up), that doesn't mean that the industry is going to roll over and just take all this efficiency lying down.

If you shift the lens from flows to **flow revenue** — assets multiplied by fees — the picture looks very different. This is what issuers actually care about -- making money. Nobody *really* keeps score with AUM, because the "product mix" is so important. All those funds on the right hand side of this chart may not have the assets of the funds on the left, but since they charge 10 times more, they don't need to. That's why, just in August, super-expensive >1% product generated about $60m in annualized fee from new assets. And if you really dig under the hood, you find it's just a small handful of firms actually making all the money:

The synthetic income folks:

... and the defined outcome/buffered folks.

Between First Trust (the VEST defined outcome series), Innovator, JP Morgan and Toroso (who's behind YieldMax), just four firms are generating over $1 billion in annualized fees on fairly cookie-cutter options-based products. That's a lot of fees.

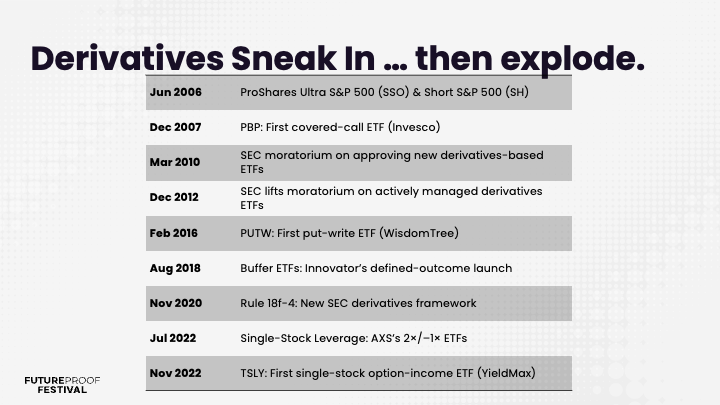

This is the new normal. Derivatives can provide genuine, useful molding of your pattern of returns, but it's also been a gravy train for the industry since the rules loosened up in the last few years.

## What Now? The Battle for Your Attention

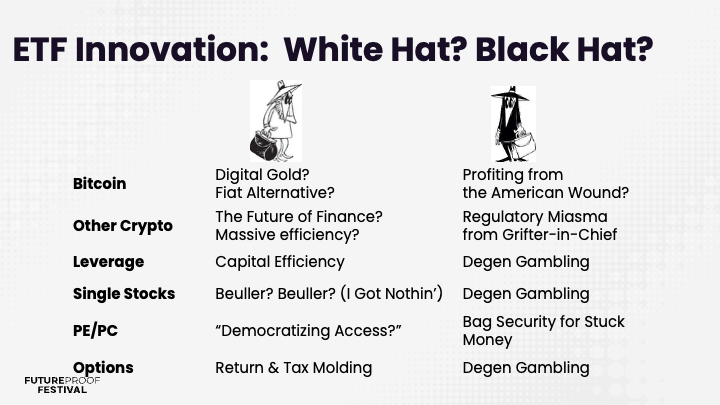

The problem with ETFs is that they've been too successful. ETFs aren't just a regulatory structure, they're an entire platform, like a cell phone. And all platforms demand attention, even if they've reached their apotheosis. The "ETFs Won" problem is made worse by a radical deregulatory environment being bulldozed by a huge shift in individual investor behavior towards products we would have called "gambling" just a few years ago.

What this means is, mostly, you can't "trust" the ETF structure or an ETF issuer or even the ETF regulators to be on your side. They're not. They're on their side. Your job is now to figure out who's wearing the black hats, and who's wearing the white hats.

It's not that issuers and funds won't be doing what they say they're going to do. If nothing else, the ETF industry is very very good at making products that do precisely what they promise to do -- if you read the prospectuses, SAIs, and supplemental information extremely, excruciatingly carefully. No, the problem is communication, around three particular issues: Leverage, Income, and private markets.

### Leverage: Now On Single Stocks!

A quick search through nearly any [related subreddit](https://www.reddit.com/r/MSTR/comments/1gqy218/mstu_leveraged_2x_mstr_questions/) will find you endless examples of folks wondering about charts like this:

That's the 2X levered Microstrategy ETFs printing down over 30% while the stock is up 15%, thanks to the magic of volatility drag! If you've been reading ETF.com a while, you'll know we write the same "[your leverage ETF is wonky](https://www.etf.com/sections/etf-basics/leveraged-inverse-etfs-why-2x-isnt-2x-you-think)" article on a nearly annual basis. Doesn't matter. People still don't get it, and flood the reddits with complaints about how all these funds are broken.

### Options Income! Now with Quantum Tax Treatments!

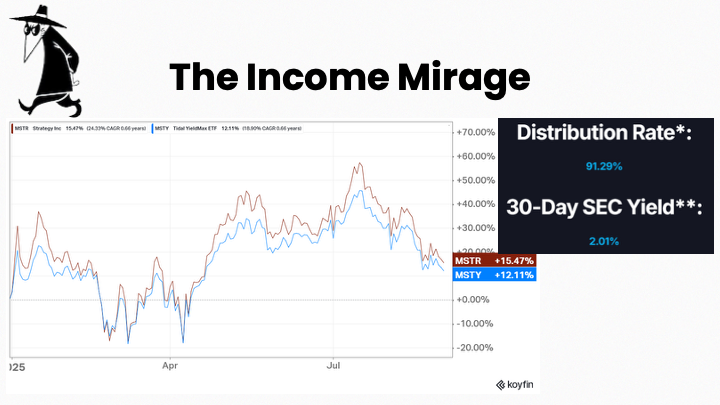

THe leverage folks have nothing on the new raft of single-stock and narrow-pooled income strategies. Most of these products work the same way -- using the options markets to create a synthetic covered call position. This is, to be over simplistic, just selling volatility on very volatile underlyings, and it leads to charts that look like this:

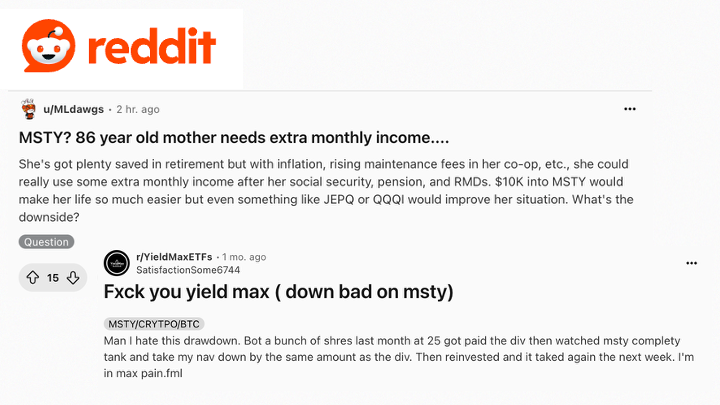

Here we have an extremely popular product, YieldMax's $MSTY. If you're a keen-eyed observer, you might notice that MSTY is trailing MSTR -- the actual stock -- on a total return basis this year. But along the way, you were promised a "distribution rate" of 91%. What that means, in practice, is the fund made massive distributions, degrading its NAV significantly, which, even if you perfectly reinvested with no tax hit, still did worse than the underlying.

These products don't work for most people because the tax treatment is so bad and unpredictable. MSTY holders had absolutely no idea they were going to get 100% income distributed if they held in 2024, because MSTY reported return of capital right up [until 6 days before the 1099s went out](https://www.nadig.com/p/the-tax-problem-with-hyper-income). The misunderstandings about how these types of hyperincome products is so profound there are essentially only two Ur-Posts on reddit about them: those drowned in hopium, and those just mad.

### Labubu Markets: Private Investing

And then there’s private credit, where the race to “democratize” has already pushed issuers to play fast and loose with regulatory edges. My big issue with the push from issuers to sell "private" everything is that none of it is coming with a clear set of pros and cons for investors: it's smoke and mirrors. To me it's very simple: why would you expect the "good" private (Credit/Equity/Real Estate) to end up in a liquid vehicle available to noobs, when the whole point of private credit has been to provide the "good stuff" to rich people who can handle illiquidity, lockups and questionable valuations.

You're right. You shouldn't. You should be enormously skeptical of anyone promising you "access," because 99.99% of the time, what you reall are is exit liquidity for someone else's bags. Not everything belongs in an intraday, millisecond tick trading vehicle. Interval funds are great.

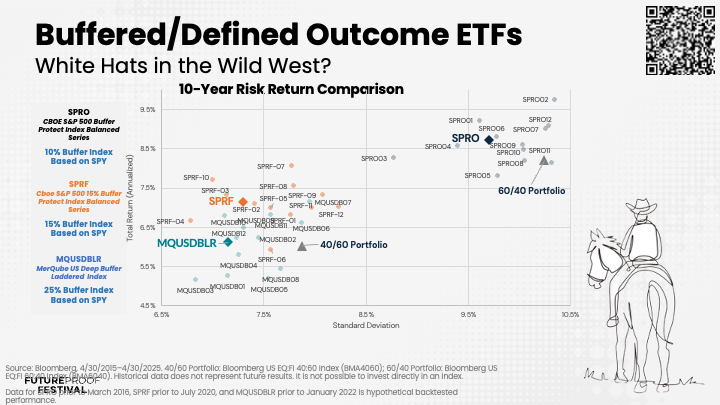

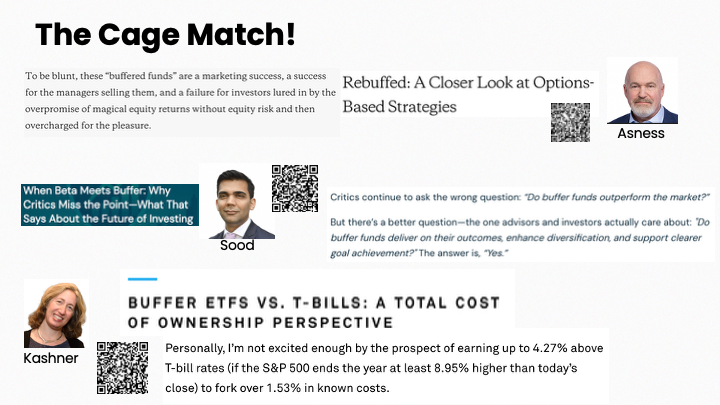

### Buffers: A White Hat in the Wild West?

If there's one piece of this new derivatives pie I can actually kind of get behind, it's buffered or defined outcome products. Whatever we call them, these are funds that take a pattern of returns (like the S&P 500) and through a combination of writing and buying put and call options, change that pattern of returns in a predictable way (usually "selling upside to fund downside-protection").

Mathematically, like most ETFs, these funds do what they say when carefully considered, and help you map out edges of the efficient frontier:

.

But, and this is an important caveat, they aren't magic. All of those transactions create opportunities for slippage, for unexpected expenses, and for, sometimes, middling returns at high fees. That's why AQR, Vest and FactSet all weighed in recently on whether buffers are "good" or "bad."

I'm not going to pick a winner in this fight. Rather, I think they're all right. Yes, buffers are a marketing success that doesn't create magic. But also, I've talked to a lot of real world advisors who use them not for magic-money-math, but for plain psychology. When you have a client who should stay invested but just can't seem to stomach the world, a buffered fund might be the thing that actually keeps them reasonably well exposed. If the alternative is "selling it all for cash" then the buffer earns it's keep as a psychological hack. And if you're a CFA like Elisabeth Kashner? You can probably roll up your own solution just fine and avoid all the fees.

### The Coming Flood & What Gives Me Hives

There's a lot of "innovation" in the ETF market right now. Here's how I'd break it down.

The point here is not to avoid all the new stuff. It's to pay very close attention to what's being promised vs. what's being offered. Bitcoin, Crypto, Leverage, and Options all have legitimate portfolio use cases. Even the private assets stuff can, eventually, be a real thing that's good for investors. But there's a black hat side to almost all of these innovations.

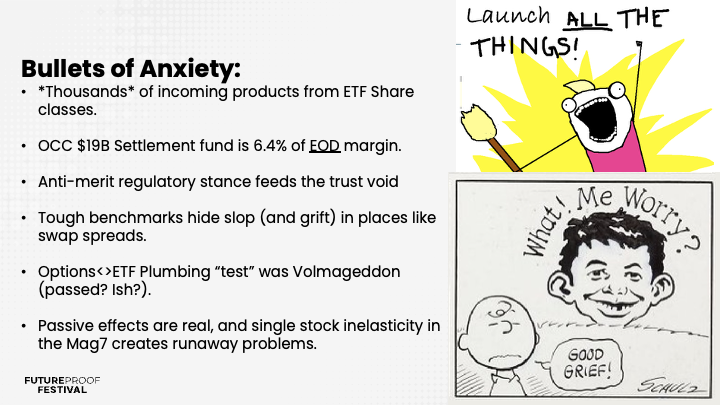

And that's really what I lose the most sleep over: the unintended consequences of all this product proliferation.

Do I have any "real" worries? A few, but they're not enormous (other than the product flood itself!)

- I worry about the amount of money we're running through the options markets -- although the Options Clearing Corporation is, in my humble opinion, the best documented, best regulated, and best run clearing house I've ever done a deep dive on. I have no notes, other than a vague concern about whether $19B is enough to cover two big Chicago firms going down intraday (instead of after the close).

- I worry that our anti-merit regulator is doing everything it can to make the world trust our markets less, not more.

- I worry that the increasing use of opaque swaps and novel structures like Cayman-subsidiaries creates cracks for either errors or malfeasance.

- And I worry a bit about passive effects, which, while very real, and very well discussed in academia now, fail the American marshmallow test for being interesting enough to bother with. The permabulls think I'm just a fearmonger, and the permabears think the [relentless bid](https://thereformedbroker.com/2014/03/05/the-relentless-bid-explained/) is a myth to be disproven and that [passive driven inelasticity](https://www.nber.org/system/files/working_papers/w28967/w28967.pdf) just.. doesn't exist.

But mostly, I worry about the decline of trust. Advisors are in the trust business, and we're in an increasingly trustless world. So, my real advice remains: **Be stingy with your trust, and base it on real human interactions.**

googletag.cmd.push(function() {

googletag.display('js-dfp-tag-in_article_unit');

});

[ + Follow ](/etf/login)

[ Dave Nadig President & Director of Research ](/contributors/dave-nadig)

Prior to becoming chief investment officer and director of research at ETF Trends, Dave Nadig was managing director of etf.com. Previously, he was… [View Bio](/contributors/dave-nadig)

Related Topics [Active Management](http://www.etf.com/topics/active-management)

[ETF.com Videos](http://www.etf.com/topics/videos)