Passive Investing's Risks Mount, Simplify's Green Says

Stock markets becoming vulnerable to crashes as passive investing boosts concentration in low-liquidity equities, Simplify's Chief Strategist Mike Green says.

If the growth of passive investing continues at its current pace the stock market will become vulnerable to a steep market crash, according to Mike Green, chief strategist and portfolio manager at Simplify Asset Management, which manages $5.7 billion across 30 U.S. ETFs.

“Everyone fancies they can get themselves out if the facts change. The problem is that is a bit like trying to leave a crowded concert through a single fire door when everybody else has the same idea,” he told ETF Stream in a recent interview.

Green is known for his work on market structure. His thesis, in simple terms, is that passive investing at scale is at best distortionary and at worst dangerous.

For Green, its rise has underpinned the increase in stock market concentration and by extension the outperformance of market cap-weighted strategies—the only truly passive investments, in his view. This outperformance has attracted yet more inflows driving even more extreme concentration—a vicious cycle.

We now sit at a dangerous point, he explained. With the pool of price conscious capital shrinking by the year, if passive inflows continue then equity valuations will climb sharply from current levels.

If these flows eventually reverse, “in the simplest terms that would cause a market crash,” Green warned.

Passive Flows Effect on Concentration

The obvious pushback is that a passive fund buys each stock in proportion to its weight in the index, therefore each stock should experience the same price impact. Concentration ought to be unaffected.

“Liquidity does not scale with market capitalization,” however, “it scales with the volatility and volume of trading activity,” explained Green.

Drawing on a Valentin Haddad paper covered by ETF Stream in 2022, Green asserted that the largest stocks in an index are also the most inelastic. Although Apple with a $3.6 trillion market cap is 36 times the size of a $100 billion stock, it may only be about five times more liquid, he said.

As a result, each price agnostic dollar flowing into passive strategies “causes, on average, the largest stocks to rise more and the smallest stocks to rise less”—increasing the levels of concentration.

Rising Passive Ownership

Estimates of ‘passive’ ownership levels vary widely, ranging anywhere from 15% to 50%. Green, perhaps unsurprisingly, is towards the higher end.

Drawing on recent academic research, Green surmised that “somewhere between 40% and 45% of total market cap is now traded in a passive framework, meaning market cap-weighted.”

The lower estimates can be disregarded because they simply add up ETFs and passive mutual funds and overlook segregated institutional mandates – a market of roughly equivalent size, he believes.

At what level does it become distortive?

The rise of passive investing is already starting to inflate equity valuations, according to Green, but valuations will rise much faster from here should inflows continue, creating a potentially precarious dynamic.

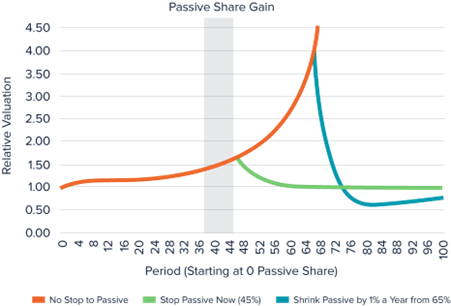

Green shared the below chart with ETF Stream plotting the share of passive ownership against relative equity valuations using the actual rate of passive adoption (the orange line).

Source: Mike Green

The green line shows that if passive inflows halted today, valuations would sink back to their starting point – painful but not a disaster.

However, if “passive ownership continues to grow at these rates and approaches a 65% share, you are talking give or take a 300% valuation increase and Shiller P/E ratios of 100.”

If passive redemptions were to occur at that point, as shown by the blue line, “what you have done is hollow out the universe of capital that can actually work against them in selling.

“Prices would rapidly get driven below fair value and probably never recover,” he predicted.

Active Managers' Pushback

A key counterargument is that the further valuations get forced from fair value, the greater the incentive for active managers to work in the opposite direction.

However, as Haddad identified in his paper, active managers have an imperfect ‘strategic response’ since they do not have unlimited access to leverage.

“By the way that is a good thing,” joked Green. “You do not want active managers with unlimited access to leverage. Those are components that cause things like a global financial crisis.”

Perhaps the most compelling pushback is that Green’s warnings about the dangers of passive investing are hypothetical. Indeed, there certainly is no historical precedent to draw upon.

If he is right, however, investors may look to diversify away from cap-weighted strategies well before the fire alarm goes off at the concert.

This article was originally published by etf.com sister publication ETF Stream.