Underweight international? The data says it’s worth a second look

After more than a decade of playing the underdog to U.S. markets, developed international equities just reminded everyone they’re still in the game.

The MSCI EAFE® Price Return Index surged 27.9% in 2025, tacking on another 9.6% as of the end of February, handily outpacing the familiar favorite, the S&P 500® Price Return Index, which returned 16.4% in 2025 and -0.3% at the end of February.

For anyone wondering when international would “show up,” well, it just did.

The portfolio problem: investors are underweight international

If you feel underweight in your international exposure, you’re not alone, and you’re not irrational.

Looking back at the post-financial-crisis era, U.S. large caps have pulled far ahead of developed ex‑U.S. stocks. From 2009 – 2024, the S&P 500® Price Return Index delivered about 8-8.5 percentage points more return per year than the MSCI EAFE® Price Return Index, whether measured using rolling or calendar‑year periods. That’s a long time to be on the wrong side of relative performance.

Meanwhile, U.S. investors have kept roughly three‑quarters of equity exposure at home, according to Charles Schwab, IMF PIP, and MSCI index data. A classic “home bias” that’s well above the U.S. share of global market capitalization at approximately 49%, according to World Federation of Exchanges and SIFMA estimates.

Is there really steam left in international trade?

Three forces are driving renewed interest in international equities:

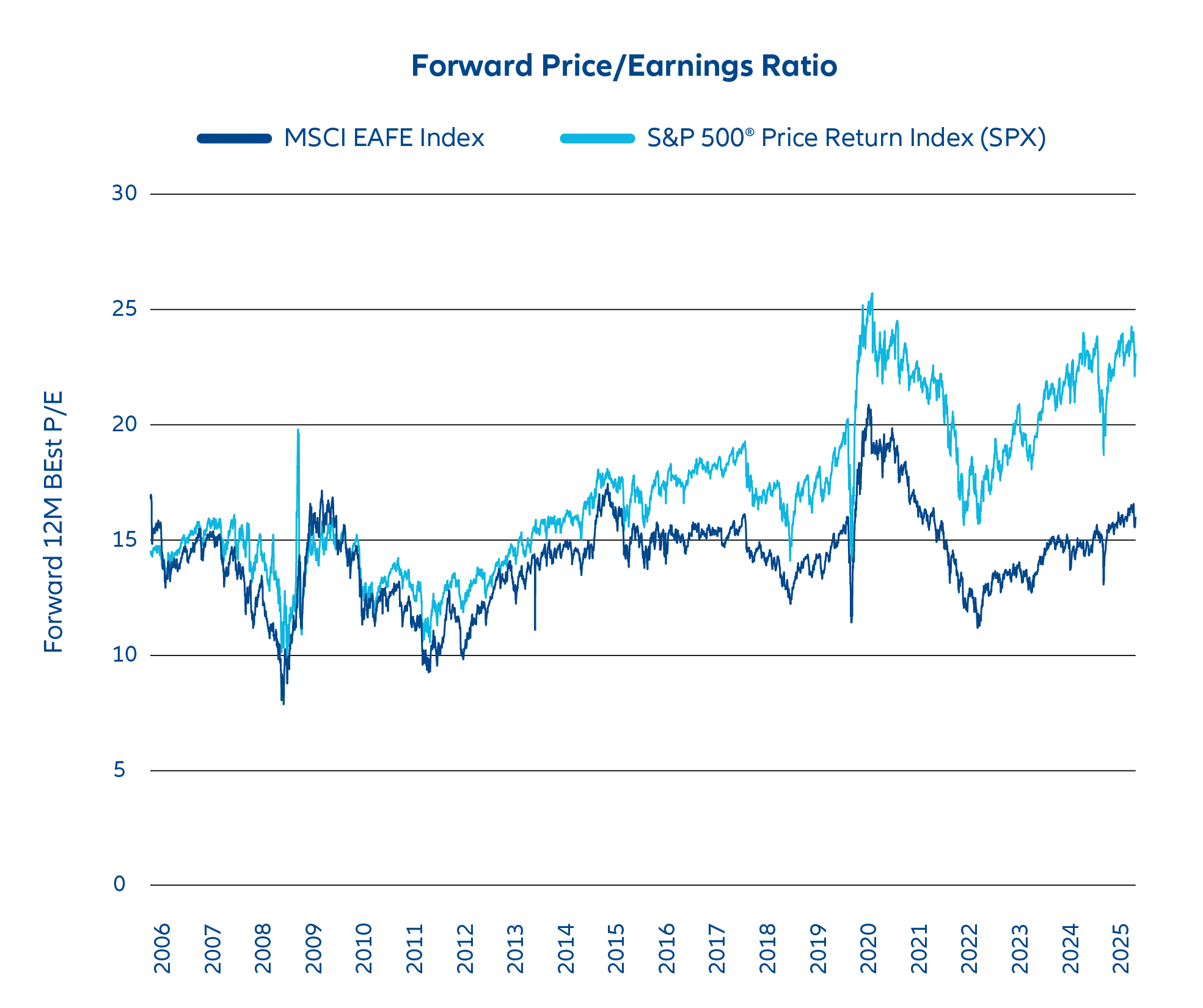

- Valuation gap: Developed ex U.S. equities have traded at a discount to the U.S. On forward earnings, international sits around the high teens multiple versus low 20s for U.S. large caps. The gap has narrowed from its extremes, but remains meaningful. Historically, valuation cycles tend to mean revert over multi year windows.

Source: Bloomberg Professional LP as of 11/30/2025; BEST P/E Ratio provides the forward-looking P/E ratio based on Bloomberg consensus earnings estimates. You cannot invest directly in an index.

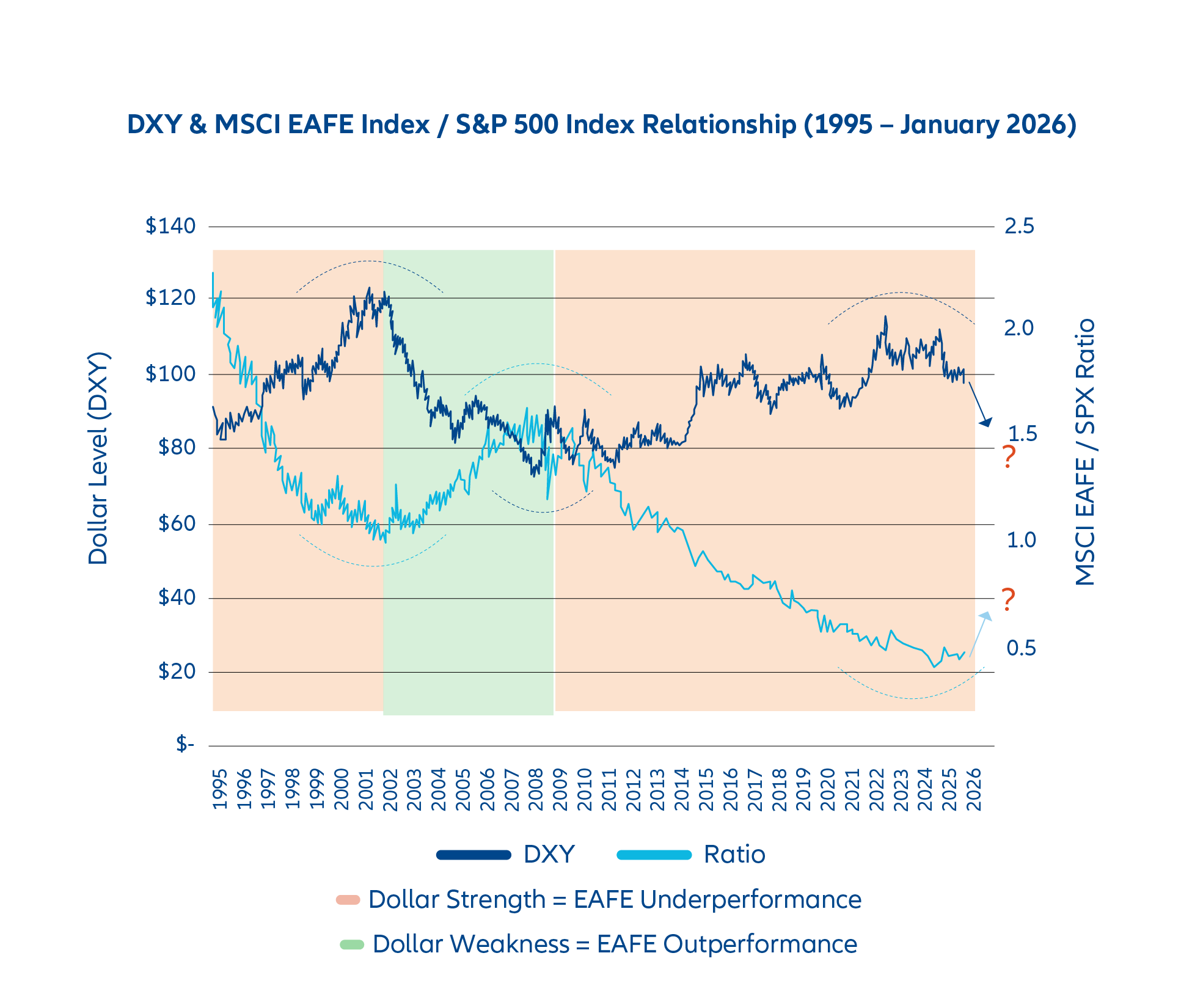

- The dollar’s direction: Over the last 30 years, periods of a falling U.S. dollar, represented by DXY in the below chart, have generally coincided with international (MSCI EAFE) outperformance vs. the S&P 500, while a rising dollar has tended to favor the U.S. While it’s not a straight line, the trend relationship has mattered for relative returns. If the next leg is a softer dollar, that historically has been a tailwind for international markets.

Source: Bloomberg Professional LP as of 1/31/2026. Allianz Investment Management LLC. Past performance is not a guarantee of future results. You cannot invest directly in an index.

- Macro and policy noise: Trade and tariff headlines continue to shift. While the specifics change, the takeaway for portfolios is consistent: policy uncertainty can amplify currency and earnings dispersion across markets, making how investors enter positions and manage risk more important than ever.

But what if this is just another head fake?

Fair question. The 1990s offered a case study in false starts. The MSCI EAFE® Price Return Index outperformed in 1993 and 1994 by 23.4% and 7.8%, respectively, only to see the S&P 500 Price Return Index go on to strongly outperform it in the following four years (24.7% in 1995, 15.9% in 1996, 30.8% in 1997, 8.4% in 1998).

Timing a secular handoff is difficult, especially against a benchmark with sector tilts (namely overweight U.S. tech/communication) that has dominated the earnings cycle.

Translation for investors: International can shine in bursts and then fade. The goal isn’t to call the turn; it’s to engineer the ride so that international diversification can contribute without derailing outcomes.

A 3 step decision guide for re-entering international

The following can serve as a short, repeatable framework for evaluating international exposure in portfolio reviews and model updates.

Step 1: Clarify the why

- Growth optionality: Capture earnings and multiple expansion where starting valuations are lower and cycles are less synchronized with the U.S.

- Diversification repair: Reduce U.S. concentration risk and bring models closer to global weights or long-term allocation targets that drifted during U.S. outperformance.

Viewed this way, the decision is less about chasing a trade and more about rebalancing the opportunity set.

Step 2: Choose your risk posture

- Risk managed exposure: Because international markets tend to deliver more frequent swings and a choppier ride, buffered strategies can act as a powerful stabilizer. These strategies, linked to widely used international benchmarks such as MSCI EAFE®, aim to absorb a predefined portion of downside over an outcome period. Traditional buffered funds often cap upside potential to finance the buffer, while uncapped designs seek upside participation beyond a spread while still offering downside protection. Consider capped vs. uncapped, buffer size, and reset cadence.

- Pure beta exposure: Decide between broad passive EAFE exposure or actively managed approaches (quality/valuation tilts, dividend bias, currency hedged vs. unhedged).

Key trade off: Aiming for a smoother ride vs. maximum upside participation. Align the choice to risk budgets, sequence risk sensitivity, and review frequency.

Step 3: Pick the vehicle

- ETFs: Tax efficient, intraday liquidity, transparent; wide menu of passive, active, and buffered strategies.

- Mutual funds: Broad active selection and next trading day liquidity, but very few buffered or passive strategies.

- UITs: Set start/end dates (often 12-24 months); buffered options exist, but usually with a higher total cost than comparable ETFs and mutual funds.

Positioning portfolios for what’s next: AllianzIM Uncapped Buffer15 ETFs

For those looking to rebuild international exposure without taking on the full risk of the market or being boxed in by an upside cap, the AllianzIM International Equity Buffer15 Uncapped ETF series offers a timely solution.

The newest fund in the series, the AllianzIM International Equity Buffer15 Uncapped Apr ETF (“ARLI”), seeks to provide 15% downside protection over a one year outcome period on the iShares MSCI EAFE® ETF (“EFA”), paired with unlimited upside potential beyond a spread.

How does it work? Hypothetically speaking, if EFA finished the outcome period down 20%, the 15% buffer aims to limit the fund’s loss to about 5%, less fees and expenses. Conversely, if EFA were up 23%, and the spread was 3%, the fund seeks to capture the remaining 20%, less fees and expenses.

ARLI is the second ETF in this lineup, joining the AllianzIM International Equity Buffer15 Uncapped Jan ETF (“JANI”), which launched at the start of February 2026.

- The design problem these aim to solve: In strong bull markets, traditional capped buffered funds can make investors feel as though they “overpaid” for downside protection once the cap is hit. The uncapped structure aims to maintain the buffer while allowing for continued upside participation beyond a defined spread, addressing one of the most consistent behavioral pain points.

- Uncapped buffered ETF mechanics: Each fund operates on a clearly defined outcome schedule with annual resets, providing an intuitive review cadence. At each reset, the buffer and spread refreshes, giving you an opportunity to continually revisit the position’s role and fit within a broader portfolio or model.

Why ARLI can fit into a portfolio or model now

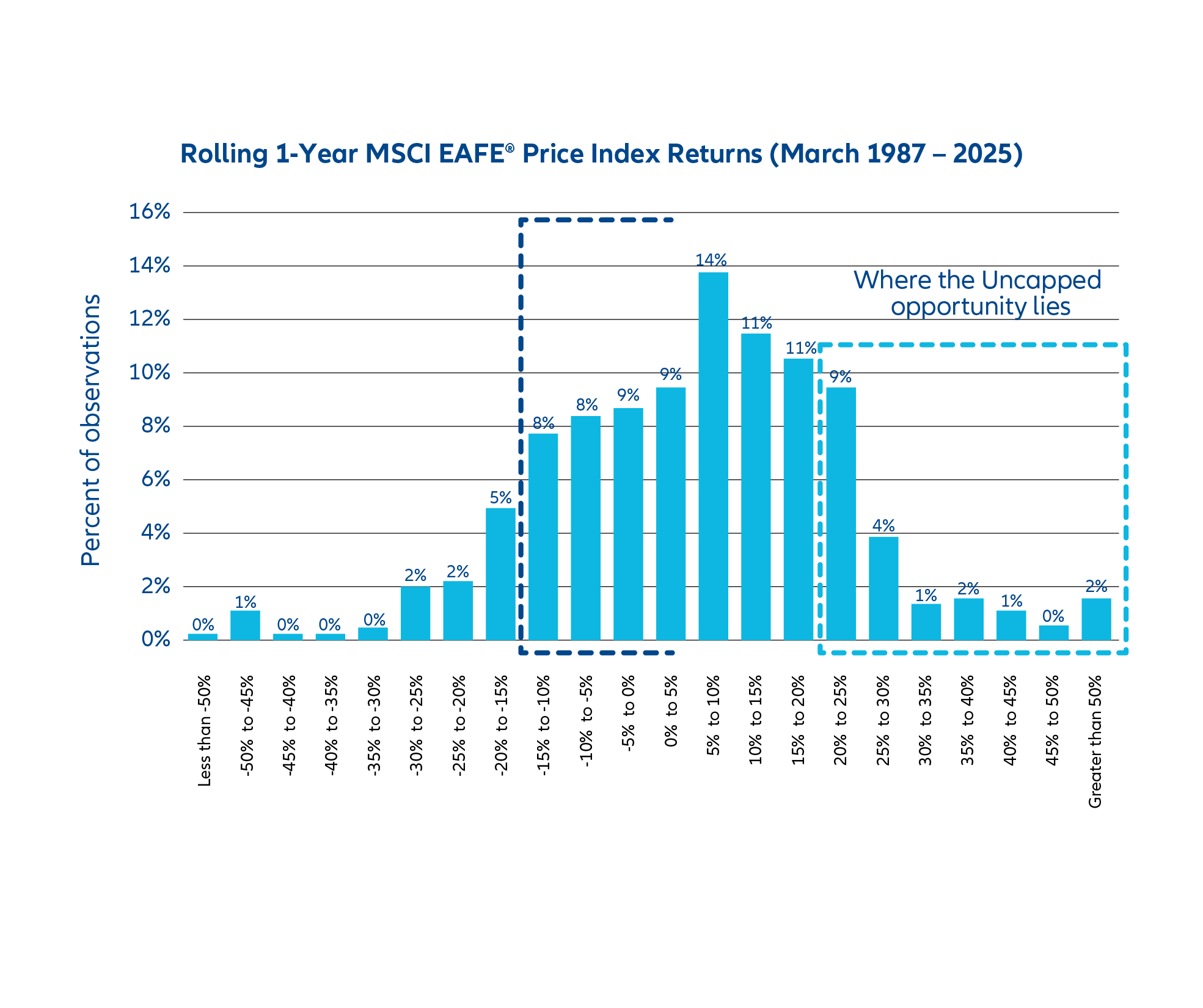

- Seek a smoother ride: A 15% buffer has historically covered a large majority of negative one year rolling return scenarios for EAFE since the late 1980s, helping to smooth the ride when international volatility resurfaces. Since March 1987 (one year after the MSCI EAFE® Price Return Index inception), a 15% buffer would have covered about 89% of one year observations. Past performance is not indicative of future results; buffers don’t protect against all losses.

Source: Bloomberg Professional L.P. as of 12/31/2025. Allianz Investment Management LLC. Past performance is not a guarantee of future results.

- Managing the fear of missing out: After a strong run, investors often wrestle with the urge to join the rally and the fear of getting in too late. The unlimited upside, after a spread, lets you stay in the conversation if international equities continue to climb. Meanwhile, the 15% buffer aims to provide protection during the inevitable bouts of volatility – an approach that bridges the gap between FOMO and fear of regret.

- Replacement or complement to existing allocations: The uncapped Buffer15 structure of ARLI and JANI can slot in as a core developed ex‑U.S. sleeve, replacing part of an existing international exposure or complementing a pure‑beta or actively managed position.

ETF-765 (3/2026)

For more information on AllianzIM ETFs, visit www.allianzIMetfs.com.

Investment involves risk, including possible loss of principal. There is no guarantee the funds will achieve their investment objectives and may not be suitable for all investors.

Investors should consider the investment objectives, risks, charges, and expenses carefully before investing. For a prospectus with this and other information about the fund, please call 877.429.3837 or visit our website at www.allianzIMetfs.com. Read the prospectus carefully before investing.

Investors may lose their entire investment, regardless of when they purchase shares, and even if they hold shares for an entire outcome period. Full extent of the spread and buffers only apply if held for stated outcome period and are not guaranteed. The spread may increase or decrease and may vary significantly from outcome period to outcome period.

The spread cost represents the upside performance a shareholder forgoes in return for the downside protection provided by the buffer. Any upside performance as measured at the end of the outcome period will be reduced by the spread cost and management fee. The fund's performance will not reflect the entirety of any upside performance of the reference asset.

The S&P 500® Price Return Index is a broad measure of U.S. large-cap stocks and does not include reinvestment of dividends. The MSCI EAFE® Price Return Index is a broad measure of large- and mid-cap developed market equities from Europe, Australasia, and the Far East and does not include reinvestment of dividends. An investor cannot invest directly in an index.

Buffered ETFs’ investment strategies are different from more typical investment products, and the Funds may be unsuitable for some investors. It is important that investors understand the investment strategy before making an investment. For more information regarding whether an investment in the Funds is right for you, please see the prospectus including "Investor Considerations.”

Allianz Investment Management LLC (AllianzIM), a wholly owned subsidiary of Allianz Life Insurance Company of North America, is a registered investment adviser and adviser to AllianzIM ETFs. Allianz Investment Management LLC, Allianz Life Insurance Company of North America, and Allianz Life Financial Services, LLC are affiliated companies and are not affiliated with Foreside Fund Services, LLC.

Distributed by Foreside Fund Services, LLC.

Join the Largest ETF Meetings Event in the World - 2,000+ Attendees, 20,000+ Meetings, the Entire ETF Ecosystem in 1 Place. Brought to You by ETF.com Learn More