Get more from your core: 3 ETFs designed to diversify risk

Key takeaways:

- Government bonds have historically been the most effective risk diversifier for client portfolios.1

- These bonds span a range of securities, each with distinct characteristics and return profiles.

- Vanguard’s three new ETFs offer targeted, flexible ways to build or refine government bond allocations.

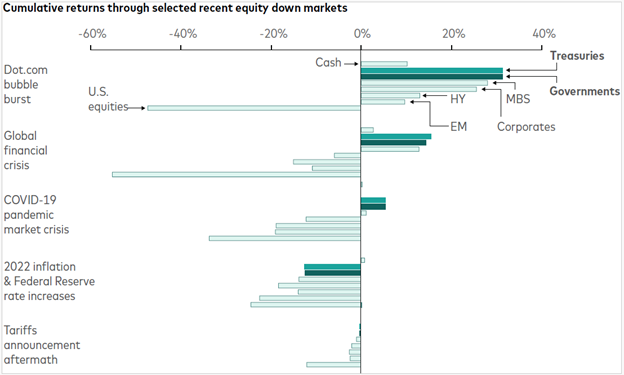

When the stock market is at its worst, government bonds often hold power for client portfolios by mitigating losses. Government or government-related bonds have historically shown the most strength during such periods.

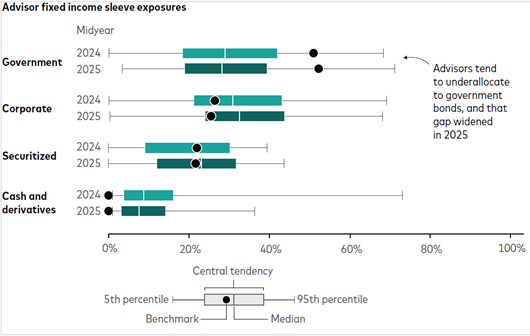

However, most advisors underallocate to government bonds, Vanguard data show. In fact, the gap between median advisor allocations and the Bloomberg US Aggregate benchmark widened in the past year to a difference of nearly 20 percentage points.

The logic is sound: In prosperous times, higher yields from credit risk are more attractive. But credit-risky sectors have historically underperformed when market turmoil or economic weakness arrives.

More risk, less safeguarding

Sources: Vanguard and Morningstar, Inc., as of June 30, 2025.

Note: There were 922 fixed income sleeves observed at midyear 2024, with an average of five tickers per sleeve, and 1,082 fixed income sleeves observed at midyear 2025, with an average of five tickers per sleeve. Fixed income charts include all observed portfolios in each time period. Fixed income benchmark: Bloomberg US Aggregate Float-Adjusted Index.

What held up when equities went down?

Past performance is not a guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Note: Cumulative returns for each category were generated using daily returns. The dot-com bubble burst is measured from March 24, 2000 to October 9, 2002; the global financial crisis is measured from October 9, 2007 through March 9, 2009; the COVID-19 pandemic market crisis is measured from February 19 through March 23, 2020; the 2022 inflation and Federal Reserve rate increases are measured from January 3 through October 12, 2022; and the tariff announcement aftermath is measured between April 2 and 8, 2022. Cash is represented by the ICE BofA US Treasury (1-3) Index. Treasuries are represented by the Bloomberg US Treasury Index. Governments are represented by the Bloomberg US Government Index. Mortgage-backed securities (MBS) are represented by the Bloomberg US MBS Index. Corporates are represented by the Bloomberg US Corporate Bond Index. High yield (HY) is represented by the Bloomberg US High Yield 2% Issuer Capped Index. Emerging markets are represented by the JPMorgan EMBI Global Index. U.S. Equities as measured by the S&P 500 Index. Data as of June 30, 2025.

It’s important to understand the wide range of securities that are considered U.S. government bonds. Here’s a quick breakdown of the most common types:

- U.S. Treasuries: Direct obligations of the U.S. government that are issued at different maturities from a few months (bills), a few years (2–10 years, notes), or for the long term (10-plus years, bonds). Treasuries are the largest, most well-supported, and liquid segment of the global bond market.

- Treasury issuance has risen from 29% of all U.S. fixed income issuance in 2017 to 45% of the $10.4 trillion in U.S. issuance in 2024.2

- Government agency mortgage-backed securities (MBS): Structures that pool together various mortgage types and carry either an explicit government backing through a government agency (GNMA) or implicit backing through a government-sponsored enterprise (FNMA, FHLMC). Monthly principal and interest payments on the underlying mortgages are passed through to the bond holder. They face the risk of prepayments if mortgage rates decline.

- Treasury Inflation-Protected Securities (TIPS): Direct obligations of U.S. government with principal values that are adjusted upward or downward based on the Consumer Price Index. TIPs are issued with 5, 10, or 30-year maturities. The principal at maturity is either the original principal or the principal adjusted for inflation, whichever is greater.

- Market pricing is based on inflation and interest rate expectations, which can change quickly. TIPS are still subject to the same inverse relationship between price and yield as other bonds.

These differences matter. Shifts in short- or long-term rates can affect yields and prices across the yield curve. All-curve fixed income ETFs, therefore, offer a one-stop-shop alternative to positioning across short-, intermediate-, and long-term buckets.

Moreover, the premier broad measure of the U.S. bond market—the Bloomberg US Aggregate Index—has been comprised of more U.S. Treasuries in recent years, as U.S. government funding needs have risen. Treasuries made up less than a quarter of the index 20 years ago, which grew to nearly half of the index as of December 31, 2024.

With the broad index heavy in government bonds, many advisors choose to use ETFs that track portions of the index, colloquially called the Agg, as well as portions outside the Agg. This helps them design customized fixed income portfolios to better meet client preferences and goals.

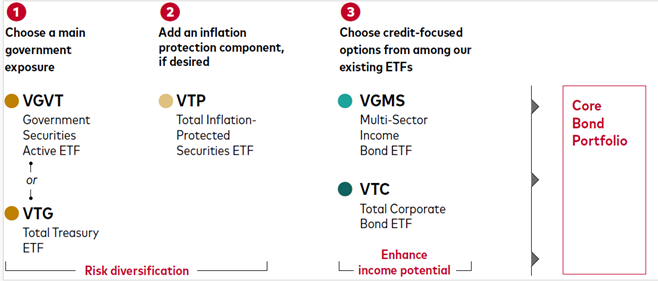

To help you tailor your clients’ portfolios more precisely, Vanguard launched three new ETFs in July:

Name | Expense | Duration | Use Case | Strategy | Could Be Suitable For |

|---|---|---|---|---|---|

| Vanguard Government Securities Active ETF (VGVT) | 0.10% | Intermediate (Manager discretion within 0.5 years of benchmark) | Flexible and full-curve exposure (0–30 years). Potential for outperformance. Managed by Vanguard’s Fixed Income team. | Invests in Treasuries, agency MBS, and other government-backed securities. Up to 10% may be in non-government securities. Uses active strategies including security selection, quantitative models, sector rotation, and curve positioning. | Investors seeking high-quality ballast to equities with potential to outperform U.S. Treasuries. |

| Vanguard Total Treasury ETF (VTG) | 0.03% | ~6 years | Full-curve Treasury exposure (1–30 years). Can be paired with corporate bond ETFs to adjust credit risk. | Index ETF tracking the Bloomberg US Treasury Total Return Unhedged USD Index. | Advisors seeking broad Treasury exposure without managing multiple segmented ETFs. |

| Vanguard Total Inflation-Protected Securities ETF (VTP) | 0.05% | ~6 years | Full-curve TIPS exposure (1–30 years). Complements a diversified bond portfolio. | Index ETF tracking the ICE US Treasury Inflation Linked Bond Index. | Investors with longer horizons seeking inflation protection. |

These ETFs can serve as the high-quality government bond allocation within a complete bond portfolio that can be customized to meet individual client’s needs.

Vanguard fixed income ETFs that complement a government allocation include:

- Vanguard Multi-Sector Bond Income ETF (VGMS), an active ETF that incorporates a spectrum of credit holdings, including high yield and emerging markets, as well as some investment-grade bonds.

- Vanguard Total Corporate Bond ETF (VTC), an index ETF that offers investment-grade corporate bond exposure across the yield curve.

With these ETFs, advisors can easily adjust the amount of credit risk in their clients’ portfolios either to defend against market turmoil or to take advantage of strong yields.

The new ETFs can lay the foundation for a core bond portfolio

Source: Vanguard.

1 Source: Vanguard Investment Advisory Research Center analysis using data from Morningstar, Inc. from January 1, 1988 through December 31, 2024.

2 Source: Securities Industry and Financial Markets Association, data as of December 31, 2024.

3 The expense ratio information shown reflects estimated amounts for the current fiscal year.

Notes:

For more information about Vanguard funds and Vanguard ETFs, visit vanguard.com to obtain a prospectus or, if available, a summary prospectus. Investment objectives, risks, charges, expenses, and other important information are contained in the prospectus; read and consider it carefully before investing.

Vanguard ETF Shares are not redeemable with the issuing Fund other than in very large aggregations worth millions of dollars. Instead, investors must buy and sell Vanguard ETF Shares in the secondary market and hold those shares in a brokerage account. In doing so, the investor may incur brokerage commissions and may pay more than net asset value when buying and receive less than net asset value when selling.

All investing is subject to risk including the possible loss of the money you invest. Diversification does not ensure a profit or protect against a loss. Past performance is no guarantee of future results.

Bond funds are subject to the risk that an issuer will fail to make payments on time, and that bond prices will decline because of rising interest rates or negative perceptions of an issuer’s ability to make payments.

Investments in bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk. These risks are especially high in emerging markets.

High-yield bonds generally have medium- and lower-range credit-quality ratings and are therefore subject to a higher level of credit risk than bonds with higher credit-quality ratings.

U.S. government backing of Treasury or agency securities applies only to the underlying securities and does not prevent share-price fluctuations. Unlike stocks and bonds, U.S. Treasury bills are guaranteed as to the timely payment of principal and interest.