## [# A Smarter Way to Bet Against Volatility?](/sections/features/smarter-way-bet-against-volatility)

# A Smarter Way to Bet Against Volatility?

A new inverse VIX product is delivering solid returns with smaller drawdowns.

[](/authors/sumit-roy)

[By Sumit Roy ](/authors/sumit-roy)

Dec 16, 2025

Edited by: ETF.com Staff

[ + Follow ](/etf/login)

Share Email LinkedIn Facebook X (Twitter)

googletag.cmd.push(function() {

googletag.display('js-dfp-tag-article_page_302x26');

});

Loading

A new exchange-traded product betting against volatility has posted solid gains since its launch, while doing so with noticeably less turbulence than many of its peers.

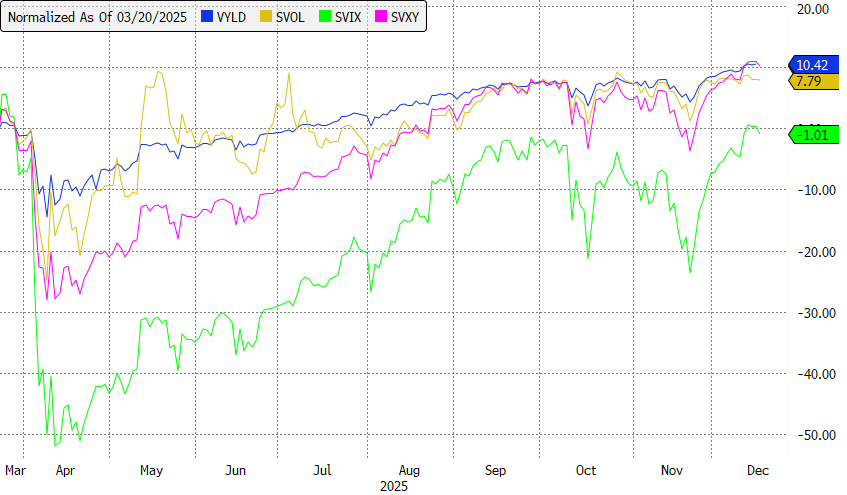

The [**Inverse VIX Short-Term Futures ETN (VYLD)**](/vyld), which launched on March 19, has gained 10.4% since inception. That puts it just in front of the 10.2% return of the [**ProShares Short VIX Short-Term Futures ETF (SVXY)**](/svx) over the same period and ahead of the 7.8% gain for the [**Simplify Volatility Premium ETF (SVOL)**](/svol) and the 1% loss for the [**-1x Short VIX Futures ETF (SVIX)**](/svix).

All of these products are designed to profit when volatility falls. They do this by taking short exposure to VIX futures.

The VIX, often called Wall Street’s “fear gauge,” measures expected volatility in the S&P 500 based on option prices. Over the past 35 years, it has exhibited strong mean reversion, with a long-term average around 19.5 and a median closer to 17.6. When markets are calm and rising, volatility tends to drift lower. When markets sell off, volatility can spike sharply.

Because the VIX itself isn’t investable, volatility products instead rely on VIX futures. Those futures usually trade in contango, meaning longer-dated contracts are more expensive than near-term ones. For investors short VIX futures, that structure can create a steady tailwind as contracts roll down the curve over time.

That dynamic has made short-volatility strategies attractive, but also dangerous. When volatility spikes suddenly, losses can be swift and severe. In 2018, a sharp surge in the VIX led to catastrophic losses in several inverse volatility products in an episode that became known as “Volmageddon.”

In response, newer volatility products have tried to dial back risk in different ways.

## The Different Flavors of Inverse VIX Strategies

SVXY, which has about $227 million in assets under management, provides roughly -0.5x exposure to short-term VIX futures. SVOL, with $648 million in assets, typically runs between -0.2x and -0.3x exposure and supplements its short position with VIX call options designed to help offset losses during extreme volatility spikes.

SVIX, launched in 2022, represents the more traditional approach, with full -1x short exposure to VIX futures. That structure can generate strong returns when volatility is low or falling, but it also comes with significant drawdown risk.

VYLD takes a different path. Rather than targeting percentage changes in VIX futures, VYLD is linked to an index that tracks absolute point moves in short-term VIX futures. Under this structure, a one-point move in VIX futures translates into a 1% move in the index, regardless of the starting level of volatility.

That distinction is significant. A one-point move when the VIX is at 10 represents a 10% change. A one-point move when the VIX is at 50 represents only a 2% change. Percentage-based inverse products respond very differently in those two environments. A points-based approach does not.

The result is that VYLD’s effective exposure adjusts with the level of volatility. When the VIX is low (historically the regime most vulnerable to sudden spikes), the product has less percentage sensitivity to moves in volatility. When the VIX is elevated, and large percentage jumps are less common, its exposure effectively increases.

This adjustment is mechanical, not discretionary. The index rebalances daily, setting its exposure so that each one-point move in VIX futures corresponds to a 1% move in the index for that day.

googletag.cmd.push(function() {

googletag.display('js-dfp-tag-in_article_unit');

});

## Performance During Volatility Spikes

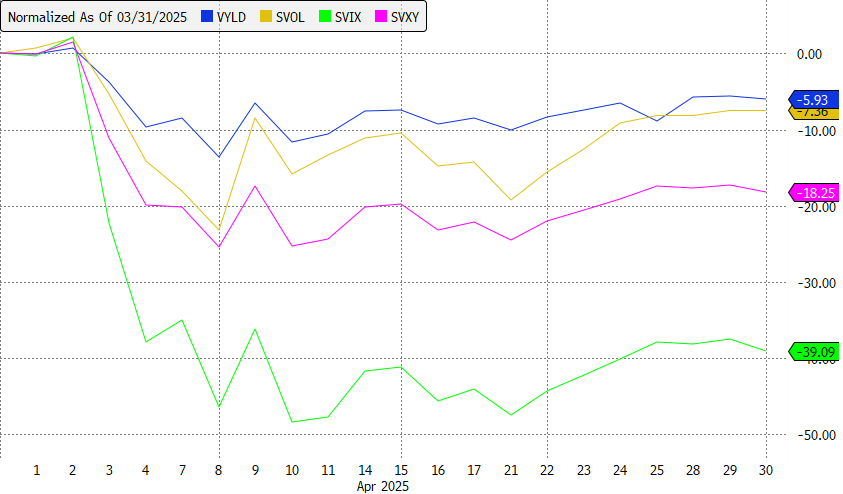

So far, the approach appears to have delivered a smoother ride. In April, when the S&P 500 sold off and the VIX briefly surged above 50, VYLD suffered a maximum drawdown of 13.6%. That compares with peak April drawdowns of 25.4% for SVOL and 25.3% for SVXY. SVIX, with its full -1x exposure, fell as much as 48%.

The trade-off, of course, is return potential. By running lower effective exposure when volatility is subdued, VYLD may capture less of the roll yield that typically benefits short-volatility strategies during extended calm periods. If volatility stays low for a long time, that could translate into relative underperformance.

Still, for investors wary of the sharp drawdowns that have historically plagued inverse VIX products, the points-based approach may offer a more palatable balance between return and risk.

That balance appears to be resonating. Since its launch, VYLD has attracted $111 million in net inflows.

[ + Follow ](/etf/login)

[ Sumit Roy Senior ETF Analyst ](/authors/sumit-roy)

Sumit Roy is the senior ETF analyst for etf.com and author of (Don't) Invest Like a Pro. He creates a variety of content for the platform, including… [View Bio](/authors/sumit-roy)

Related Topics [Volatility](http://www.etf.com/topics/volatility)

[Inverse ETFs](http://www.etf.com/topics/inverse-etfs)

[Inverse](http://www.etf.com/topics/inverse)

[Advisor Center](http://www.etf.com/topics/advisor-center-0)