Private Credit ETFs 101: “Core Plus”

Wrapping up the exploration of private credit ETFs, Conor MacWilliams breaks down the "Core Plus" category, including its history, potential uses, and possible pitfalls.

This is the final installment of Your Private Credit ETF Crash Course. In this installment we’re going to look at the burgeoning “Core Plus” segment. These are broad market fixed income ETFs that can include allocations to BDCs, private credit CLOs, and direct private loan exposure. That last asset is what we’ll be focusing on as it, along with a public credit sleeve, is what makes these products distinct from the rest of the private credit ETF segment.

We’ll go through what these products are, what direct private loan exposure is, how it gets into an ETF, and a lot of positives and negatives for the segment. We’ll also touch on how there are a few funds adding this private exposure without telling anyone!

Core Plus, Core Adjacent, Core Private?

Let’s do a quick history of Core Plus: this segment of ETFs evolved out of actively managed fixed income mutual funds over the last decade, with mutual fund versions in use for even longer.

The Core Plus thesis entails having broad market fixed income exposure that includes investment grade, high yield, and emerging market debts, along with strong portfolio management. Together these would result in superior risk-adjusted returns over comparable benchmarks like the Bloomberg US Aggregate Bond Index (the Agg).

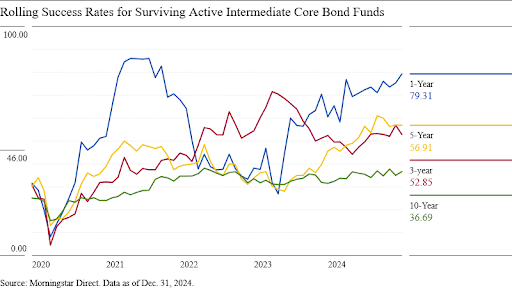

Morningstar has a terrific article that shows active bond fund managers have the highest likelihood to outperform their passive benchmarks. Unsurprisingly, we’ve seen a lot of movement into this space with a number of active mutual funds converting to similar strategies in ETF form, and also the launch of many new funds as well.

We have to obviously caveat a lot of this with an understanding that bond funds have experienced relatively little flows over the last 15 years while the equity bull market stole the show. However, as the credit cycle continues to spin, we’re seeing that equity attention start to broaden out as another generation of investors gets closer to the end of their asset growth period and changes over to a more income-focused portfolio.

So why did I use “Core Plus” instead of just Core Plus at the beginning of this article?

There are a few reasons. The first is that recently a number of funds have launched that incorporate a private credit allocation into the usual Core Plus strategy. I think this fundamentally changes the investment thesis and thus I wouldn’t group them with the rest of the segment.

The second is that, of the products we’re looking at in this space, they fall into two distinct categories:

- Core Plus + Private Credit (Disclosed)

- Core Plus + Private Credit (Undisclosed)

These two categories have incredibly different optics on how they approach private credit. In my opinion, the products in the latter bucket are not being transparent with their investors on how they’re approaching their portfolio construction. There are also other transparency issues with this whole subsegment that I’ll explain that below.

From here on out, we’ll only be discussing the private credit allocations for these products. The rest of the Core Plus portfolios are pretty standard fixed income assets that have been covered extensively.

Core Plus + Private Credit (Disclosed)

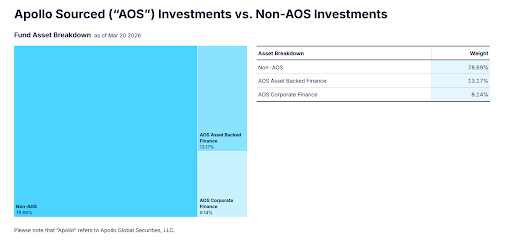

We’ll start with the Core Plus products that are disclosing their private credit exposure. I’ll use the first product to launch as our example: State Street IG Public & Private Credit ETF (ARCX:PRIV), launched in February 2025. The fund aims to hold a portfolio with the following breakdown:

- Public Credit (MBS, U.S. Treasuries, Corporate IG Credit) – 65-90%

- Private Credit (Private credit CLOs, direct private loan exposure, and private funds) – 10-35%

PRIV sources this private credit exposure from an agreement with Apollo Global Securities LLC in which Apollo will provide competitive bids at least 3 times a day for all assets it sources for the portfolio.1 This is what is called a backstop or repurchase agreement and it’s how State Street achieves the feat of getting famously illiquid direct private credit loan access into a continuous liquidity vehicle like an ETF.

Let’s stop here and talk about direct private loan exposure and the role Apollo plays in getting them into the fund’s portfolio. Speaking broadly, the structure of this arrangement mimics what you would see in a traditional private credit fund with a GP/LP (general partner/limited partner) functionality. Apollo is in the role of GP. They originate/source the loans, underwrite them, service them, and provide daily valuations. As I mentioned earlier, they also act as a liquidity backstop. If PRIV is hit by an outflow and needs to rebalance their portfolio, Apollo will repurchase assets (which they classify as AOS Corporate Finance assets) from State Street.

State Street acts as the LP, providing capital and trusting in Apollo to provide high quality capital deployment in addition to their reporting. The loans in PRIV’s portfolio are investment grade2, they range from a recapitalization of Air France/KLM3 to an Intel chip fabrication plant in Ireland4.

This direct private loan access is exactly that. Direct. There are no intermediaries similar to CLOs (One layer removed), BDCs (Two layers removed), or CEFs (One layer removed). This means you are far more exposed to liquidity concerns than you would be in those other exposures. That’s reflected in their nature of their liquidity profile: these are classified as “illiquid” under SEC Rule 22e-45. Having Apollo as a backstop softens that profile a bit but still prevents issuers from having 100% exposure to these assets.

So how does the composition of the portfolio actually breakdown? It fluctuates with market conditions but generally 75-80% of the portfolio is in public credit. The remaining 20-25% is divided into a CLO/ABS portion (“less liquid” assets and thus not subject to the 15% illiquidity barrier) of between 12-18%, along with a constant 8% allocated to direct private loans. This is a sensible amount as it would require assets to halve before the illiquidity barrier is hit and allow State Street to offload positions to Apollo.

Source: PRIV Portfolio as of 3/20/2026

Core Plus + Private Credit (Undisclosed)

Undisclosed? You mean there are funds out there carrying direct private credit loan exposure without disclosing it to their investors?

Yes. There are at least two. If you’d like to do some research for yourself, you can cross reference the existing AOS Corporate Finance assets from PRIV with other funds in the Core Plus space.

Now obviously there are a few issues with this. Having direct private loan exposure without disclosing it as part of your investment portfolio in your prospectus is generally a no-no. These funds do not have any agreement with a fund provider like Apollo to provide a backstop in the event that they need to liquidate their positions. Having tracked the pricing on these assets, I can say that these funds are not changing the marks on their private allocations with any regularity.

The section is meant to be a wakeup call for investors. Be sure to research what you’re investing in! If you’re buying a vanilla Core Plus ETF as a fixed income portion of your portfolio, you’re expecting exactly what the prospectus tells you. Having small percentages of private credit creep in is not what you signed up for! This is bad fund management and shouldn’t be encouraged. The de minimis juice that the manager will potentially get from adding a 1% position in private credit will not only be likely irrelevant but breaks down the trust between investor and fund issuer, which is paramount to the industry as a whole.

Pros and Cons

We’ve gone over the structural components of these “Core Plus” products and identified a few that may need some additional disclosure. Now let’s go over what the positives and negatives of these funds are. Most of them depend on your risk tolerance.

Positives:

- Direct private market access for credit: This is it. You can’t get more direct, you are the LP, you get access to the investment grade portion of the private credit universe that’s usually gated behind high fees, minimum asset requirements, and redemption barriers.

- One size fits all: This can be your entire fixed income allocation. It’s meant to function as a complete basket.

- Yield: Private credit yields more, so having 20-35% of extra juice in a portfolio is likely to boost the risk adjusted return.

- Lower correlation to public markets: I’ll put this as a “feature”, but it does work both ways.

Negatives:

- Liquidity mismatch: ETFs offer daily liquidity while private credit is a long-term liability. These two things will constantly be in tension, especially when you’re dealing with direct private loan access. This leads to the next point.

- Wasted space: These products only have 8% direct private loan access and 12-18% other private credit. That isn’t much. Given the fees (55bp for PRIV), you’re paying quite a premium for the rest of the standard AGG-like portfolio (3bp). These are not building blocks like BDC or private credit CLO ETFs can be. They do not allow any customization based on risk profile.

- Counterparty risk: In cases like PRIV, you are almost entirely dependent on Apollo for everything to do with the private credit portion of the portfolio. While Apollo has proven to be a very capable and disclosure forward partner, there is still real risk associated with having a single partner versus having an array of liquidity partners as you would have with a private credit CLO fund.

- Regulatory uncertainty: These funds are operating in a novel space. Direct private loan access inside of an ETF is a brand-new concept and while the regulators have made some noise about them—mostly related to the fund's original use of Apollo's name in the title, which State Street subsequently removed—we're largely in uncharted territory. If the private markets have a negative cycle, there could be risk of changes.

"Core Plus" At a Glance

And that's it. We’ve covered the whole of the private credit ETF space for now. There may be new innovations and product structures that pop up moving forward and I’ll add to this series if ever it needs updating.

I think private credit ETFs are in a weird space. They are innovative and fun to analyze, but they don’t seem to have found the correct formula to draw major in-flows from investors. PRIV has drawn nearly 700mm in flows so far this year so they may be cracking that code but the total AUM of the segment is still small.

As this space continues to add products, be sure to research the investment thesis along with the current portfolio to make sure they match your risk tolerance.

| Metric | BDC / CEF ETFs | CLO ETFs | Core Plus |

|---|---|---|---|

| Directness of exposure | Two layers removed: ETF → BDC equity → underlying loans | One layer removed: ETF → CLO tranche → loan pool | Direct: ETF → private loan (no intermediary) |

| Liquidity profile | BDC shares trade on exchanges; underlying loans are illiquid but ETF investor isn't exposed to that directly | Senior CLO tranches (AAA/AA) have robust secondary market liquidity; mezzanine is thinner | Public credit sleeve is liquid; direct loans are illiquid (Rule 22e-4), backstop agreement softens but doesn't eliminate the mismatch |

| Transparency | High — BDCs are public companies with SEC filings, quarterly earnings, disclosed portfolios | Moderate — CLO manager reports available but underlying loan-level detail requires digging; marks may lag | Mixed — public sleeve is transparent; private loans rely on originator (Apollo) for daily valuations; some funds in this space are not disclosing private exposure at all |

| Typical ETF fee range | 40 – 75 bps + acquired fund fees (AFFE) from underlying BDC management fees | 20 – 68 bps; No AFFE; CLO management is embedded in tranche pricing | 55 bps (PRIV); Covers both public and private sleeves; high relative to the ~75% that mirrors AGG (3 bps) |

| Counterparty dependency | Low — diversified across many BDC issuers; no single liquidity provider | Low to moderate — diversified across CLO managers; ETF manager selects tranches | High — single originator/backstop (Apollo) for all private credit; no alternative liquidity partners for direct loans |

| Customization / building block | Yes — can be sized and paired with other fixed income allocations to target a specific risk profile | Yes — AAA-only, mezzanine, or broad; multiple products allow granular allocation | No — one-size-fits-all; ~8% direct loan exposure is fixed; not usable as a standalone private credit building block |

| Best suited for | Income-focused investors comfortable with equity-like volatility who want high yield and dividend exposure | Fixed income investors seeking floating-rate yield with controllable credit risk across the capital structure | Investors who want a single-ticket core bond allocation with embedded private credit and are comfortable with the originator relationship |

- https://www.sec.gov/Archives/edgar/data/1516212/000119312525036426/d915332d497k.htm

- https://www.ssga.com/library-content/products/fund-docs/etfs/us/ps/doc-ap-chia-priv.pdf

- https://www.ssga.com/library-content/products/fund-docs/etfs/us/ps/spdr-doc-ap-hermes-priv.pdf

- https://www.ssga.com/library-content/products/fund-docs/etfs/us/ps/spdr-doc-ap-grange-priv.pdf

- https://www.law.cornell.edu/cfr/text/17/270.22e-4