Swedroe: Be Prepared For Losses

Understand the risk levels in your portfolio and how much you can handle.

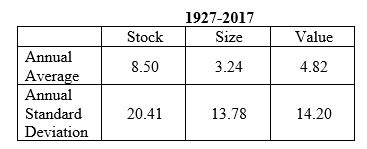

The stock premium—the annual average return of stocks minus the annual average return of one-month Treasury bills—has been high, attracting investors to the stock market. For the period 1927–2017, it averaged 8.5%. There have also been size (return of small stocks minus return of large stocks) and value (return of value stocks minus return of growth stocks) premiums of 3.24% and 4.82%, respectively.

However, the excess returns are generally referred to as risk premiums—they aren’t free lunches. We see evidence of that in the volatility of the premiums. The stock, size and value premiums have come with annual standard deviations of 20.41% (2.4 times the stock premium), 13.78% (4.3 times the size premium) and 14.20% (2.9 times the value premium), respectively.

Let’s take a closer look at some of the data that illustrate the riskiness of the premiums. For the period:

- The stock premium was negative in 27 of the 91 years (30% of the years). There were 17 years (19% of the years) when the premium was worse than -10%, 12 years (13% of the years) when it was worse than -15% and seven years (8% of the years) when it was worse than -20%. As another indicator of the volatility of the stock premium, we see that the gap between the best and worst years was 102.2%, more than 12 times the size of the premium itself. The worst year was 1931, when the premium was -45.11%. Given a premium of 8.5% and a standard deviation of 20.41%, this was more than a 2.5 standard deviation event. The best year was 1933, when the premium was 57.05%, also more than two standard deviations from the mean. In fact, we had six such two-standard-deviation events. We would have had just four if the returns had been normally distributed.

- The size premium was negative in 42 of the years (46% of the years). There were 10 years (11% of the years) when it was worse than -10%, three years (3% of the years) when it was worse than -15%, and three years (3% of the years) when it was worse than -20%. The worst year was 1929, when the premium was -30.8%, a 2.5-standard-deviation event. The best year was 1967, when the premium was 50.69%, more than a three-standard-deviation event. The gap between the best and worst years was 81.49%, more than 25 times the size of the premium itself. In five of the years, returns were more than two standard deviations from the mean.

- The value premium was negative in 35 of the years (38% of the years). There were 11 years (12% of the years) when it was worse than -10%, four years (4% of the years) when it was worse than -15%, and three years (3% of the years) when it was worse than -20%. The worst year was 1999, when the premium was -31.7%, more than a 2.5-standard-deviation event. The best year was 2000, when the premium was 39.69%, a 2.5-standard-deviation event. The gap between the two was 71.39%, 14.8 times the size of the premium itself. In six of the years, returns were more than two standard deviations from the mean. Even if we extend our time frame to five years, we see that there is still risk in the premiums. Using non-overlapping data, we have 18 five-year periods.

- In four periods (22% of the periods), the stock premium was negative. The worst period was 1927–31, when the stock premium was -46.76%.

- In nine periods (50% of the periods), the size premium was negative. The worst period was also 1927–31, when it was -30.92%.

- In five periods (28% of the periods), the value premium was negative. The worst period was 2007–11, when it was -32.27%. If we extend our time frame to 10 years, we have nine non-overlapping periods. There were no periods when the stock premium was negative, one period when the value premium was negative (2007–16, when it was -17.59%) and two periods when the size premium was negative (1947–56, when it was -29.95% and 1987–96, when it was -19.21%).

Further Evidence

Eugene Fama and Ken French examined the volatility of the three equity premiums we have been discussing in their December 2017 study “Volatility Lessons,” which covered the period July 1963 through December 2016. In addition to finding high volatility of stock returns, they also found:

- Skewness of returns is -0.53 for monthly equity premiums, so the distribution of monthly premiums is skewed to the left. (If a distribution is symmetric about its mean, Skew (the third moment about the mean, divided by the cubed standard deviation) is zero.) However, Skew is positive (0.25) for annual premiums and increases a lot for longer return horizons, to 3.78 for 30-year premiums. Increasing right skew means more of the dispersion is toward good outcomes (good news).

- Monthly equity premiums are “leptokurtic,” which means there are more extreme returns than we would expect with a normal distribution (the tails are fat). Kurtosis (the fourth moment about the mean, divided by the standard deviation to the fourth power) is 3.0 for a normal distribution, and 4.97 for monthly equity premiums. Kurtosis falls to 3.19 for annual premiums but then rises strongly for longer return horizons, to 32.37 for 30‑year returns. The combination of right skew and kurtosis means that outliers are primarily in the right (good) tail.

- The standard deviation of equity premiums increases with the return horizon, from 17% for annual premiums to 2551% for 30-year premiums.

- In general, the distribution of premiums moves to the right faster than its dispersion increases. For example, the median increases 231-fold, from 6% for annual premiums to 1390% for 30-year premiums. Together, increasing kurtosis and right skew for longer horizons spreads out the good outcomes in the right tail more than the bad outcomes in the left.

Fama and French noted that while most of the news about equity premium distributions for longer return horizons is good, there is bad news. They used the realized monthly returns from the period their study covered to construct long-horizon simulation returns, and found that for the three- and five-year periods that are often the focus of professional investors, negative equity premiums occur in 29% of three-year periods and 23% of five-years periods of simulation runs. Even for 10- and 20-year periods, negative premiums occur in 16% and 8% of simulation runs, respectively.

Fama and French found similar results for the size and value premiums, and concluded that this is simply the nature of risk—if you want to earn the expected (the mean of the distribution of potential outcomes) premiums, you must accept the fact that you will experience losses, no matter how long your horizon. Said another way, if you can’t stand the heat, get out of the kitchen.

They concluded: “The high volatility of stock returns is common knowledge, but many professional investors seem unaware of its implications. Negative equity premiums and negative premiums of value and small stock returns relative to Market are commonplace for three- to five-year periods, and they are far from rare for ten-year periods. Given this uncertainty, investors who will abandon equities or tilts toward value or small stocks in the face of three, five, or even ten years of disappointing returns may be wise to avoid these strategies in the first place.”

Myopic Behavior Kills Returns

In my more than 20 years of providing investment advice, I’ve concluded that most investors —both individual and institutional—believe that when it comes to evaluating investment returns, three years is a long time, five years is a very long time and 10 years is an eternity. However, financial economists know that the historical evidence demonstrates that 10 years can be nothing more than noise and thus should be treated as such.

Most investors lack the discipline required to do so. Thus, they end up being subject to recency, which results in buying after periods of strong performance (when valuations are high and expected returns are low) and selling after periods of weak performance (when valuations are low and expected returns are high). That’s not a prescription for investment success. It is also why Warren Buffett says his favorite investment horizon is forever.

Before concluding, it’s important you understand we cannot be certain of the investment risks (the odds of negative premiums) we have been discussing. That should make us less confident about earning premiums, meaning the odds of not earning the premiums may be higher than our estimates.

In other words, at best we can only estimate the odds of experiencing negative premiums—we cannot know them. That helps explain why the premiums have been so large. Investors don’t like uncertainty and demand large ex-ante premiums as compensation. They dislike even more owning assets that tend to do poorly during bad times, when their labor capital is put at risk. And that’s exactly when the three premiums tend to turn negative. Together, these two issues provide the explanation for the large size of the three risk premiums.

Two more important points we need to cover both relate to the diversification of risk. First, the odds of earning the premiums are based on portfolios that are highly diversified. For more concentrated portfolios (like those of the typical actively managed fund or the typical individual investor buying individual stocks), uncertainty about outcomes is higher. That is another reason why active investing is called the loser’s game.

Second, there is very low correlation of the three risk premiums. From 1964 through 2017, the annual correlation of the size and value premiums to the stock premium has been just 0.26 and -0.25, respectively, and the annual correlation of the size and value premiums is close to 0 (0.02). That makes them effective diversifiers of portfolio risk, a type of diversification not achieved by investors whose portfolios are limited to total market portfolios.

This is an issue that many find difficult to understand. Here is a brief, and hopefully helpful, explanation. It’s true that total market portfolios own small and value stocks, providing positive exposure to the premiums. However, they have no net exposure to the size and value premiums because their holdings of large and growth stocks provide negative exposure to the premiums—exactly offsetting the positive exposure provided by the small and value stocks.

Summary

The bottom line is that when developing your investment policy statement, you must be sure that your portfolio doesn’t take more risk than you have the ability, willingness and need to take. You must also be sure that you understand and accept the nature of the risks you are going to have to live with over time. The appropriate warning is that most battles are won in the preparation stage, not on the battlefield.

If you don’t understand the nature of the risks, when they do show up, you will be unable to keep your head while all about you are losing theirs, and it’s far more likely your stomach will take over. And I’ve yet to meet a stomach that makes good decisions. The result will likely be that your well-developed plan will end up in the trash heap of emotions. Forewarned is forearmed.

Next, we’ll take look at the two premiums related to bonds: term and default.

Note: Data presented in this blog is from Kenneth French’s website.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.