Hunt For ETF Flow Signals Dangerous

Recent stories suggesting you can extract signals from ETF flows are full of holes.

Recent stories suggesting you can extract signals from ETF flows are full of holes.

Recent stories suggesting you can extract signals from ETF flows are full of holes.

Bob Pisani has a blog out this morning talking about recently published work by Deutsche Bank Markets Research suggesting ETF flows can be in some way predictive of future performance. I once again find myself having to jump on the caveat train on ETF flows, but this time I thought I’d point out a few missed nuances.

First, let me say that the folks at DB do great work, and I encourage folks to read the actual note published on July 2. And true nerds may want to dig into the methodology of their Tactical Asset Allocation Relative Strength Signal (TAARSS) process, which they published in May.

I fear the enormous level of detail put into the process by DB is going to be largely lost in the media headlines, which all seem to sum it up as: “ETF Flows Have Predictive Value.”

In fact, the original DB work goes to great length to point out all of the ways in which a naive read of ETF flows can lead investors astray, including:

- Create-to-lend activity, which is common in rapidly declining sectors

- Create/redeem to cover activity, which is how large investors unwind short ETF positions

- Rebalancing trades, which are when the issuer works with major institutions to help unload and acquire large blocks of securities through the creation/redemption process

- Seasonal effects, such as tax loss harvesting

Their methodology attempts to correct for these issues, largely by removing ETFs they deem not to be used by serious asset allocators. After all, the whole point of looking at ETF flows for signals is to be able to say “Aha! Money is flowing into small-cap financials, and we think more money will CONTINUE to flow into small-cap financials, so if we buy now, we make money!”

The unfortunate side effect is that DB deliberately excludes products definitely used by plenty of long- term, buy-and-hold investors—the SPDR S&P 500 ETF (SPY | A-98) and all of the Select Sector SPDRs. The end results, however, certainly look impressive.

Page after page of the methodology shows positive returns for their various flavors of strategies that rotate in and out of countries, sectors or commodities based on their cleaned-up ETF flow signal.

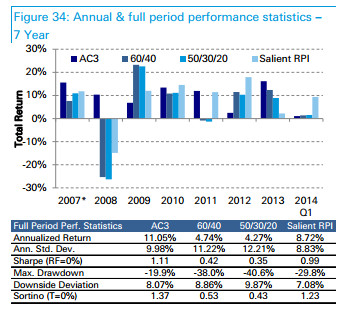

This chart, from the big report they published in May, highlights their most successful strategy, which rotates between asset classes based on ETF flows. It compares the strategy (AC3) to different passive portfolios and Salient’s Risk Parity Index.

Honestly, that part is unsurprising; very few papers get published that show how badly a signal or factor theory works. Academic finance is fundamentally about manipulating data and algorithms until something looks shiny in the rearview mirror.

What’s more surprising is that the data set the models use all start in mid-2007, and most of the positive returns for the headline sectors get their “juice” by being in the right place during the worst of the financial crisis.

It’s not that I don’t believe them—I actually do believe them; they do good fundamental work. There’s some data I’d love to see that for some reason often gets omitted in nonpeer-reviewed work, like beta and statistical significance, but those are relatively normal quibbles I make on work like this.

My bigger concern is this: Here we have one of the largest asset managers in the world with some of the smartest people, and deepest access to data, and in order to create a backtested model that makes ETF flows relevant, they have to torture the data, removing the largest ETFs, making broad assumptions about what’s relevant and what’s not, and then create a rather complex model to correct for the enormous amount of noise present in the data.

That’s dangerous, because it leads investors to conclude, “Hey, I can try this at home.” I think it leads people into the tenuous waters of thinking they can be “smarter than the herd,” getting in just at the right time to catch a wave, and getting out before the party’s over.

Wall Street is littered with the corpses of investors who thought that time and time again. DB (and frankly a whole slew of flow-followers on Wall Street) is doing solid work trying to separate the signal from the noise in pursuit of investment returns, and I can’t argue with either the process or the intent.

But this is noise I stare at every day, and I remain extremely skeptical that anyone is going to eke out a long-term performance advantage chasing ETF flows on the highway in front of us, whatever the rearview mirror might suggest.

At the time this article was written, the author held no positions in the security mentioned. Contact Dave Nadig at [email protected].