The ‘Stock Picker’s Market’ That Wasn’t

Active management failed to bounce back in the first quarter.

Todd Rosenbluth is director of ETF and mutual fund research at CFRA.

While 2017 was supposedly set up as a U.S. stock pickers’ market—with a new president, a Federal Reserve poised to raise rates and expectations of higher stock dispersion creating opportunities to spot winners—it is not looking good so far.

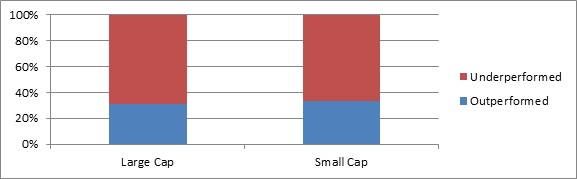

Just 31% of large-cap core mutual funds ended the first quarter beating the S&P 500 index’s total return, while 33% of small-cap core funds bested the Russell 2000 Index.

Naturally, investors should not make a decision based on just one quarter of performance. Yet given the ongoing shift of assets to passive, the 0.61% lag in the return of the average large-cap core fund will not help to stop the asset bleeding.

Part of the underperformance stems from the 1.1% average net expense ratio for the mutual funds in contrast to a free index. However, investors in these funds could have earned a 5.92% return with the SPDR S&P 500 ETF Trust (SPY) or the iShares S&P 500 (IVV) for modest fees of 0.09% and 0.04%, respectively, and seek to replicate the index.

2017: Year For Active Management?

% of Mutual Funds Outperforming S&P 500 & Russell 2000 Indices

Source: CFRA Research

Some Cheap Funds Outperform

Not surprisingly, some of the outperforming active large-cap core funds this year—and there always are some—include products with below-average expense ratios. CFRA five-star ranked Vanguard PrimeCap Core Fund (VPCCX) and four-star American Funds Fundamental Investors (ANCFX) have 0.46% and 0.60% net expense ratios, and rose 7.44% and 6.60%, respectively, in the first quarter, ahead of the 5.49% peer average.

VPCCX outperformed its peers in the last four calendar years, and at year-end was heavily weighted toward information technology (28% of assets) and industrials (19%), such as Southwest Airlines and Texas Instruments. Unfortunately, for those seeking out strong active management, the fund is closed to new investors.

However, ANCFX is open, and outperformed its peers in three of the last five calendar years. The fund’s largest sector exposure, information technology (21% of assets), is aligned with the broader index. Rather, the fund’s stock selections are differentiated, with Broadcom among its top-10 holdings, and not Apple.

But with fewer than one in three large-cap core funds beating the index, even some funds with a moderate fee are lagging. AB Relative Value and Oakmark Select Fund were up 3.25% and 3.0%, respectively, in the first quarter, despite expense ratios below 1.0%.

Equal Weight Worked For Some Funds

Some investors may have wanted an index-based strategy differentiated from the market-cap-weighted S&P 500 Index, and in some cases, the start of 2017 has been good to them. The PowerShares Russell Top 200 Equal Weight Portfolio ETF (EQWL) was up 6.88% in the first quarter, aided by its diversification. Exposure to health care (17% of assets) included strong performers Allergan and Amgen. However, EQWL has just $37 million in assets.

However, the $13 billion Guggenheim S&P 500 Equal Weight ETF (RSP) was up just 5.23%, despite also using an equal-weighting approach. Although, as is common when the names are similar, the underlying exposure RSP provides is different. RSP has less in technology and more in utilities than EQWL.

While a lot of the attention in the active/passive discussion resides in the large-cap style, investors in small-cap funds would have been better selecting the iShares Russell 2000 ETF (IWM), up 2.24% this year, than with the 1.87% return for the average small-cap core mutual fund.

However, despite IWM’s relatively strong record this year, CFRA has valuation and risk concerns for many of its holdings and also sees bearish technical trends. CFRA ranks approximately 1,000 equity ETFs on a daily basis independently from mutual funds.

High Fees Can Be A Drag

Similar to large-cap funds, part of the challenge for investors is that the high fees can be a drag, as the average small-cap core fund has a 1.27% net expense ratio. Further, performance success can materialize from products with middling recent records.

Prudential Jennison Small Company Fund (PGOAX) and Royce Premier (RYPRX) are two strong performers this year, rising 6.27% and 6.71%, respectively. However, both PGOAX and RYPRX underperformed the small-cap core peer group in four of the five last five calendar years, a reminder that past performance is not indicative of future results. They each have moderately below-average net expense ratios, but are constructed differently.

All About Stock Selection

PGOAX’s sector exposure is relatively similar to IWM, but has benefited this year from stock selection. Recent top-10 holdings include Global Payments and Vail Resorts. In contrast, RYPRX recently had a hefty 36% stake in industrials, such as Copart. CFRA ranks approximately 8,000 domestic equity mutual fund share classes with a star based on a combination of performance metrics, holdings analysis and cost factors.

Even as the above suggests investors might want to look more closely at passive ETFs, figuring out which of those can generate performance success is a challenge if only performance records were used.

For example, the Vanguard Small-Cap Index Fund (VB), tracking a different CRSP index with a higher weighted average market capitalization than IWM, underperformed its peer by 3.14% in 2016. In the first quarter, VB was ahead by 1.45%. VB is ranked ahead of IWM by CFRA Research, in part due to its lower expense ratio and stronger technical trends. There are also small-cap core ETFs from a range of providers that perform differently than IWM and VB.

As many active funds seek to regain their relative footing in the remaining months of 2017, investors should look beyond one period of performance when sorting through the universe.

At the time of writing, neither the author nor his firm held any of the securities mentioned. Todd Rosenbluth is director of ETF and mutual fund research at CFRA, an independent research firm that acquired S&P Global Market Intelligence's equity and fund business in October 2016. He can be reached at [email protected]. Follow him at @ToddCFRA