Q1 '26: The State of the (Bonkers) ETF Market

We've entered a new era for the ETF industry, here in the institutional decay phase of the Fourth Turning. Where we once just talked about the growth of the organism, now we wrestle with the mutations.

There's so much going on — in markets, in geopolitics, in America — that it sometimes seems almost a little silly to turn our focus narrowly on the ETF market. Objectively, fee cuts and M&A activity don't matter much to the average investor or advisor when markets are whipsawed double-digits by 4AM social media posts. But it would be a mistake to ignore the challenges facing the ETF industry, if only because the numbers are truly wild.

1. The Big Numbers

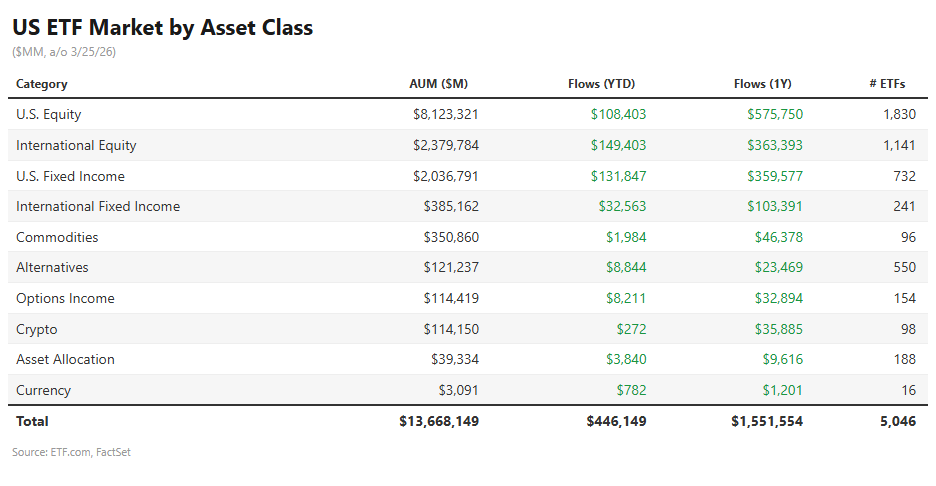

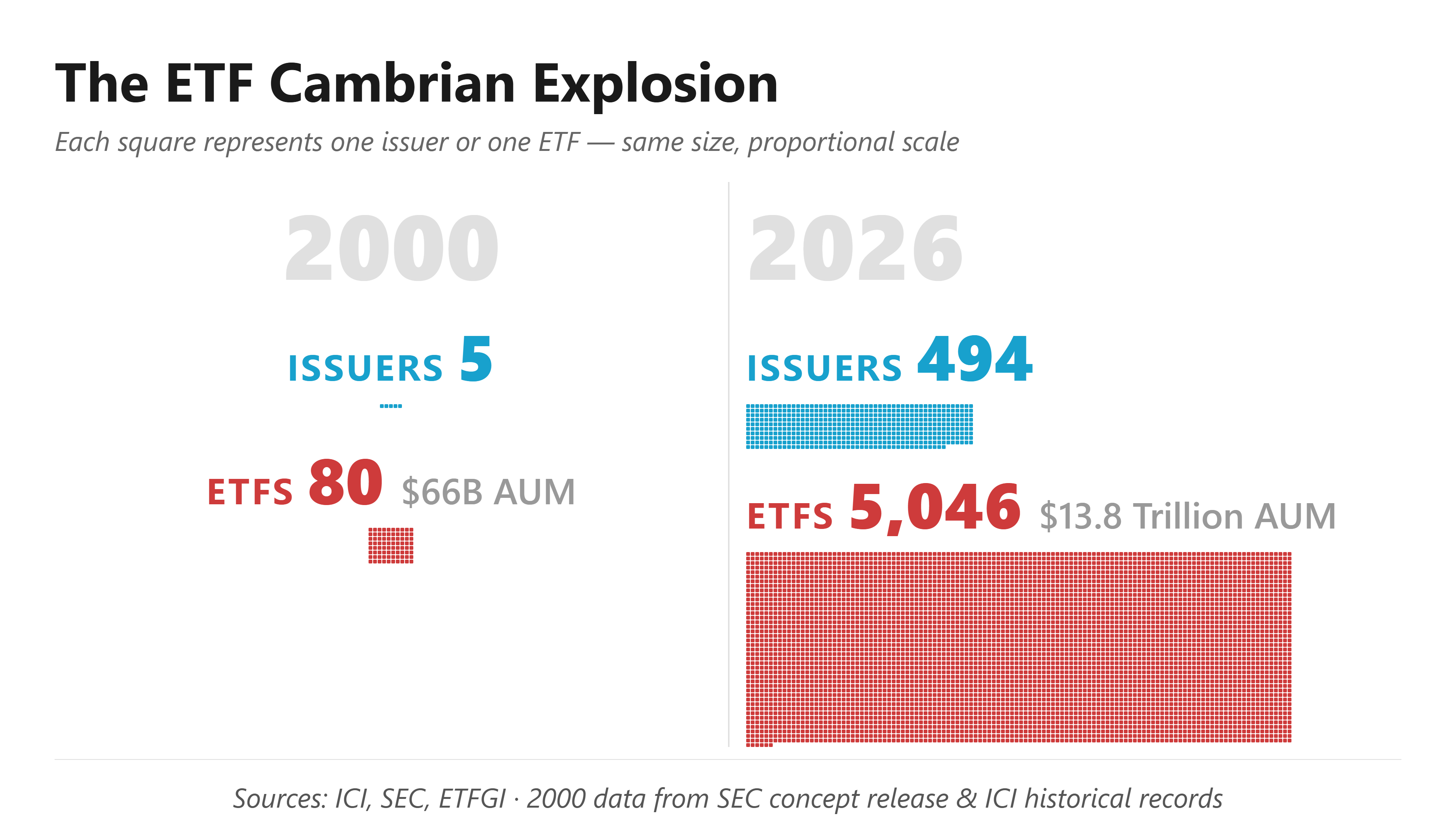

U.S. ETF assets are roughly $13.8 Trillion, now spread across 5,046 funds. (Outside the US, our friends at ETFGI tell us that globally, we've got some $21.24 Trillion in ETF structures.) Vanguard pulls roughly $1.5B per day. VOO alone absorbed $39.3B YTD. The top three issuers (BlackRock, Vanguard, State Street) control 70.2% of U.S. ETF assets.

And the flows are also bonkers! Year-to-date inflows ($446B) are running 64% ahead of 2025's record pace: on track for $2T+, seven years ahead of Bloomberg Intelligence's 2024 forecast for when we might hit that kind of number.

And the trading! ETFs now account for roughly 40% of total U.S. exchange volume, up from a 30% average in 2025 (according to Strategas).

And the launches! 231 new ETFs launched in 2026 so far (pulling $37.2B in assets).

2. The Structural Shift: Share Classes + Active

The share class story is well trod at this point: the Vanguard patent for ETF share classes of traditional mutual funds expired in 2023, and by last December the SEC had granted exemptive relief to over 30 firms. Two weeks ago, on March 17th, the SEC completed the transition to this new era by issuing the final Exchange Act relief for multi-class ETFs.

(That sound you heard was a starting gun.)

About 100 applications are in, about 70 orders issued. 2 firms launched.

F/m Investments actually jumped the line in reverse, launching a mutual fund share class to their TBIL ETF on February 12th. Dimensional followed on March 20th with DFMC, the first actively managed ETF share class, bolted onto a mutual fund they've run since Reagan. Twelve more Dimensional conversions are planned. Fidelity just filed for ETF shares on three mutual funds. You get the picture... there are going to be a lot of new ETF share classes coming to market — perhaps a few hundred by year end, perhaps more. Each one wants your attention and capital.

The implication is existential for the $32 trillion mutual fund industry. Every mutual fund in America can now add an ETF class. Cerulli estimates $15-30B in mutual fund marketing and distribution fees are at risk, because nobody is ever going to be able to justify sticking a client in the Mutual Fund share class unless they have to for structural reasons (like presence in a 401k plan).

"It's not entirely clear how you would justify using a mutual fund share class if an ETF share class is available, when you look at the fees charged, the tax efficiency and the liquidity of the share class." Jennifer Klass, K&L Gates (FT)

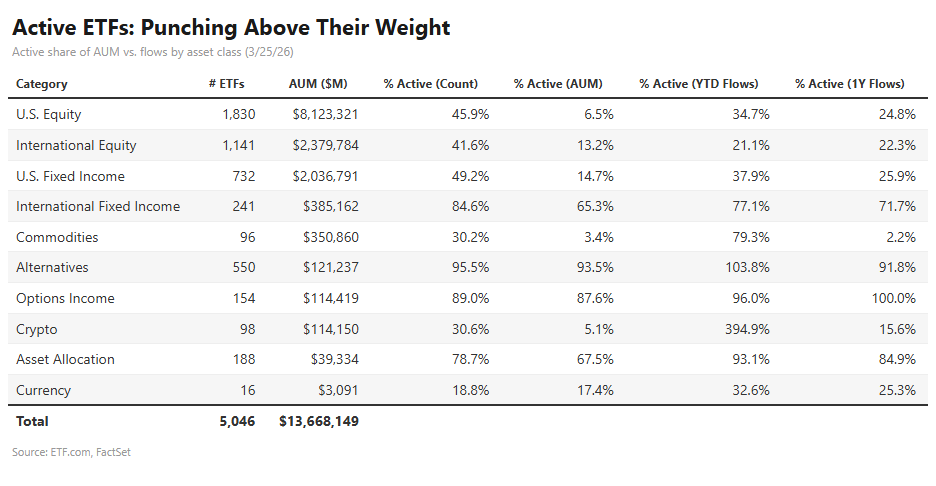

A big part of this flood will be, as with Dimensional, active ETFs. While we could do a lot of splitting hairs on just how "active" a lot of them are, there are indeed now more active than passive ETFs: 2,751 vs. 2,295. 84% of 2026 launches are active, with flows that mirror. Active is gaining assets at 3X its base: 12% of assets but 38% of flows.

But count and AUM only tell half the story:

In U.S. equity, active manages just 6.5% of assets but is capturing 34.7% of YTD flows, more than five times its weight. U.S. fixed income shows a similar pattern: 14.7% of AUM, 37.9% of flows. Options income and alternatives are already active-dominated categories where the shift is essentially complete.

I suspect it's the combo platter of these two ingredients that combines to make the real meal. Share class relief makes the active invasion easier, and quite quickly, the bulk of the activity in ETFs will look nothing like the index funds that built the industry.

3. Macro Means ETFs

Even before the Not-A-War in Iran ("Article 2 Self Defense Operation" being overseen by the newly-named Department of War), we were talking about the "Sell America" trade, and how it had fizzled out.

How times change. Just in the first quarter, international equity ETFs pulled in $149.4B versus $108.4B for U.S. equity, with South Korea (EWY) the standout country bet: +$6.1B YTD and +32.4% return. 85% of non-U.S. MSCI ACWI countries are outperforming the U.S. by an average of 10%. Since Inauguration Day, the S&P 500 ETF ranks 36th of 46 country-specific ETFs, and it's still up 16%!

While I hardly think we're headed for the kind of catastrophe the anti-dollar pundits have been predicting for a year, the core belief system of the market does seem to be shifting. The flows into international have now been big enough, and consistent enough that we can't call it a headline trend, but an actual (if calm) rotation. Of course, with the AI trade in constant flux (Sora+Disney! Sora Cancelled! Memory in crisis! Memory flood!) who can keep up?

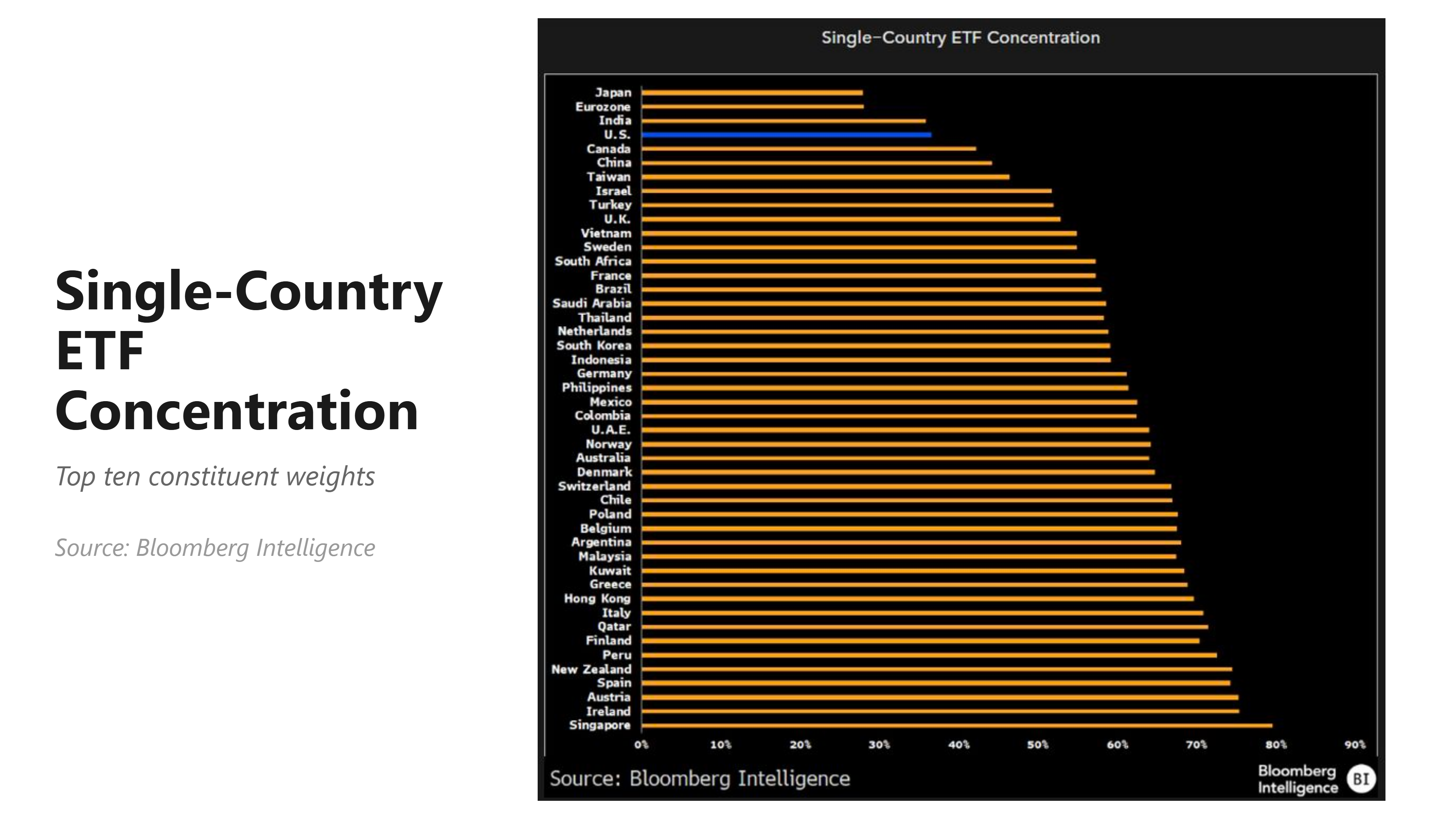

S&P 500 concentration is finally cracking too: Top-10 weight has dropped back below 40% (to ~38.3%). And as the folks at Bloomberg point out: the US is actually less top heavy than most markets anyway:

Outside the S&P: Gold crossed $5,000 in late January while gold ETF AUMs hit a record $701B, backed by Q1 inflows of over $21B . Precious metal ETF daily volume hit $64 billion on January 27 — a single-day record — with SLV briefly displacing SPY as the most-traded ETF. But all that activity doesn't necessarily mean investors got what they expected.

"Investors just got a big-time reminder that gold has zero correlation to stocks, not inversely correlated. Big difference. Good diversifier but unreliable hedge." Eric Balchunas (tweet)

The silver mania was even wilder. In the last week of January, SLV posted $40B in trading volume on Monday, more than all of Q1 2025 combined, hit a record, and by Friday plunged 31% in its worst single-day drop since March 1980 — making it 3X more volatile than Bitcoin for a hot minute.

While nobody particularly enjoys markets like this, the good news is that ETFs — structurally — are crushing it. Note that nowhere in the above description of record breaking chaos is there any mention of broken creates, bad trades or stressed infrastructure. Macro means ETFs now.

4. The Product Zoo

While the big macro building blocks are humming along with high efficiency and incredible liquidity, that doesn't mean the product manufacturers have sat still — far from it. Things have gotten nuttier than they've ever been.

Buffer ETFs:

Goldman acquired Innovator for $2B. For that, they got 159 defined outcome ETFs, with about $28B in AUM. Cerulli projects buffer ETFs could quadruple to $334B by 2030 at a 35% CAGR (Cerulli). Todd Sohn predicts Vanguard launches buffers within 12-18 months.

"Buffer ETFs hit $80B in assets, massively growing. Goldman just bought Innovator for $2B. I've seen breadcrumbs ... Vanguard hired ex-iShares buffer team." Todd Sohn via @TheETFTracker (tweet)

Leveraged & Single-Stock:

While there's a lot of smoke around both of these groups, there's not actually that much heat. There are a total of 549 leveraged + 160 inverse ETF, about 2/3 of which target single stocks. But the total geared AUM is just $132B with about $10B/day volume: as much as gold on a normal day. While there have been the inevitable catastrophes (T-REX 2X UPXI down -99.6% anyone? Defiance 2X HIMS down -98.2%), the more interesting research is on how badly investors do in general chasing performance with levered products. A recent SSRN preprint presented the fun stat that single stock leverage baked in an average 0.79%/month systematic underperformance. And Jeff Ptak at Morningstar ran the numbers a few months ago on 2X Microstrategy ETFs and found that while the funds gained 98% in his sample period, actual investors lost $397M due to terrible timing (a common finding in any hot dot fund.)

My point isn't that these are good or bad funds — they just don't fit in really any rational portfolio context. As Morningstar's Ben Johnson put it:

"How can anyone even think about a retirement crisis now that we've got a filing for CoinShares Bitcoin Volatility Leveraged ETF? Put that in your Monte Carlo simulator and run it." Ben Johnson, Morningstar (tweet)

Private Credit / Private Equity:

Obviously the Private space is hot, and we've written about it extensively, both on the Credit and Equity side. ERShares XOVR has somewhere between 10 and 50% of the fund in a SpaceX SPV we know almost nothing about, but it still seems to get huge inflows and outflows. Demand for private credit assets has been muted given the high profile liquidity issues in some private credit interval funds and BDCs.

Battle lines are being drawn. On the one hand, State Street continues to partner with Apollo to launch Private Credit ETFs. On the other, State Street partner DoubleLine's Jeff Sherman came out recently pretty definitively: "Does private credit work in ETFs? Absolutely not." (Bloomberg).

For most investors, privates of any kind are going to be at most a niche in their portfolio, and one which could likely be filled with something like an interval fund where the liquidity can be better managed. But we'll keep getting new product even if nobody buys it: there's that much push from the asset owners.

Crypto:

By my count we're at 98 crypto ETFs, $114.2B AUM, and a paltry $0.3B in YTD flows, which is frankly incredible given the massive 40% drawdown in Bitcoin. Crypto ETFs went from being a joke to the crypto-native diehards to being the most finely cut of diamond hands. But the product queue is relatively light, and investor interest remains anemic enough to keep it that way in the short term.

Options Income:

While everyone still wants income, and we have over 159 options-income ETFs, it's still a niche. With just $114.4B AUM and $8.2B in 2026 flows, nobody is actually kicking JP Morgan out of their corner booth: JEPI + JEPQ are 68% of category.

Prediction Markets:

3 issuers have filed for prediction market ETFs tied to US Election contracts to be regulated by the CFTC. While I personally find these annoying, I am unworried someone won't understand what they are: gambling-wolves in security-sheep clothing.

5. The Plumbing Renovation

While the bombs drop and the issuer community mostly focuses on degenerate gamblers, the boring infrastructure underneath the ETF market is being rebuilt by a consortium of players, and I'm a fan.

Tokenization (covered a lot last month) is mostly the story, and there are a bunch of cool angles being explored. NYSE is building 24/7 tokenized stock and ETF trading. The DTCC for its part is creating tokenized rails for (eventually) any DTC-held security. Franklin Templeton and Ondo Finance are wrapping ETFs for non-US crypto rails, just to name a few of the dozen projects underway.

At the same time, S&P licensed the S&P 500 to Trade[XYZ] for the first-ever officially approved S&P 500 perpetual futures contract on a DeFi exchange, and ProShares jumped on the cash-management bandwagon with their Genius Act compliant money market fund, IQMM (part of a wave of issuers realizing they can roll their cash desks into products).

And while all this is going on, Texas is launching an exchange and Schwab's back to charging platform fees.

Honestly, except for Schwab, all of these are positive developments. I remain particularly excited by the DTCC's work, as it's where, eventually, the rubber has to meet the road. No amount of shenanigans in "wrapping" TSLA stock inside crypto is real tokenization.

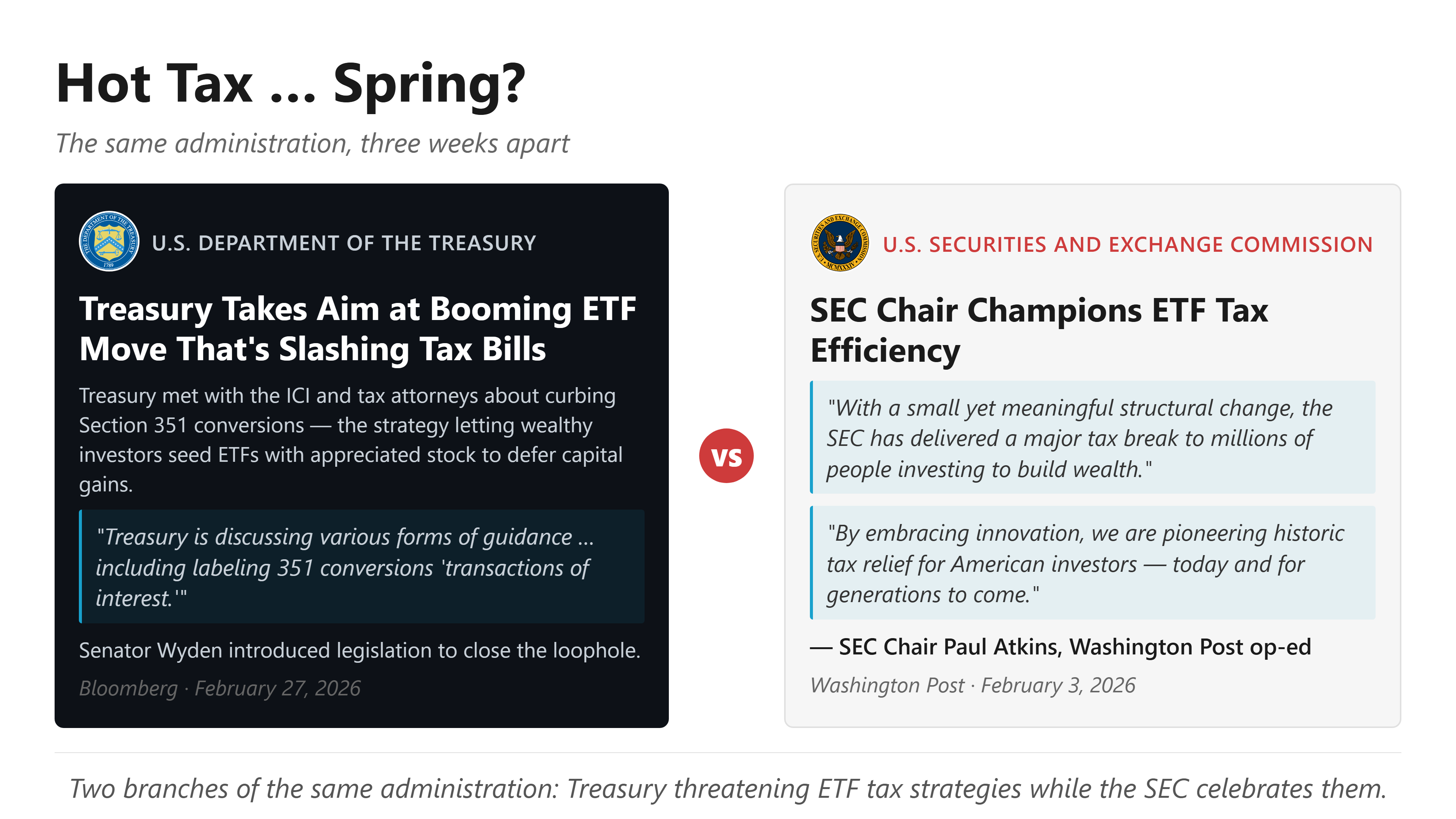

6. Hot Tax ... Spring?

The ETF's greatest structural advantage (tax efficiency) is both under attack and more in focus than ever before. Most of the focus is on "351 transfers" where rich folks use their low-basis portfolios of concentrated positions to seed a "new" ETF, thus getting diversification and potentially the benefits of ETF tax deferral through in kind creation/redemption in the resulting new fund. Some 60 or so of these 351 ETFs have been seeded this way since 2022, the largest of which was seeded with almost $2 Billion back in 2024.

Some folks noticed. Treasury met with the ICI and tax attorneys about curbing Section 351 conversions back in February, and there are some concerns that the industry is perhaps going too far. Treasury is discussing labeling 351 conversions "transactions of interest," and Senator Wyden introduced legislation to close the loophole. Fordham Law professor Colon argues Congress should revisit Section 852(b)(6) the statutory foundation of ETF tax efficiency itself. So there are a few danger signs for ETF tax efficiency.

But there's a huge counterweight: The SEC itself.

SEC Chair Atkins wrote a Washington Post op-ed cheering the dual share class framework, arguing it would extend "a major tax break to millions of people investing to build wealth." It seems unlikely that the administration that could crack down on 351 seeding from one branch would simultaneously champion the broader ETF tax advantage. Perhaps they could surgically target one without damaging the other, but my prediction is that all of this gets lost in the chaos that is Washington, and absolutely nothing of import happens to ETF tax treatment for at least a few years.

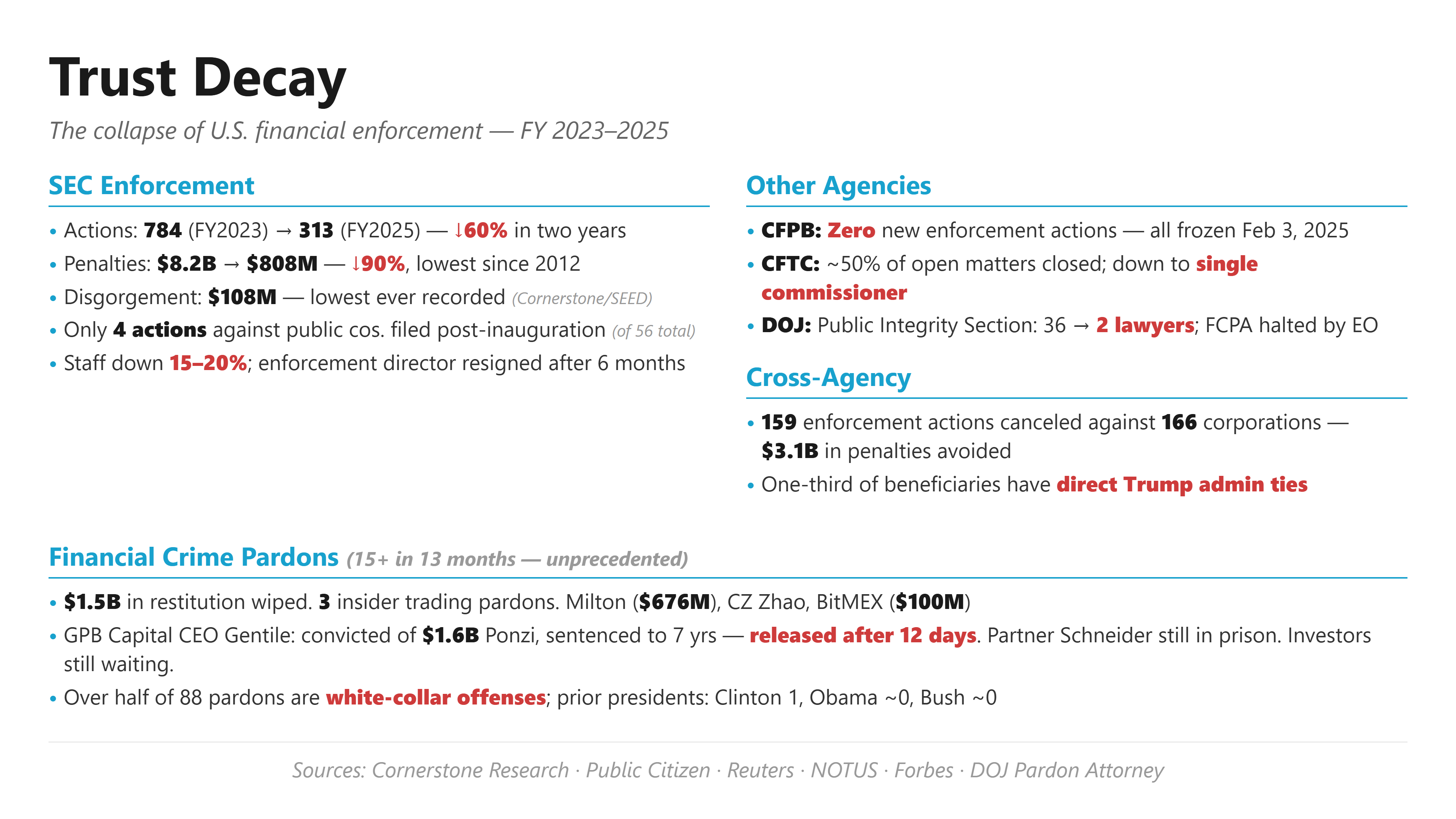

7. Trust Decay

The ETF industry's value proposition was built on trust. Back in the 1990s, they were sold hard based on transparency, regulatory oversight, fair markets and institutional backing.

That trust infrastructure is cracking, badly. It's not that the rules are changing — that would be predictable. Rather, it's that the rules no longer seem to matter.

Just this month SEC Enforcement Director Margaret Ryan resigned after just six months on the job. It's been widely reported that she clashed with Chair Atkins and the administration over cases touching Trump's circle, including Justin Sun (World Liberty Financial backer) and Elon Musk, at the same time that the staff itself lost the authority to actually do any formal probes of any kind of regulatory violation — everything now requires specific commissioner approval.

The effects have been stark: SEC enforcement actions have fallen 60% in two years (784 in FY2023 to 313 in FY2025). Monetary remedies dropped 90% ($8.2B to $808M), the lowest since FY2012. Disgorgement — where fraudsters make your clients whole — are at $108M, the lowest ever recorded. Of 56 actions against public companies in FY2025, 52 (93%) were filed under Gensler before January 20. Only 4 under Atkins. And virtually all already extant enforcement actions have been cancelled: 159 canceled or frozen enforcement actions against 166 corporations in the first year of the admin, forfeiting $3.1 billion in unpaid penalties. One third of benefiting corporations have direct ties to the administration. (Public Citizen).

Even worse, with the insanely obvious insider trading happening in both prediction markets and traditional financial markets around Trump-statements, the very folks who would actually look into it — the DOJ's Public Integrity Section — was cut from 36 full-time lawyers to just two (NOTUS).

Pile on to that over 15 securities/financial fraud pardons in 13 months (wiping at least $1.5B in restitution to, you know, folks like us, investors) and it should be very clear to investors and advisors: You are absolutely on your own.

The pardons got personal for anyone in the independent BD business with the weirdly asymmetrical commutation of half the pair sent to jail for running GPB Capital, a $1.6 billion private equity Ponzi scheme that was sold through independent broker-dealers and RIAs to thousands of retail investors. Well-connected David Gentile, GPB's CEO, was convicted in August 2024 after an exhaustive eight-week trial and sentenced to seven years. He reported to prison in November, and was released 12 days later. His partner Jeff Schneider, sentenced to six years for the exact same fraud, remains confined, and more importantly, investors — many of them clients of advisors reading this — are still waiting on any kind of restitution.

I've been playing in the ETF regulatory sandbox since before there were any ETFs at all, and I feel very confident in saying: this is the least trustworthy the U.S. financial system has been in my lifetime.

It doesn't mean numbers go down. It doesn't mean a specific firm crashes. What it means is that if you find yourself on the wrong side of a bad trade, a bad actor, a fraudster, a product that broke the rules, or a fund with a weak board who's fine ignoring the SEC, you're hosed. Trust is everything in 2026. Size, Brand and Laws absolutely do not protect you. Your skepticism for new ideas and big promises should be extreme.

8. Industry Consolidation

While all this is going on, there is a lot of capital out there looking to get into the ETF game, and there are a lot of smaller ETF issuers looking for a paycheck. There are 494 ETF issuers with over 5000 products. In 2000 there were a 5 with fewer than 100.

Goldman acquired Innovator for $2B. Schroders has agreed to a £9.9B takeover by Nuveen as passive pressure squeezes active margins. FalconX bought 21Shares for their Crypto ETFs. But not every deal is going through: Victory Capital pulled out of the Janus Henderson acquisition after Morgan Stanley and Citi wealth units urged rejection, and key PMs generating 30-40% of revenue threatened to quit (Bloomberg).

Consolidation makes sense. Top 3 providers still hold 70% of the US assets, and the advantages of scale are only compounding. As Bloomberg's Eric Balchunas puts it, the ETF industry is a terrordome of efficiency. When that terrordome meets global uncertainty and institutional decay, bad ideas and expensive products don't last long.