Can Nontransparent ETFs Save Active Mgmt?

New ETF structure could give actively managed strategies a much-needed boost.

“If you’re a mutual fund warehouse, you’re trying to figure out how to grow your business without giving away your secret sauce.” —Nichole Kramer, Manager of ETFs, ALPS

Most investors know the story by now: Actively managed stock mutual funds have bled investor dollars while ETFs have raked in cash.

A lengthy bull market has helped mask active mutual fund outflows, but fund companies are well aware of what is really going on behind the scenes. They are rightly concerned about the future of mutual funds, which grows bleaker by the day.

Source: ICI

Enter nontransparent ETFs. Years in the making, the Securities and Exchange Commission (SEC) recently approved Precidian’s nontransparent ETF structure, ActiveShares. Some are labeling this the next big thing in ETFs.

According to Precidian CEO Dan McCabe: “For the first time, investors will be able to access actively managed ETFs that do not disclose their holdings on a daily basis, but trade and operate in a similar manner to other ETFs.”

“Other ETFs” refers to traditional ETFs, which are generally required to publicly disclose their security positions every single trading day.1 Mutual funds must only disclose holdings quarterly (and up to 60 days in arrears).

The daily transparency of traditional ETFs has dissuaded mutual fund companies from launching their flagship active equity strategies (think Fidelity Contrafund or American Funds Growth Fund of America) using the traditional ETF wrapper.

Daily Disclosure Concerns

Many active managers view daily disclosure as giving away their “secret sauce,” allowing other market participants to potentially reverse engineer their strategies and erode their “edge.” Fund managers are also concerned trades might be front-run (think high speed traders attempting to jump ahead of a fund manager’s large buy or sell orders, resulting in worse price execution for the manager).

This fear of daily disclosure has been enough to keep many of the largest fund companies from using the transparent wrapper. ActiveShares solves this problem by allowing the same quarterly disclosure as mutual funds, but providing the potential benefits of the ETF investment vehicle. From a mutual fund company’s perspective, it’s the best of both worlds.2

Source: Brown Brothers Harriman

If you don’t think daily transparency has mattered, consider the brand-name fund companies unwilling to launch their flagship equity strategies in a traditional ETF wrapper: Fidelity, T. Rowe Price, American Funds, Dodge & Cox, Franklin Templeton, Janus Henderson, American Century. As a result, transparent actively managed ETFs are only a sliver of the nearly $4 trillion ETF market—less than 1% (about $12 billion in assets).

Game Changer?

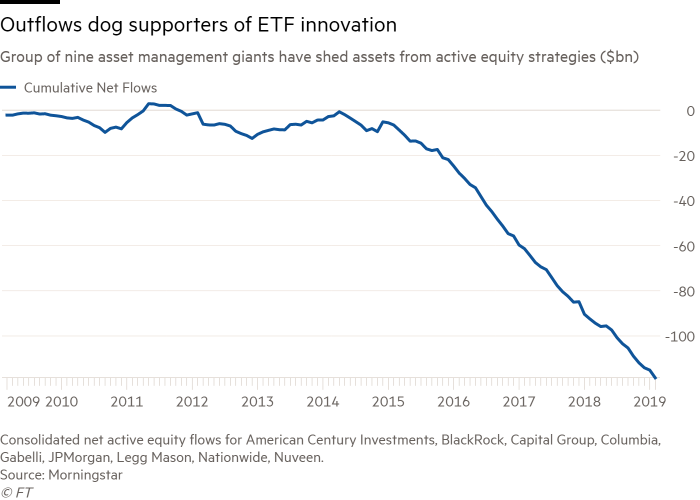

ActiveShares potentially changes the game for active ETFs. The following fund companies have already licensed ActiveShares from Precidian: Legg Mason, BlackRock, Capital Group, J.P. Morgan, Nationwide, Gabelli, Columbia and Nuveen. American Century has taken the additional step of filing for exemptive relief to launch ActiveShares ETFs. These same nine companies have watched investors pull billions of dollars from their actively managed stock mutual funds.

Source: Financial Times

The rationale for embracing ActiveShares is logical: If ETFs offer a superior investment delivery vehicle, and fund companies can also protect their “secret sauce,” this seems like a no-brainer. And, with lower costs and without the tax drag, perhaps active managers can close the performance gap or even—gasp(!)—generate more consistent outperformance.

“What we’re doing now is leveling the playing field for the active manager who can provide alpha, and allow him to bring his wares to the market,” Precidian’s McCabe said.

Model Still Faces Obstacles

Could nontransparent ETFs be the savior active management is so desperately seeking? Perhaps, but there are four potential roadblocks to salvation:

- Fund companies will have a difficult decision to make. Launching (likely) lower-cost ActiveShares ETFs competes directly with their mutual fund cash cows.3 Given the benefits of the ETF wrapper—especially tax efficiency—this puts fund companies in a slippery situation. As McCabe noted, nontransparent ETFs are now leveling the playing field. The ETF is a superior overall investment vehicle. This says everything about the challenge fund companies face adopting nontransparent ETFs. How will they market nontransparent ETFs? Will they basically say mutual funds are inferior? This challenge is why Matt Hougan, head of research at Bitwise and longtime ETF industry veteran, told Barron’s the rollout of ActiveShares is “one of the last steps in the dinosaur-ification of the mutual fund.” Are fund companies willing to help facilitate the extinction of their own mutual fund cash cows?

- Performance. The underperformance of active stock fund managers has been well-documented. I’m not going to regurgitate the stats (read about them here and here). Will ActiveShares help? It should. Fund fees and taxes eat into returns. Lowering both through a better structure should provide a boost. ActiveShares’ fees will still be higher than plain vanilla index funds. Can active managers consistently clear that fee hurdle, even if lowered? There is no question that since the financial crisis, the stock market hasn’t been ideal for active management. The S&P 500 has defeated nearly all comers. Could a different, more challenging market environment help shift the tide? Perhaps, though the data doesn’t support that idea. For any type of fund, performance dictates success. ActiveShares will need to have it.

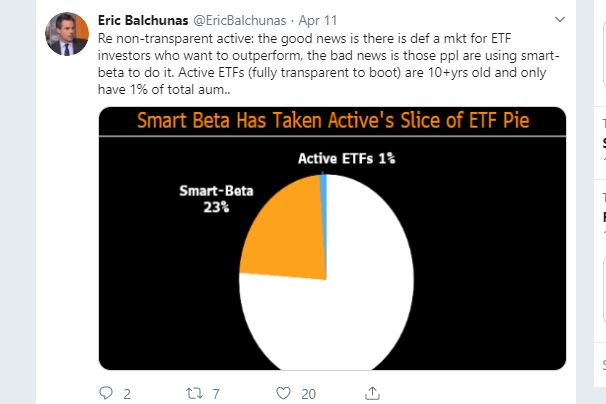

- Smart beta ETFs. Is active management being automated altogether anyway? Do investors even want human managers—who are subject to the same emotions and biases as all of us—picking stocks? Smart beta ETFs offer the automation of active management, using a rules-based approach in an attempt to provide higher risk-adjusted returns. Is this the future? We don’t know yet, but at a minimum, it’s an obstacle for traditional active managers.

- Complexity. The daily transparency of traditional ETFs helps authorized participants (APs) keep the price of an ETF in line with the value of its underlying holdings. Without that daily transparency, ActiveShares will use an AP representative or a “trusted agent,” who sits between APs and the ETF sponsor. The trusted agents will be the only players outside of the fund managers and custodians to know an ActiveShares ETF’s holdings and weightings. The trusted agents will perform creations and redemptions on behalf of APs using confidential accounts. There is some complexity involved here. Whenever a layer of complexity is added, the room for error grows. Concerns have been voiced over bid/ask spreads (think transaction cost: the difference in price between what an investor can buy and sell shares at) given that APs won’t know the exact underlying holdings. If bid/ask spreads are higher for ActiveShares, that could offset some or all of the fee and tax savings. Concerns have also been raised regarding insider trading (which the SEC has rebuffed). AP representatives will be under contractual obligation to not disclose holdings. Regardless, investor education will be needed to explain how these products work. The fund industry doesn’t necessarily have a reputation as a high quality educator. Morningstar’s Ben Johnson wonders who the additional complexity benefits, noting: “This solves the problem for asset managers, but it does little for the end clients.”

Why Transparency Wins

I still believe the best route for fund companies is to simply launch their flagship equity strategies using the transparent ETF wrapper. I previously laid out the case why. The bottom line is transparency equals trust. Since the global financial crisis, the investment world has been moving toward greater transparency, not less. Knowing exactly what your investments hold provides a level of trust.

From a portfolio management perspective, transparency helps avoid overlap of holdings (owning the same securities in multiple funds) and allows the monitoring of style drift (a manager drifting from its stated investment objective).

As it relates to manager fears of divulging their “secret sauce” and trade front-running, I have spoken with numerous active managers using the transparent ETF wrapper. I consistently hear the same message: These fears are overblown. The fact is there are currently active managers generating outperformance using the traditional ETF structure.

Also, let’s assume a manager’s strategy can be reverse engineered. Who is going to copy it? Is it a fund company wanting to launch the exact same strategy? Why would they do that? Even if they do, can they stick with the strategy? How similar will it really be? This is easier said than done. Is an individual investor going to steal the secret sauce? If so, does it matter?

ETFs The Future Of Active

So what actually happens? We know ETFs are where the future growth lies in the asset management space.

“We have launched one mutual fund in the last 18 months, but we’ve launched many more ETFs—and we’re a traditional mutual fund company. And I think that is a common experience,” said Joe Sullivan, CEO of Legg Mason.

All signs point to active ETFs as the likely candidate for higher rates of future growth. Cerulli found 37% of fund managers are planning to develop active ETFs and 22% nontransparent ETFs, compared with 18% for passive and 11% for strategic beta.

For a larger view, please click on the image above.

Source: Cerulli

For investors currently owning traditional active stock mutual funds, converting to nontransparent ETFs might make sense. Investors won’t lose anything, and they will likely gain lower costs, tax efficiency and intraday trading. Perhaps that will be enough to ignite nontransparent ETFs.

But what if fund managers offering transparent active ETFs are able to deliver a similar performance track record? If investors can get the exact same experience—with more transparency—why wouldn’t they do that?

Whichever direction fund companies choose—transparent or nontransparent ETFs—they are going to cannibalize their existing mutual fund business. That’s a fact. My preference is to see investment strategies delivered in the most investor-friendly format. But as I mentioned earlier, ultimately, performance will hold the key.

If there is some credence to the “secret sauce” and “front-running” arguments, that should show up in the numbers. If performance doesn’t materialize, nontransparent ETFs will have a short life span. And, regardless of whether transparent or nontransparent, active has to continue battling the major head wind posed by passive investing.

“I appreciate the point that, early on, ETF growth was all about passive management, but we see active ETFs as the next stage in the evolution of the business,” said Rick Genoni, head of ETF product management at Legg Mason.

I agree, but transparent or nontransparent active ETFs? Investors will ultimately decide.

1Everyone except Vanguard, whose ETFs are a share class of existing mutual funds, and disclose holdings monthly.

2Note the SEC approval limits ActiveShares ETFs to securities traded on U.S. exchanges during the same time as the ETF.

3In addition to launching stand-alone ActiveShares ETFs, there’s discussion surrounding whether mutual fund companies can simply convert an existing mutual fund into an ETF. Blog for another time.

Follow Nate Geraci on Twitter @nategeraci