Investors Pour $25B Into Semiconductor ETFs as DRAM Plunges 40%

Chip funds have plunged since June 22, but the money keeps coming in.

Semiconductor stocks ripped higher through the second quarter. Then the third quarter started, profit-taking kicked in, familiar worries about the AI trade resurfaced, and the whole group rolled over.

ETF investors have responded by buying with both hands.

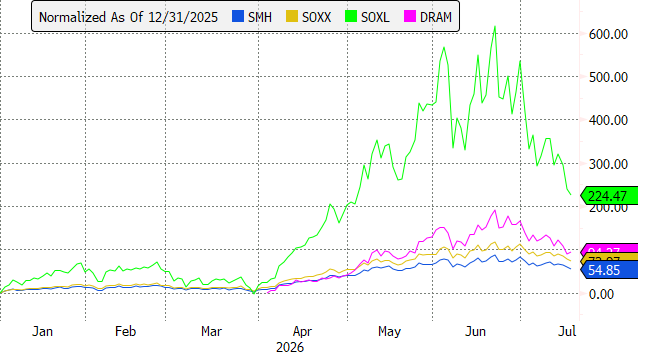

The big semiconductor ETFs peaked on June 22. Since that date, the Roundhill Memory ETF (DRAM) has fallen from 80.72 to an intraday low of 48.64 on Friday, a drop of nearly 40%.

The iShares Semiconductor ETF (SOXX) lost 24% over the same stretch and the VanEck Semiconductor ETF (SMH) lost 20%. The leveraged Direxion Daily Semiconductor Bull 3X Shares (SOXL) fell 61%.

All four have taken in enormous amounts of money anyway. DRAM pulled in $8.8 billion, SOXX $8.5 billion, SOXL $5.1 billion and SMH $2.3 billion, a combined $24.7 billion in under a month.

The DRAM figures highlight just how forceful the buying has been. The fund lost close to 40% of its value, yet the amount of money invested in the fund sits at $23.4 billion today, only a touch below the late-June peak of $25.9 billion. Inflows have almost entirely offset the market losses.

High Flyers Retreat

The hardest hit semiconductor stocks have been the ones that ran the furthest. Micron Technology, one of the biggest beneficiaries of high bandwidth memory demand, Marvell Technology, which sells custom AI silicon and optical interconnect products to hyperscalers, and the semicap giant Applied Materials have all given back a large chunk of their gains.

There is a simple explanation for what happened. These stocks went up an extraordinary amount in a short amount of time, and some of the air came out.

At its high, SOXX was up 118% year to date, SMH was up 86%, and DRAM, which only launched in April, was up 191%. The 3x leveraged SOXL was up an incredible 616%.

Even after the pullback, all four remain solidly higher on the year.

Other Explanations

While profit taking is the simplest read, there are more elaborate explanations available for anyone who wants one.

Investors have questioned the sustainability of the AI buildout for a few years now, and even though capital expenditure budgets at the largest technology companies keep rising, the questions about whether it can all last resurface every few months.

More recently, the release of Kimi K3, a Chinese open source model that reportedly rivals US frontier models from Anthropic and OpenAI, has prompted comparisons to the DeepSeek episode in early 2025, when the prospect of cheap Chinese models briefly convinced the market that AI infrastructure spending would come down.

The concerns are real and worth considering. Nobody knows how much longer capex on AI infrastructure can keep climbing, and nobody knows what a credible open source frontier model does to demand for closed frontier models, and by extension to demand for the infrastructure underneath them.

The early read from analysts is that Kimi K3 is competitive on capability but not on cost per task, which complicates the picture.

Still, despite the concerns and the pullback, the broader bull case for AI infrastructure has not changed much, and flows suggest investors are treating the drawdown as a buying opportunity rather than a sign that the top is in.