The Power Buildout: A Multi-Decade Investment Cycle

Power demand is projected to grow ~2.5% annually through 2030, and 50–100% by 2050, creating significant multi-decade investment opportunities across the power value chain in both the production, delivery, and consumption of power.

Power Demand – The Situation in 2026

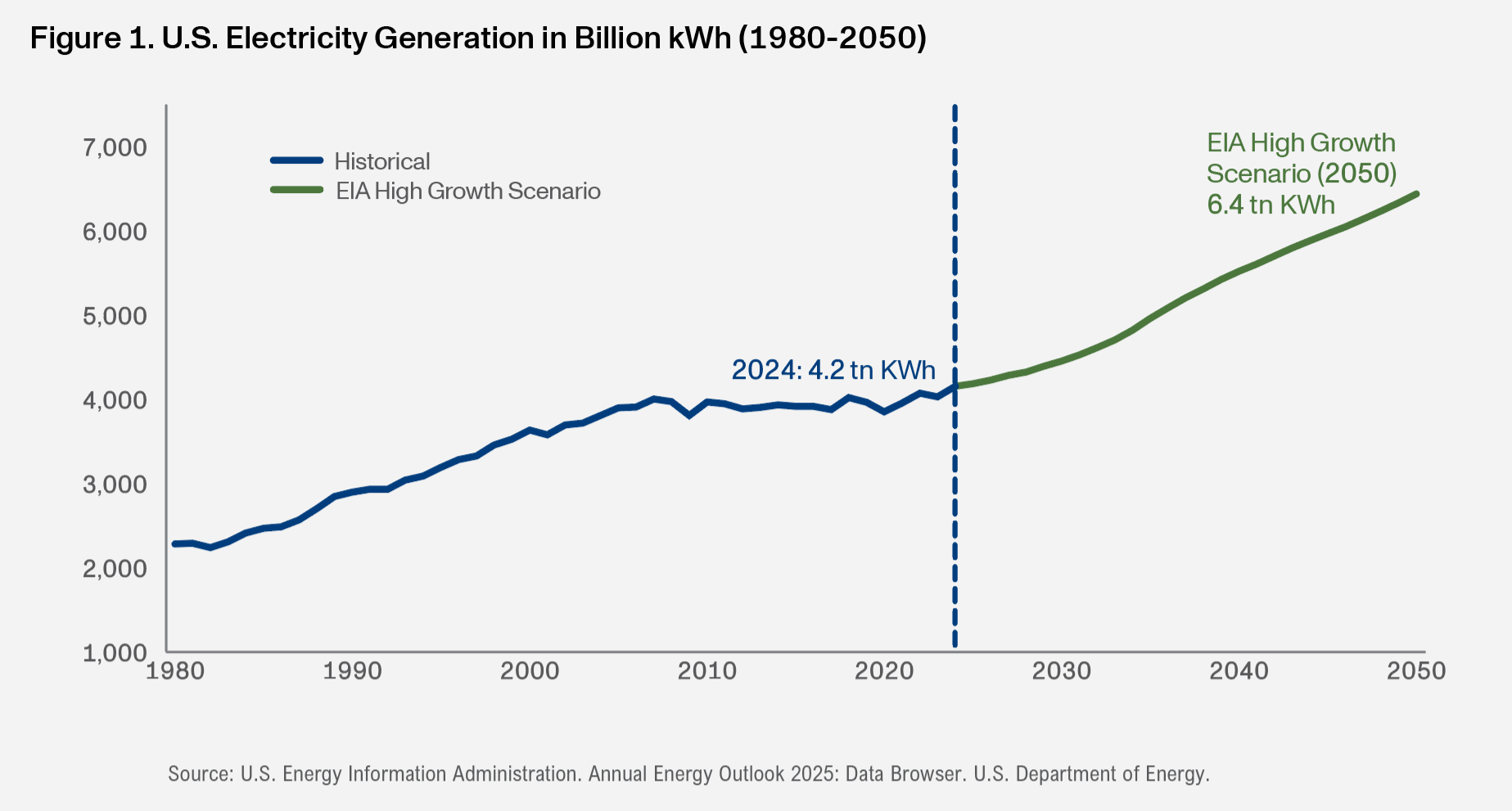

The U.S. is currently in the midst of a once-in-a-generation shift in electricity market dynamics, as power demand growth, driven by AI and cloud datacenters, industrial reshoring, and electrification,1 is outpacing power supply growth. The U.S. Energy Information Administration’s (EIA) latest forecast sees electricity consumption growing by 1% in 2026 and 3% in 2027, after growing 2-2.5% annually in 2024 and 2025, “marking the first four years of consecutive growth since 2005-2007, and the strongest four-year period of growth since the turn of the century” (see Figure 1).2

The resultant supply shortage is driving up electricity prices, especially in power markets with concentrated datacenter buildout such as PJM Interconnection (covering 13 mid-Atlantic and Midwest states), where the latest capacity auction cleared at the record price cap of $333/Megawatt-day for the 2026/27 delivery year, up ~10x from 2023-2024, and would have hit $530/MW-day in the absence of a price cap. The auction still fell 6.6 GW short of its reserve margin target, meaning an emergency backstop auction may be required to alleviate reliability concerns.3

Energy affordability, which was already a hotly debated topic during election campaigns in 2025, is set to become a political flashpoint ahead of the 2026 midterms, as datacenters are blamed for rising power prices, blackouts, and water shortages. Several states are considering a pause on new data centers and legislation requiring tech firms to fund grid upgrades.

Looking ahead, the U.S. faces a multi-year power crunch. Since January 2021, $3 trillion in mega project investments have been announced across North America, of which only 16% have broken ground,4 implying a strong pipeline for future construction and power demand growth. Large and fast-growing AI/cloud computing companies (“hyperscalers”) continue to accelerate their datacenter buildout and are on track to spend over $650 billion on AI investments this year (60%+ higher than 2025).5

Power demand is projected to grow ~2.5% annually through 20306, and 50-100% by 2050,7,8 creating significant multi-decade investment opportunities across the power value chain in both the production, delivery, and consumption of power.

Supply-Side: Building and Fueling the Next Grid

Meeting this unprecedented growth in demand will require a massive buildout of low-carbon, reliable, and dispatchable generation from a diversified mix of energy sources, as each energy source has its own constraints:

- Renewables offer the quickest path to power and are preferred by hyperscalers for their emissions reduction goals. However, in addition to interconnection delays, the intermittent nature of renewables is incompatible with the 24/7 power needs of datacenters without additional backup generation or battery storage.

- Natural gas, as a transition fuel, is a reliable and relatively lower carbon source of energy, but faces permitting and pipeline bottlenecks, and a 5+ year wait for gas turbines.

- Nuclear power continues to gain momentum, but near-term capacity additions remain limited to restarts and uprates of existng plants, with any new advanced reactors unlikely to be operational before 2030.

Consumption-Side: Three Structural Drivers of Growth

Although data centers dominate media coverage, they only account for about 40% of projected annual demand growth through 2030, and roughly 11% of total power consumed in 2030. Through 2030, demand growth will be driven by three distinct forces: the rapid expansion of data center infrastructure (~40% of total projected demand growth), a reversal of decades-long industrial power decline as manufacturing re-shores (~17%), and accelerating electrification across transportation and buildings (~43%).9

- The datacenter revolution is reshaping infrastructure needs. Training and inference workloads are growing exponentially, driving up demand for high performance chips, and power and thermal management systems, and AI infrastructure platforms that can deploy, customize, and monetize models at scale. Additionally, grid constraints, equipment and construction backlogs are changing where and how data centers are built, driving up demand for modular data center construction, distributed energy resources such as utility-scale batteries, diesel generators, and repurposed engines, not just for emergencies, but as primary power.

- Annual industrial power demand in the U.S. peaked in 2000 and has since declined 4-6% in aggregate, stabilizing at around 1,000-terawatt hours in recent years (~25% of total U.S. demand)10 due to the large-scale offshoring of manufacturing during the height of globalization. This trend is now reversing as manufacturing increasingly returns to the U.S., driven by a prioritization of supply chain resiliency and security and bipartisan support.

- Electrification across transportation and buildings is emerging as a significant driver of long-term electricity demand growth. Despite federal policy shifts, Electric vehicles (EVs) are projected to increase their share of the U.S. retail auto market from roughly 10% in 2024 to 27% by 203011, supported by state and local policy incentives, declining component costs, improved battery ranges, faster charging speeds, and continued expansion of charging infrastructure. Residential and commercial building electrification is accelerating as consumers and businesses increasingly adopt electric heat pumps, air conditioners, cooking appliances, and other electric technologies. This shift is driven largely by economic and efficiency gains, including lower upfront prices, reduced operating and maintenance costs, and access to utility and government incentives.

- Growing loads from transportation and building electrification are expected to intensify load volatility and create localized surges in electricity demand because charging tends to be highly concentrated in the evenings and at specific locations, such as homes and public charging stations. This pattern is already prompting utilities and grid operators to invest in grid hardening equipment, smart charging infrastructure, and other localized grid upgrades to manage peak loads and ensure reliability as adoption scales.

The rising power demand and power-intensity of end uses is placing significant stress on new and ageing U.S. grid infrastructure. Demand for electrical capital goods has led to 2-3 year lead times for transformers and switchgear. Additionally, engineering and construction companies that build and repair electrical grids and datacenter infrastructure are experiencing record backlogs and labor shortages. Materials companies are also benefiting from this sustained and resurgent need for capital investment, as demand for steel, copper, concrete, and other critical materials and metals pushes up global commodity prices.

The TCW Edge

The U.S. is entering a new era of power scarcity and reinvention. The transition to a digital and electrified economy is colliding with the physical limits of the grid and geopolitical tensions. But this challenge is also a generational investment opportunity.

TCW Transform Systems (PWRD) and TCW Artificial Intelligence (AIFD) ETFs aim to capture and navigate this moment. PWRD targets companies enabling the power buildout: from gas turbines and nuclear developers to grid equipment suppliers, Energy Performance Certificates (EPCs), and energy storage innovators. AIFD focuses on the demand side: the AI infrastructure leaders building, training, and scaling next-gen models, often in power-constrained environments.

1 Chintalapati, Varun, and Eli Horton. America’s Thirst for Power: More Than Just Data Centers. TCW, 14 July 2025.

2 U.S. Energy Information Administration. Short-Term Energy Outlook. U.S. Department of Energy.

3 PJM Interconnection. 2027/2028 Base Residual Auction Report. PJM, 17 December 2025.

4 Eaton Corporation Earnings Call Q4 2025 (February 2026)

5 Company announcements

6 Goldman Sachs Research. AI/Data Center Power Demand: The 6 Ps driving growth and constraints. Goldman Sachs, 13 October 2025.

7 National Electrical Manufacturers Association. A Reliable Grid for an Electric Future: NEMA’s Grid Reliability Study. Make It Electric, April 2025.

8 Gagnon, Pieter, et al. 2024 Standard Scenarios Report: A U.S. Electricity Sector Outlook. National Renewable Energy Laboratory, December 2024.

9 Goldman Sachs Research. AI/Data Center Power Demand: The 6 Ps driving growth and constraints. Goldman Sachs, 13 October 2025.

10 U.S. Energy Information Administration. Monthly Energy Review - February 2026 (Table 7.6). U.S. Department of Energy.

1 1 BloombergNEF Electric Vehicle Outlook 2025, June 2025.

Before investing you should carefully consider the fund’s investment objectives, risks, charges, and expenses. This and other information is in the prospectus, a copy of which may be obtained from etf.tcw.com. Please read the prospectus carefully before you invest.

INVESTMENT RISKS

TCW Transform Systems ETF (PWRD) is actively managed and may be susceptible to an increased risk of loss, including losses due to adverse events that affect the Funds’ investments more than the market as a whole, to the extent that the Funds’ investments are concentrated in the securities of a particular issuer or issuers, country, group of countries, region, market, industry, group of industries, sector or asset class. Shares are subject to the risks of an investment in a portfolio of equity securities in an industry or group of industries in which each Fund invests. Investments in emerging market countries may be subject to greater risks than investments in developed countries. The Funds may purchase and write put and call options on futures contracts that are traded on an exchange as a hedge against changes in value of its portfolio securities, or in anticipation of the purchase of securities, and may enter into closing transactions with respect to such options to terminate existing positions. There is no guarantee that such closing transactions can be effected. Transform Systems ETF is a non-diversified management investment company under the Investment Company Act of 1940. Diversification does not assure a profit or protect against a loss in a declining market. It’s not possible to invest in an index. An outbreak of an infectious respiratory illness, COVID-19, has resulted in significant economic impacts. Other infectious illness outbreaks in the future may result in similar or other impacts. TCW may consider any sustainability factors as core to its investment process but its specific focus for the Transform Systems ETF will be on the environmental factors most relevant to climate change. TCW intends to incorporate sustainability insights and analysis to ultimately drive financial and operational performance however there is no guarantee that this strategy will be achieved, and such assessment is at TCW’s discretion. TCW does not use sustainability ratings or rankings to exclude specific companies, but instead uses its own proprietary analysis to attempt to make better informed decisions. The Transform Systems ETF may forgo certain investment opportunities that do not TCW’s criteria and results may be lower than other funds that use different or no sustainability criteria to screen out certain companies or industries. All investing involves risk including the potential loss of principal. Market volatility may significantly impact the value of your investments. Recent tariff announcements may add to this volatility, creating additional economic uncertainty and potentially affecting the value of certain investments. Tariffs can impact various sectors differently, leading to changes in market dynamics and investment performance. Please see the Fund’s Prospectus for more information on these and other risks.

TCW Artificial Intelligence ETF (AIFD) seeks to invest in the companies that the Adviser believes will benefit from the artificial intelligence, or “AI,” transformation. The Fund’s investment objective is long-term growth of capital. The Fund is actively managed and may be susceptible to an increased risk of loss, including losses due to adverse events that affect the Funds’ investments more than the market as a whole, to the extent that the Funds’ investments are concentrated in the securities of a particular issuer or issuers, country, group of countries, region, market, industry, group of industries, sector or asset class. The Funds may purchase and write put and call options on futures contracts that are traded on an exchange as a hedge against changes in value of its portfolio securities, or in anticipation of the purchase of securities, and may enter into closing transactions with respect to such options to terminate existing positions. There is no guarantee that such closing transactions can be effected. TCW Artificial Intelligence ETF (AIFD) is subject to the following risks: Equity securities are subject to changes in value, and their values may be more volatile than those of other asset classes. The net asset value of the Fund will fluctuate based on changes in the value of the equity securities held by the Fund. Funds investing in mid and small cap companies involve special risks including higher volatility and lower liquidity. The Fund’s investments in companies involved in, or exposed to, artificial intelligence-related businesses may be negatively impacted because of, among other things, limited product lines, markets, financial resources and/or personnel these companies may have, intense competition and potentially rapid product obsolescence these companies may face, loss or impairment of intellectual property rights, and the inability to successfully develop products or services even after spending significant amount of resources. Undervalued stocks may not realize their perceived value for extended periods of time or may never realize their perceived value. Value stocks may respond differently to market and other developments than other types of stocks. The Fund will concentrate its investments in various technology industries. At times of such impact, the value of the Fund may fluctuate more widely than it would for a fund that invests more broadly across varying sectors. The Fund may be more susceptible to any single economic, political, or regulatory event than a diversified fund because a higher percentage of the Fund’s assets may be invested in the securities of a limited number of issuers. Investments in emerging market countries may be subject to greater risks than investments in developed countries. Active ownership can take any of several forms, including proxy battles, publicity campaigns, and negotiations with management. In the event that an affiliate of the Fund or its investment adviser is engaged in an activist campaign with respect to a portfolio company, the Fund may be foreclosed from taking certain actions with respect to that company as a result of prohibitions on engaging in joint transactions with affiliates under Section 17(d) of the 1940 Act or as a result of other regulatory or fiduciary concerns. The Fund is considered to be non-diversified, which means that it may invest more of its assets in, and be more exposed to the risks of, the securities of a single issuer or a smaller number of issuers, which may increase the Fund’s volatility. All investing involves risk including the potential loss of principal. Market volatility may significantly impact the value of your investments. Recent tariff announcements may add to this volatility, creating additional economic uncertainty and potentially affecting the value of certain investments. Tariffs can impact various sectors differently, leading to changes in market dynamics and investment performance. Please see the Fund’s Prospectus for more information on these and other risks.

The Fund is advised by TCW Investment Management Company LLC. Distributed by Foreside Financial Services, LLC. Effective October 13, 2023, the Transform Fund’s adviser became TCW Investment Management Company LLC. Prior to that date, the Transform Fund’s adviser was Fund Management at Engine No. 1 LLC.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

© 2026 TCW Group. All rights reserved.