Scots Not Pounding The Pound, It’s Yellen

Today the news is full of stories about the collapsing pound. Not so much.

Today the news is full of stories about the collapsing pound. Not so much.

Today the news is full of stories about the collapsing pound. Not so much.

With a vote on Scottish independence looming next week, and major Scottish financial firms swearing they’re headed for London if Scotland becomes, well, the land of Scots, the pound’s being, and will continue to be, hammered. At least, that seems to be what the breathless newswires are saying.

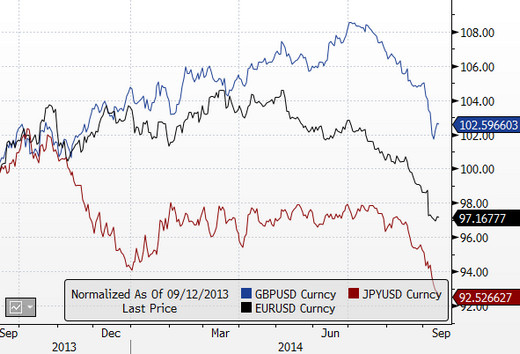

Actually, that’s not really what I see going on. Consider the chart of the three major currencies over the last year:

I’ve normalized all of these to 100 at the beginning of the period, but notice something here? All three are in lock step since the summer. All of them are down substantially against the dollar.

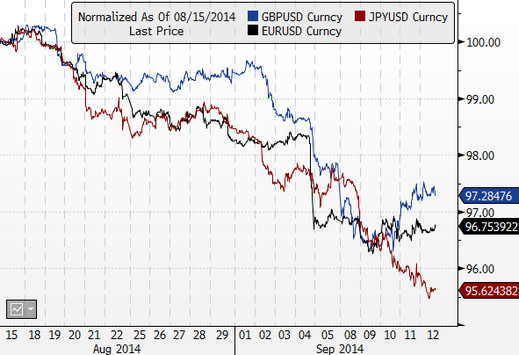

And while, yes, the pound has had a bad run the last few weeks with the news of Scottish independence, half the coverage I read seems to ignore the relative performance of other currencies in the same period. In fact, look at how the big three have done just in the past few months:

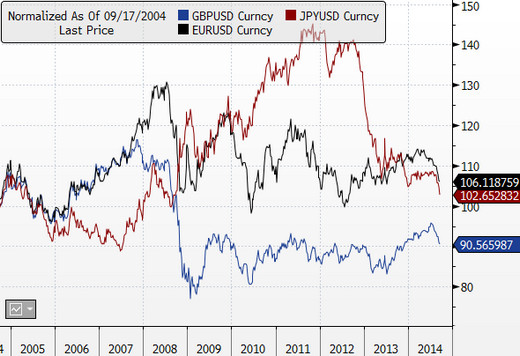

Yes, the pound is down just under 3 percent, but the euro is down more, and the yen is down far more. And in fact, the pound’s rallying right now. If we take the long view, going back 10 years, the pound remains horribly depressed and below its long-term averages, suggesting, perhaps, it’s due for more recovery:

Of course, that kind of talk, about “normal” and “due” is really “chart-speak,” and I don’t generally truck with such things. I’m more of a “what’s the story?” kind of guy. And the story remains a strong dollar more than anything else.

Here’s What’s Going On

In fact, what’s really going on here, in my thinking, is a referendum on Janet Yellen.

Next week’s FOMC meeting is critical to the market’s perception of U.S. interest rates. Boston Fed President Eric Rosengren suggested yesterday that the Fed should stop giving any forward guidance on interest rates, changing a policy that’s been in place since the financial crisis of spoon-feeding the future to the markets.

Despite all the handwringing of Republicans, the reality is that unemployment—now the favorite Fed bogey—is down to 6.1 percent, which is surprisingly healthy. While they’d like their magical 2 percent inflation target to be solid as well, all signs are pointing toward rising rates, and perhaps with unpredictable timing.

The stock market may end up hating that, but the currency markets would love it. After all, interest rates are one of, if not the key, differential in currency investing.

The time-honored carry trade is “borrow the low-interest-rate currency to invest in the high-interest-rate currency,” and it’s been the dollar on the short end of that stick for a long, long time. With even a minor uptick in the rate paid on U.S. Treasurys, cash will flood into the dollar, making it even stronger.

So what’s with the Scots then? Really, the currency market has one major concern. If in fact Scotland spins off like a subsidiary, what will that new country do about British sovereign bonds? The U.K. finances itself with gilts as much as any other industrialized country, and those debt obligations have been backed by the economy of a unified Great Britain.

If the new Scotland were to tell Old England to shove off, leaving England and Northern Ireland holding the bag on debt, well, that makes England a lot less noble of a credit. While I don’t predict a British bankruptcy in my lifetime, it’s still not great for the balance sheet of the remaining U.K.

There’s a lot of water to pass under that bridge, however, and no firm idea how a split Scotland would even happen.

The FOMC meeting, however, is a sure thing.

Contact Dave Nadig at [email protected] or follow him on Twitter @DaveNadig.