Why Active ETFs Matter More in 2026

01 Active ETFs are a central tool for modern portfolio construction, offering investors a flexible and efficient way to access active management.

02 In a market defined by high concentration and growing dispersion, active strategies are proving their value by helping investors navigate complexity and uncover differentiated opportunities.

03 From equities to fixed income, active ETFs are gaining momentum as advisors seek more precise, transparent, and tax-efficient ways to manage risk and pursue outcomes.

In 2025, the U.S. ETF market set a staggering record with $1.47 trillion in total net inflows. Active ETFs were the primary catalyst for this expansion, capturing over $450 billion in U.S. net inflows – accounting for roughly 30% of all ETF flows despite representing only 11% of total U.S. ETF assets.

The Explosive Growth of Active ETFs: Data & Market Dynamics

The exchange-traded fund has come a long way over the past 30 years. Originally conceived by regulators in the wake of the 1987 market crash to facilitate trading large baskets of stocks, ETFs have evolved into a market exceeding $13.5 trillion in U.S. assets as of year-end 2025, expanding at roughly 33% per year.1 For much of their rise, ETFs were synonymous with passive investing. Many active strategies underperformed after fees; the ETF allowed institutional investors and retail retirement savers to own the market and trade it with the ease of a single stock. For many clients, the new vehicle also offered improved tax efficiency at minimal cost. For a time, the rise of passive investing was almost indistinguishable from the growth of ETFs.

But markets do not remain static. The tremendous inflows into passive ETFs have reshaped market structure, influencing concentration, liquidity, and, in turn, how ETFs are deployed within portfolios. Actively managed ETFs, once viewed as a sideline, have now become the fastest- growing segment of the ETF market. Advisors increasingly combine passive and active exposures, using ETFs as a foundation for more robust portfolio construction.

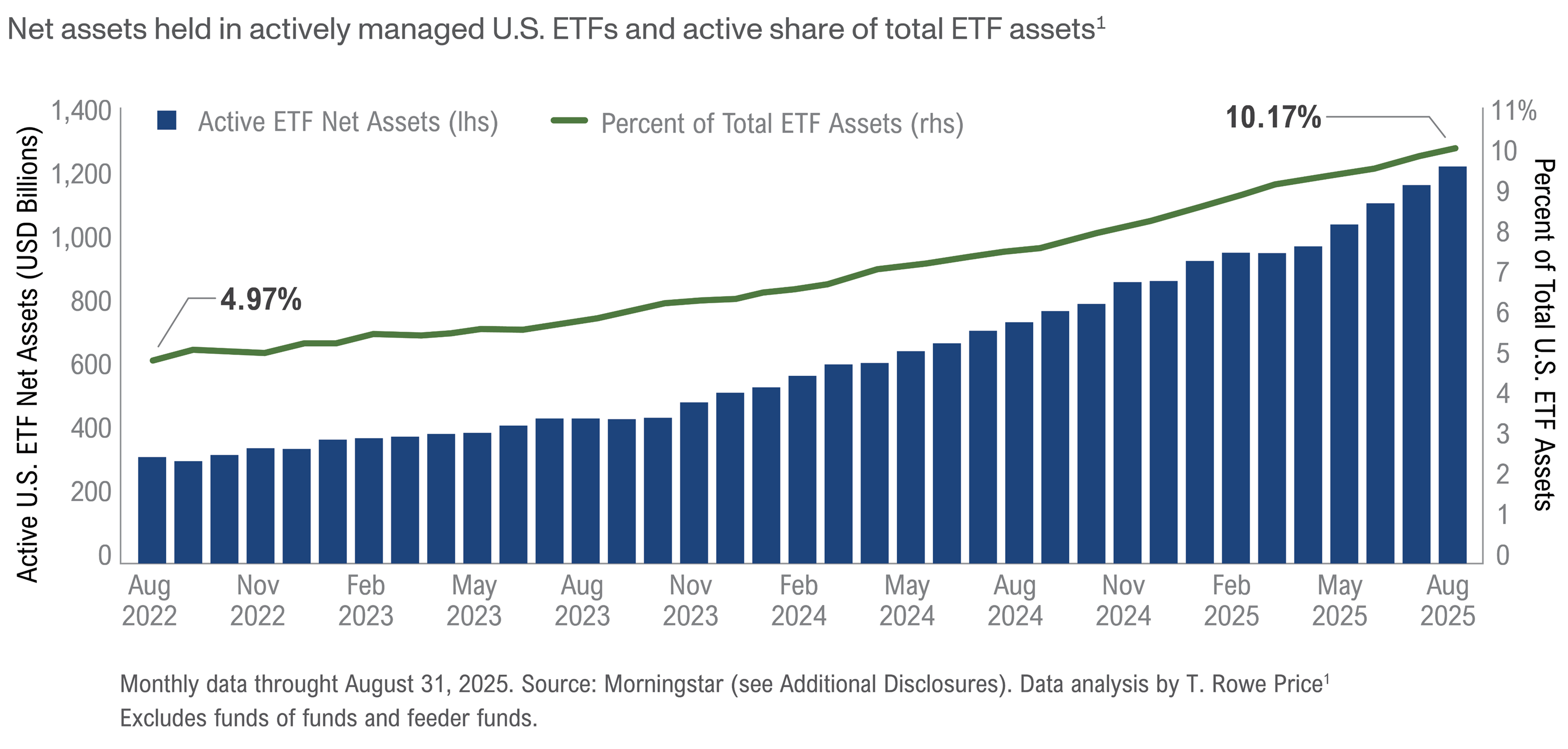

In 2025, the U.S. ETF market set a staggering record with $1.47 trillion in total net inflows. Active ETFs were the primary catalyst for this expansion, capturing over $450 billion in U.S. net inflows – accounting for roughly 30% of all ETF flows despite representing only 11% of total U.S. ETF assets. On a global scale, active ETF assets surged to $1.92 trillion by year-end, representing a 64.5% increase from $1.17 trillion in 2024. This momentum was underpinned by $637 billion in global net inflows, the highest annual total on record. The industry’s tilt toward active management was further evidenced by product development: roughly 1,000 ETFs launched in 2025 and active funds accounted for over 85% of all new ETF entrants, (see Figure 1).

Figure 1. Active ETFs are Growing Quickly

These developments reflect a structural shift. If the first three decades of ETF evolution were defined by the wrapper itself, that wrapper has become table stakes. What matters more today is how it is used – and the outcomes it makes possible.

What’s Driving Adoption: Transparency, Flexibility, and Outcomes

Even as many active managers struggled to retain assets in prior years, investors never abandoned active decision-making. Allocating to a market index ETF, after all, is itself an active portfolio decision. As major indices have become more concentrated, reflecting market dynamics and the scale of passive flows, the decision to remain fully invested in them, or seek alternative diversification, has taken on even greater weight.

Market concentration has coincided with widening dispersion across companies, sectors, and asset classes. In 2025, dispersion created a more favorable environment for active managers: only 54% of large-cap active equity funds underperformed the S&P 500 Index in the first half of the year, the best showing since 2022. In small- and mid-cap equities, more than 70% of active managers outperformed their benchmarks.2 Such conditions expand the opportunity set for skilled managers, but they also raise the stakes for advisors. A set-it-and-forget-it allocation to broad passive exposures may appear low-risk based on tracking error, yet conceal a wider range of potential outcomes. In this setting, the active ETF has emerged as a purpose-built vehicle. The same liquidity, transparency, and tax efficiency that drew advisors to passive strategies have supported the transition back to active ones. Advisors are using ETFs to construct more risk-managed core exposures, manage duration and credit flexibility, and enhance income generation and volatility management.

Transparency illustrates the shift. The ETF creation and redemption process means that holdings are disclosed regularly rather than only at quarter-end. For years, many active managers resisted the structure, fearing that, particularly in less liquid segments, others could front-run the manager’s trades. Over time, advances in data and analytics made clear that much of this information was already inferable to sophisticated market participants.

The active ETF structure helped level that asymmetry. By making holdings explicit and systematically available, ETFs allowed markets to price active decisions openly. Strategies became more transparent for advisors and clients, with better visibility into overlap and risk. Across markets, the emphasis shifted away from “hot stocks” toward portfolio construction and risk budgeting.

Carving Your Edge: The Advisor Mindset in 2026

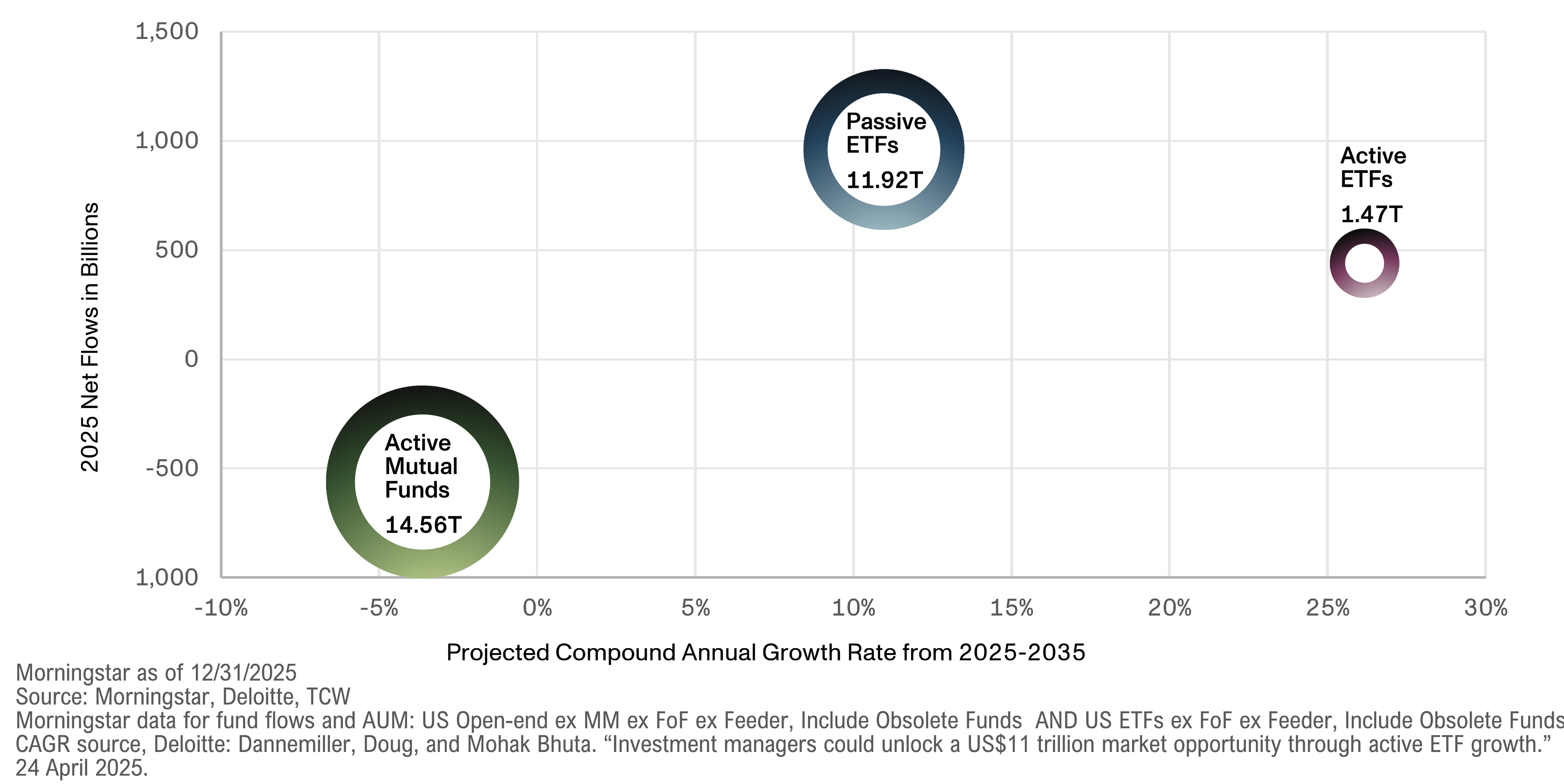

A high-concentration, high-dispersion market driven by dominant macro themes demands greater precision and conviction (see Figure 2).

The principle applies across asset classes. While a large share of active ETF flows in 2025 were equity-based, viewing active ETFs as primarily an equity phenomenon misses the bigger picture. Active ETFs first gained traction in fixed income. They address the structural reality of fixed income markets – the impracticality of replicating benchmark exposures one-for-one and the value created by selectively deviating from them. In fixed income, active ETFs attracted $238 billion in global net inflows in 2025.3 This strong demand reflects the structural realities of bond markets, thousands of securities, limited liquidity, and meaningful inefficiencies that reward skilled active management. Over the long term,4 active fixed income ETFs have delivered stronger risk-adjusted returns than their passive counterparts, particularly during periods of rising interest rates and market stress.

Looking ahead to 2026, three factors suggest continued opportunity for active fixed income: tight credit spreads that require security selection, Fed policy uncertainty that rewards dynamic duration management, and persistent market complexity that passive strategies cannot navigate effectively.

Figure 2. Where Industry Growth is Concentrating

As investors’ demand for yield has grown, it is likely not a coincidence that the 39% of active ETF flows directed toward fixed income in 2025 mirrors the traditional 60/40 framework.

Active equity ETFs represent a related evolution. The early growth of whole-market ETFs was followed by factor and thematic products that offered investors more control over exposures. As macro shifts and style rotations intensified, many investors discovered they were exchanging one form of passive risk for another. In 2025, only 31% of active U.S. large blend equity managers outperformed their benchmarks, but in more targeted strategies, such as small cap value or international equity, active managers fared significantly better. These outcomes reflect the growing dispersion in stock returns and the limitations of market- cap-weighted passive strategies, which are increasingly concentrated in a handful of mega-cap names.

In such an environment, managing through cycles requires active decisions at both the manager and portfolio-construction levels. Increasingly, this has meant more deliberate construction of building blocks and closer attention to how exposures interact within the portfolio. Active ETFs offer the transparency, liquidity, and tax efficiency of the ETF wrapper, while enabling advisors to express high-conviction views and manage risk with greater precision.

Institutional Active Management, Modern ETF Delivery

Against this backdrop, the most successful outcomes often start with thoughtful origination. TCW brings decades of active management experience to the ETF wrapper. The firm initially built its reputation in fixed income and has selectively expanded into equity and alternative strategies, maintaining an emphasis on research depth, discipline, and risk management. That philosophy now finds expression in an ETF lineup designed for defined portfolio roles.

Active ETFs entered the firm’s product set when many investors still viewed the structure with skepticism. Today, a robust creation and redemption infrastructure supports strategies designed for liquidity, tax efficiency, and integration into broader portfolios.

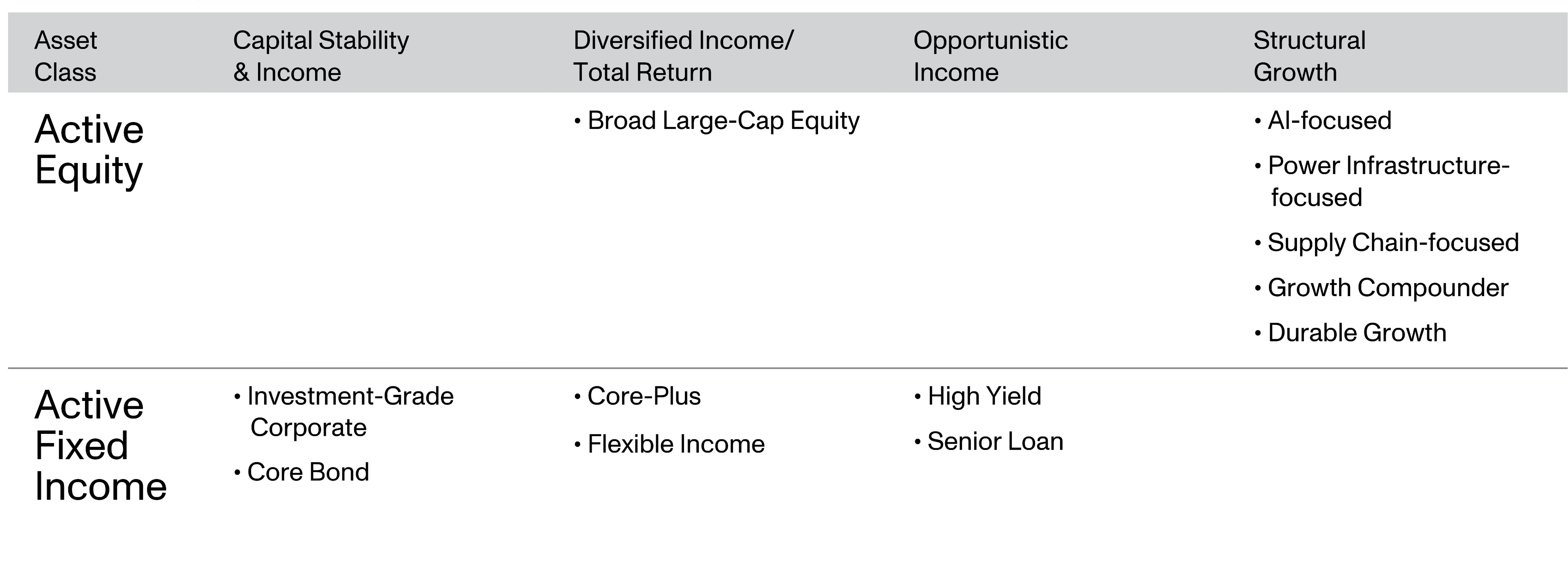

Designed as an integrated toolkit, TCW’s active ETF lineup spans core income, diversified credit, and structural equity growth, (see Figure 3.)

Fixed income remains a foundation. With rates on an uneven path, spreads tight in places, and opportunity concentrated in segments such as mortgages and asset-backed securities, deep sector expertise and flexibility across duration and credit have become central to anchoring portfolios.

The equity lineup follows a similar and complementary logic. In a market shaped by AI-driven concentration, diversification does not necessarily require abandoning a dominant theme. It often means understanding where structural constraints and counterbalances reside within that theme.

As demand for AI compute continues to grow, power remains a binding constraint cutting across platforms and competing architectures. Regardless of which models, chips, or ecosystems ultimately prevail, they all require power. Combining active exposure to AI innovation with active exposure to power infrastructure providers allows one set of more structurally stable return drivers to help offset the inherent variability in another.

Expressed through active ETFs, these combinations can produce portfolios more closely aligned with the real-world economic forces shaping markets – forces that broader thematic vehicles often struggle to capture.

Figure 3. A Purpose-Built Active ETF Platform

The Road Ahead: Active ETFs Become Core

Active ETFs are no longer simply a structure, they are a tool for deliberate portfolio design. As markets become more concentrated and dispersion persists, advisors need flexibility and precise exposures without sacrificing transparency or liquidity. In that environment, active management delivered through ETFs is becoming core to how portfolios are built.

1 FactSet, “U.S. ETF Summary: December and Full Year 2025 Results,” January 8, 2026. Available at: https://insight.factset.com/u.s.-etf-summary-december-and-full-year-2025-results (U.S. ETF assets: $13.5 trillion at year-end 2025)

2 SPIVA U.S. Mid-Year 2025 Scorecard by S&P Dow Jones Indices

3 ETFGI, “ETFGI reports Actively Managed ETFs Hit Record US$1.92Tr as 2025 Marks Highest Ever Inflows,” January 22, 2026. (Active fixed income ETFs: $237.93 billion in year-to-date inflows)

4 Journal of Beta Investment Strategies, “Active vs Passive Fixed-Income ETFs in the United States,” July 2025.

Before investing you should carefully consider a fund’s investment objectives, risks, charges and expenses. This and other information is in the prospectus, a copy of which may be obtained from etf.tcw.com. Please read the prospectus carefully before you invest.

Investing involves risks and the possible loss of principal.

Fixed income investments entail interest rate risk, the risk of issuer default, issuer credit risk, and price volatility risk. Funds investing in bonds can lose their value as interest rates rise and an investor can lose principal. Equity securities are subject to changes in value, and their values may be more volatile than those of other asset classes. The net asset value of the Fund will fluctuate based on changes in the value of the equity securities held by the Fund.

DEFINED TERMS

Duration – A measure of the sensitivity of the price (the value of principal) of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Rising interest rates mean falling bond prices, while declining interest rates mean rising bond prices.

Alpha – A measure of active return on investment in excess of benchmark index.

Correlation – A statistical measure of how the prices or returns of two or more securities (or portfolios) move in relation to each other. A negative correlation between returns of two securities implies that if the first security is generating positive returns then the second security would be expected to generate negative returns.

TCW ETFs are advised by TCW Investment Management Company, LLC. Distributed by Foreside Financial Services, LLC.