## [# Word to the Wise: Don't Fear the Securities Lender](/sections/advisor-center/word-wise-dont-fear-securities-lender)

# Word to the Wise: Don't Fear the Securities Lender

People consistently think ETFs loaning out shares to shortsellers is some kind of shady side-business. Nonsense.

[](/contributors/dave-nadig)

[By Dave Nadig ](/contributors/dave-nadig)

May 08, 2026

Edited by: ETF.com Staff

[ + Follow ](/etf/login)

Share Email LinkedIn Facebook X (Twitter)

googletag.cmd.push(function() {

googletag.display('js-dfp-tag-article_page_302x26');

});

Loading

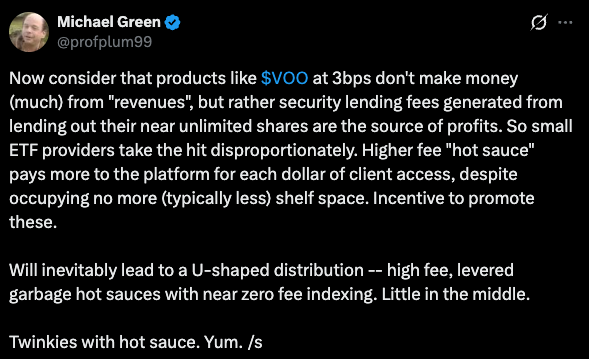

In a completely unrelated tweet-storm about Schwab and Fidelity charging $100 transaction fees on ETFs that won't share revenue with them, Simplify's Mike Green made this comment:

First I want to cede the main point here: Yes, if I have a $100 million fund charging 1%, my revenue is $1 million. If Fidelity want's 15% of that, that's 15bps on the Fidelity assets! If I have a $1 billion index fund charging 10 basis point, my revenue is still $1 million, and Fidelity will still want 15% of that. In that sense the small fund is being "disproportionately" charged based on their AUM -- because they are small and expensive, not large and cheap.

In other words: scale players have an advantage. Of course.

But the part I really can't stomach is the implication that securities lending is a profit center that is somehow more important and larger than the actual investment management revenue, and thus big indexers are shielding their real profits from discussions of revenue sharing. After all, that's at least how *I* interpret "don't make... from revenues, but rather security lending fees”.

### The Rules

Securities lending is quite simple (here's an [old ETF.com explainer from Lara Crigger](https://www.etf.com/sections/news/securities-lending-good-etf-investors)). Everyone wants to short TSLA. An ETF can loan their shares of TSLA to a short seller, who, in return, gives the fund >100% of the value of the borrowed TSLA in cash-or-similar. When the shortseller covers (or the fund just says they want their shares back), they return the collateral to the short seller, and the shortseller returns the TSLA shares.

Why bother? Because that collateral earns a short-term yield — call it 4%. Depending on how badly the short seller wants the TSLA, and how much the fund feels like loaning it out, they negotiate how much of that yield the fund gets to keep, and how much gets paid back to the shortseller. At one extreme, the fund might keep almost nothing, because TSLA is easy to borrow. At the other extreme, the shortseller might have to pay up more than the yield to the fund — a negative rebate.

Because this is obscure back-office stuff, there are [pretty strict rules](https://www.sec.gov/investment/divisionsinvestmentsecurities-lending-open-closed-end-investment-companieshtm), most of which revolve around transparency. Sec lending has to be disclosed (including stuff like who's doing the work and how they're getting paid) in the Statement of Additional Information (SAI), and actual activity has to be reported annually on form N-CEN, monthly on form N-PORT, and on form N-PX for voting.

There are also some guardrails: funds can't loan out more than 1/3 of their securities (ICI reports it's well under 1% industry wide). Collateral has to be at least 102% (105% for international stocks). Everything has to be marked daily, and collateral has to be trued up.

I've been writing about securities lending since the 1990's, and in all that time, the only time securities lending shows up in the news is when someone tries to break these rules. (The most infamous case: the 2023 SEC barring of Sam Masucci from ETF Managers Group, for using [the *promise* of securities lending business](https://www.sec.gov/newsroom/press-releases/2023-144) to extract a $20 million investment from a broker dealer.)

But the actual day-to-day business? Pretty boring.

### The Actual, Non-Twitter Math

So how does this fairly boring "make a little income for the fund" business become a real profit source for an ETF issuer? Well, let's look at some actual numbers.

Let's start with[ **iShares S&P 500 ETF (IVV)**](https://www.etf.com/IVV). I picked this over State Street's [**SPDR S&P 500 ETF Trust (SPY)**](https://www.etf.com/SPY) because SPY is a Unit Investment Trust and not allowed to loan securities at all. I picked it over the [**Vanguard S&P 500 ETF (VOO)**](https://www.etf.com/VOO) because Vanguard's weird mutual structure has its own issues (although the sec lending math ends up being the same). But most importantly, I picked Blackrock because my expereince would suggest they're likely the *very best* at extracting maximum revenue from securities lending.

Here's their 2025 Sec Lending statement, from the [SAI](https://www.sec.gov/Archives/edgar/data/1100663/000119312526114192/d45638d497.htm):

Fiscal year ended March 31, 2025:

IVV Securities Lending ItemAmountGross income from securities lending activities$130,495,222Rebate paid to borrowers$122,600,877***Securities lending income paid to BTC as lending agent******$1,165,357***Cash collateral management expenses not included in BTC lending-agent income$1,021,020Administrative fees$0Indemnification fees$0Other fees$0Aggregate fees/compensation for securities lending activities$124,787,254*Net income from securities lending activities retained by IVV**$5,707,968*All the yield on all the collateral sent over by shortsellers in the year was $130 million. They returned $122 million back to the shortsellers. Net proceeds from all that activity were about $8 million. From that $8 million, IVV — the fund itself — paid Blackrock's lending group (BTC), just over $1 million in fees (in bold).

The net return to IVV shareholders? $5.7 million in net income. What happens to *that* net income? We hop over to the [annual report](https://www.ishares.com/us/literature/annual-financial-statements/afs-j-ishares-core-s-and-p-etfs-03-31-en.pdf) and find:

IVV Statement of Operations ItemAmountDividends - unaffiliated$6,989,596,661Dividends - affiliated$78,639,946Interest - unaffiliated$3,933,010***Securities lending income - affiliated - net******$5,707,968***Foreign taxes withheld$(2,029,661)Total investment income$7,075,847,924***Investment advisory expense******$158,485,881***Interest expense$17,062Total expenses$158,502,943Net investment income$6,917,344,981See it there in bold? The $5.7 million in investment income, alongside the $7 *billion* in dividend income, and $4 million in interest? That's the benefit to IVV shareholders: $5.7 million of the $6.9 billion in investment income.

While that's tiny, some ETFs can make a LOT more money for investors if they happen to have hot and/or hated stocks. Throughout the 2010's, the [**Invesco Solar ETF (TAN)**](https://www.etf.com/TAN), made more than a percent a year in yield loaning out big chunks of the fund. In 2012, securities lending income [was almost 11%](https://www.sec.gov/Archives/edgar/data/1365662/000089180412001400/gug55171-ncsr.htm)!

### The "Profit" Issue

The original tweet that got me so annoyed suggested that the paltry revenue from asset management of big index funds didn't matter, but rather it was the security lending fees from relatively endless shares that generated profits.

So lets run that math. For the IVV example, we know that Blackrock Trust Company (BTC), the Blackrock entity that actually books revenue for Blackrock, Inc., from sec lending made $1.16 million for servicing IVV. That $1 million in revenue is likely not included when Fidelity or Schwab come knocking for a their share of revenue on IVV.

But look back a few paragraphs. See that "Investment advisory expense" in bold? That's what Blackrock Fund Advisors, the Blackrock entity that books revenue for Blackrock, makes from running the fund. $158 million. That's the line item the custodians like Schwab and Fidelity are after. Sec lending is less than a percent of that revenue, which itself is just basis points of the fund.

Of course, Blackrock's BTC does make some real revenue lending juicier funds. Blackrock’s [**iShares Russell 2000 ETF (IWM)**](https://www.etf.com/IWM), has attractive names in it. Last year they [made a net $74 million](https://www.ishares.com/us/literature/annual-financial-statements/afs-j-ishares-russell-top-2000-etfs-03-31-en.pdf) in sec lending for the fund, and paid BTC $17 million to do so. Which sounds like a lot, but again, it's an order of magnitude lower than the $128 million in advisory fees collected. And that's their juiciest big index fund for lending.

### The Point

Why should you care about any of this?

**First:** You should love securities lending and be happy your ETFs participate. It's the equivalent of collecting rent on a second home: you don't need it right now, why not make a little from someone who does? The *vast* majority of the economics go directly to you, the shareholder, not to the issuer or anyone else. The best framing: how much of your fee is being paid for by short-sellers? I mean come on, *it's where the biggest risk takers in price setting -- short sellers -- meet up with risk averse index assets*. How can you not love that there's a market in between them.

**Second:** This is not driving some secret profit line that obviates asset management fees. Blackrock makes $18.4 billion in asset management fees (the part Schwab and Fidelity want a piece of). They make another $700 million from securities lending services (a lot of which comes from specific sec lending programs run for institutions like pensions, not from ETFs). That 3% extra topline revenue isn't altering the negotiation much, and it's certainly not their primary source of profit when their operating margins are 30-40% on asset management. (And most firms can't even keep these revenues in house, instead contracting with a lending agent).

**Third:** Active managers play this game too, this isn't just a Blackrock or Index story. ARK Invest currently covers about 5-10% of fund expenses from sec lending. Baron Partners Fund has historically covered 20%. Being "big" is what matters — that's what gives you inventory to lend!

**Last:** If you're looking to invest in a weird niche, this can matter. TAN is the poster child (their securities lending activity *still* covers about 40% of all expenses). Reading the deep documents sometimes yields gems.

P.S.: If you're inside this process and something here makes you throw a koosh ball at your monitor, reach out. I only ever want to learn!

[ + Follow ](/etf/login)

[ Dave Nadig President & Director of Research ](/contributors/dave-nadig)

Prior to becoming chief investment officer and director of research at ETF Trends, Dave Nadig was managing director of etf.com. Previously, he was… [View Bio](/contributors/dave-nadig)

Related Topics [Equity](http://www.etf.com/topics/equity)

[Advisor Center](http://www.etf.com/topics/advisor-center-0)