Nadig: Trading Gold ETFs The Right Way

Look really closely at the price of an ETF before you trade it.

Look really closely at the price of an ETF before you trade it.

Look really closely at the price of an ETF before you trade it.

There’s one statistic that’s absolutely crucial to effective ETF trading, and pretty much nobody ever talks about it. Handle.

The “handle” of a security is the left-hand side of the price. In the old days, when stocks were quoted in fractions, you’d see IBM quoted as “10 1/8,” with “10” being the handle. There was a time when the first electronic quote services were coming out—I used to get quotes on an actual mobile Quotron pager—where bandwidth was at such a premium that the systems didn’t even display the handle. They’d simple show the part that was different on the bid and ask side.

So for example, if stock was bid 50 1/8 by 50 ½, the quote might simply come through as “1/8 – 1/2” and you, the trader, were expected to know that the handle was 50.

Why in the world does any of this matter to an ETF trader in the modern, high-bandwidth, decimalized market? Because when comparing two ETFs, handle is often the biggest determinant of how well you’ll be able to trade with frequency and size.

Consider two investors interested in gold.

One wants to hold for a year, the other is just looking for a short term hedging vehicle. As good ETF investors, they’ve both been trained to pay a lot of attention to expense ratios—after all, it’s one of the only knowable predictors of your return, right?

The two biggest ETFs are the SPDR Gold Trust (GLD | A-100), with an expense ratio of 40 basis points, or $40 for each $10,000 invested, and the iShares Gold Trust (IAU | A-100), with an expense ratio of 25 basis points. Like IAU, Axel Merk’s innovative new gold bullion ETF also has a small handle, which could help it gather assets in its early phase.

In any case, both GLD and IAU—as evidenced by their perfect scores in our analytics engine—reliably do exactly what you want them to do, and the do it efficiently and with high levels of tradability. But there’s a 15-basis-point difference in expense ratio. Imagining our two investors want to put $1 million to work—they’ll save $15,000 a year in IAU!

Well, not so fast. There’s another expense at work here—trading costs.

And that’s where handle comes into play. Looking on screen, both of these ETFs trade as tight as the market allows them to—a penny wide, all day, every day, with rare exceptions. But a penny on IAU’s price of $12.55 is a whole lot more than a penny on GLD’s price of $124.65. That’s why we always suggest that people think of their trading costs not in dollar terms, but in percent terms.

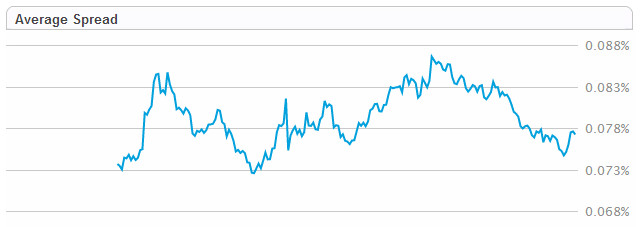

That’s how we display it in our system. Here’s the rolling spread chart for IAU:

You can see that on a percentage basis, IAU has a spread of roughly 8 basis points, or 0.08%.

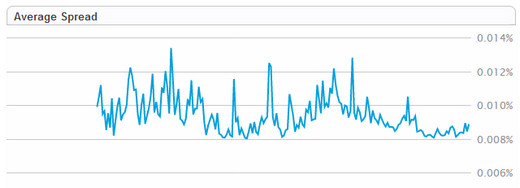

Here’s the same chart for GLD:

GLD’s average spread is actually less than 1 basis point. That’s because that large handle makes a penny relatively meaningless.

The 7-8 basis point difference in spread makes the decision of which near-perfect gold ETF to buy slightly more complicated. Our one-year holder is still better off in IAU, but he’s not $1,500 better off, he’s only $750 better off, because he’s going to pay more in spread going in and out of his position.

Our day trader, on the other hand, just needs to be confident he’s holding less than six months. Any window shorter than that, and he’s saving substantially solely because of GLD’s larger handle. If he’s in a brokerage arrangement that charges him by the share to trade—which is still not that uncommon—he’s saving even more money with a big handle.

So, if handle matters so much, why don’t ETFs trade with $1,000 handles?

For the obvious reason that it makes trading unwieldy.

Most investors are looking not for a certain number of shares, but to put a certain amount of money to work. If I want to put $2,500 to work, having a $1,000 handle means I’ll end up either over- or underexposed.

Even at the $125 handle, GLD might be too “chunky” for a retail investor; hence iShares’ decision to keep a low $12 handle on IAU. That makes for a nice accessible trade for everyone.

It’s worth noting that handle is a product design choice, not an accident, and ETF issuers can and do adjust handles all the time—by splitting or reverse-splitting their shares.

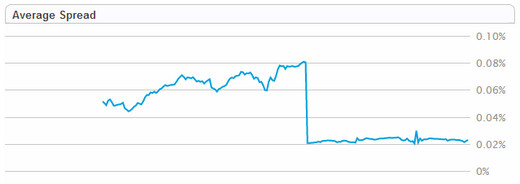

Consider what happened to the spreads of the iPath S&P 400 VIX Short-Term Futures ETN (VXX | A-54) when it did a 1-4 reverse-split last fall:

In short: instantaneous savings for anyone trading VXX with any frequency. And in a product like VXX, I certainly hope it was traders, not long-term investors, driving the flows.

The moral of the story here is simple: Look beyond the expense ratio when selecting your ETF, and always consider the impact of handle on your true costs.

At the time this article was written, the author held no positions in the securities mentioned. Contact Dave Nadig at [email protected].