Swedroe: Don’t Blame Lack Of Dispersion

Active managers didn’t underperform indexes in 2014 because of the decline in the dispersion of returns.

In a recent article, Advisor Perspectives editor Robert Huebscher noted: “During the last 40 years, an average of 60% of equity funds underperformed the S&P 500. But, according to the SPIVA data, 86.4% of large-cap managers underperformed their benchmark in 2014. The percentages were not much better last year for mid-cap (66.2%) or small-cap (72.9%).”

The article goes on to cite work by Michael Mauboussin, managing director and head of global financial strategies at Credit Suisse, which makes the case that this poor performance was due to fewer opportunities for active management to add value because the dispersion of returns was lower than historically has been the case.

In other words, “Skill alone is not a predictor of success in active management; a second ingredient—opportunity—must be present. Last year’s failure was not because there were fewer active managers or because they lost their touch.”

While the dispersion of returns last year was indeed lower than the historical average, and you need dispersion to generate alpha, it’s simple to show that there was still plenty of opportunity for active managers to add value. It’s just that they didn’t do it. Even though dispersion may have been less than the historical average, there remained a massive amount of it that active managers could have exploited.

For example, Mauboussin’s data show that the average return of the top half of performers in the S&P 500 in 2014 was 42.9%. Compare that with the average return of the bottom half, which was just 21.3%. That’s a performance gap of 21.6 percentage points. Isn’t that a sufficient opportunity to generate alpha?

A Simple Solution

But it’s even much simpler than that to demonstrate the massive opportunity last year for active managers to add value. Consider the evidence in the table below, which shows the returns for the 10 best and the 10 worst performers in the S&P 500 Index:

| 10 Best S&P 500 Performers In 2014 | Return (%) | 10 Worst S&P 500 Performers In 2014 | Return (%) |

| Southwest Airlines | 124.6 | Transocean Ltd. | -62.9 |

| Electronic Arts | 104.9 | Noble Corp. | -55.8 |

| Edwards Lifesciences | 93.7 | Denbury Resources | -50.5 |

| Allergan Inc. | 91.4 | Ensco PLC | -47.6 |

| Avago Technologies | 90.2 | Avon | -45.5 |

| Mallinckrodt PLC | 89.5 | Genworth Financial | -45.3 |

| Delta Air Lines | 79.1 | Freeport McMoRan Copper & Gold B | -38.1 |

| Keurig Green Mountain | 75.3 | Range Resources | -36.6 |

| Royal Caribbean Cruises | 73.8 | Diamond Offshore Drilling | -35.5 |

| Kroger Co. | 62.4 | Mattel | -35.0 |

All an active manager would have had to do to generate a large amount of alpha was to overweight the top 10 performers and avoid the bottom 10. If they were really good, they should easily be able to avoid the worst 10 performers, shouldn’t they? Isn’t that what investors supposedly are paying them to do? Again, it’s that they just didn’t do it.

Every year, we hear the usual litany of excuses for why active management failed. In recent years, we’ve heard that this occurred because the correlations of returns had risen, reducing opportunities to generate alpha.

Unfortunately, it doesn’t matter what happens to correlations—active managers fail with persistence. Last year correlations fell sharply. Yet despite that, we saw almost 90% of large-cap managers underperform. Falling dispersions is just another excuse that doesn’t hold up to scrutiny.

Actually, there is a very simple explanation for why so large a percentage of large-cap managers underperformed. It’s called the law of style purity, sometimes referred to as Dunn’s law (named after the Southern California attorney who provided the insights).

The Law Of Style Purity (Dunn’s Law)

Dunn’s law states that when an asset class does well, index funds in that asset class will outperform active managers also in the asset class because index funds have the “purest” (greatest) exposure to large stocks. In 2014, the best-performing asset class was large-cap stocks.

The S&P 500 Index returned 13.7%, the MSCI U.S. Mid Cap 450 Index returned 13.4% and the MSCI U.S. Small Cap 1750 Index returned 6.1%. However, when an asset class does poorly, active managers in that asset class then have a greater chance to outperform their benchmark index.

The logic is simple: Index funds generally achieve the greatest exposure to the relevant risk factor responsible for the vast majority of the returns. In other words, when large-cap stocks are the leading asset class, as they were in 2014, index funds will dramatically outperform large-cap active managers.

The reason is that active managers tend to style drift (for example, large-cap funds often own mid- and small-cap stocks, and small-cap funds often own mid- and large-caps). Thus, active managers tend to lose some of their exposure to both the “winning” and “losing” asset classes. Consider the following evidence.

In every year from 1995 through 1998, the S&P 500 Index outperformed the MSCI midcap and small-cap indexes, generally by wide margins. And in each of those years, the S&P 500 Index outperformed about 80% or more of active managers (about 94% for the entire period, even before taxes).

Furthermore, in each of those years, the dispersion of returns was greater than it was in 2014. In 1998, it was far greater, about twice as high a level of dispersion as was the case in 2014. So much for that theory on lower dispersions.

Note that the reverse is also true. During periods like 1977 through 1982, when small-caps outperformed large-caps by about 16% per annum, only in a single year did index funds outperform even 40% of active large-cap managers.

The reason is simple: Active large-cap managers tend to own smaller-cap stocks than those in the S&P 500 Index (as Mauboussin noted). Thus, they held some of the “outperformers,” unlike in 2014, when they held some of the “underperformers.”

In periods when the S&P 500 outperforms, you hear claims like, “It wasn’t a stock picker’s year.” Stock picking has virtually nothing to do with it. It’s all about asset allocation. Active managers appear to lose (or win) because they style drift. In periods when small-caps outperform the S&P 500, active managers claim victory for their stock-picking skills.

Again, stock picking likely had little or nothing to do with it. If it did, then the same managers would keep repeating their outperformance, but we see very little evidence of that occurring.

Thus, we can conclude that one likely explanation for the miserable performance of large-cap managers in 2014 was that large-caps were the best-performing asset class. Mauboussin himself provides us with another explanation—which also helps explain why the midcap and small-cap managers fared so poorly, though not as poorly as the large-cap managers. The explanation lies in what is known as the “paradox of skill.”

The Paradox of Skill

Charles Ellis, one of the most respected minds in the investment industry, wrote in a recent issue of Financial Analysts Journal, “Over the past 50 years, increasing numbers of highly talented young investment professionals have entered the competition. … They have more-advanced training than their predecessors, better analytical tools, and faster access to more information.”

And according to Ellis, the “unsurprising result” is that “the increasing efficiency of modern stock markets makes it harder to match them and much harder to beat them, particularly after covering costs and fees.”

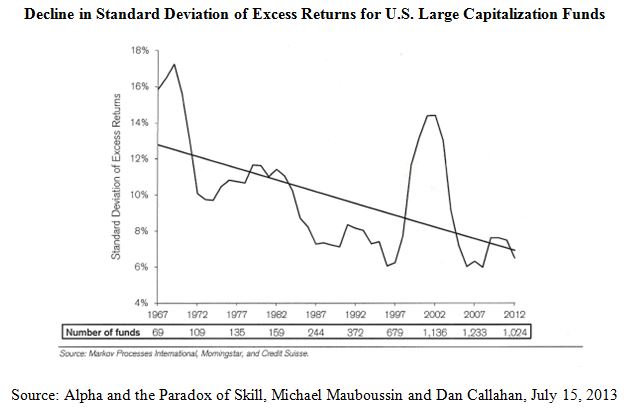

The working hypothesis, then, should be that, as the level of competition increases, we should see a decline in the dispersion of excess returns. The graph below shows the rolling five-year average standard deviation of excess returns in U.S. large-cap mutual funds over the last five decades. You should expect to see wide dispersions when there are large differences in the level of skill. Mauboussin’s finding of declining dispersion in excess returns fits perfectly with Ellis’ view that the competition is getting tougher.

In our book, “The Incredible Shrinking Alpha,” my co-author, Andrew Berkin, and I present four major themes we believe are making active management an ever-more challenging task—the odds of outperforming are persistently declining.

The first is that, through academic research, what once were sources of alpha have been converted into beta, or exposure to a systematic factor (such as size, value, momentum or profitability/quality). That reduces the amount of alpha available to be harvested.

Second, given that alpha is a zero-sum game before expenses and a negative sum game after expenses, to generate alpha there, must be victims that can be exploited. Unfortunately, the pool of likely victims has been persistently shrinking. Seventy years ago, 90% of stocks were held directly by individual investors. Today that figure is about 20%. The pool of sheep waiting to be sheared has shrunk dramatically, reducing the pool of available alpha.

Third, as Ellis noted, the competition is getting tougher. And fourth, the amount of capital chasing alpha has expanded greatly at a time when the sources of alpha are disappearing. Sixty years ago, there were less than 100 mutual funds. Today we have about 8,000 of them chasing alpha. Sixty years ago, there were very few hedge funds. Today we have about 10,000, representing more than $2.5 trillion in assets, all competing to generate alpha.

Those four factors are why active management is becoming more and more of a loser’s game. Yes, it’s still possible to win, but the odds of doing so are collapsing. Twenty years ago, about 20% of actively managed funds were generating statistically significant alpha. Today that figure is down to about 2%. And that’s before taxes.

As sure as the sun rises in the east, at the end of every year, you will hear excuses from active managers about their previous performance and claims that next year will be one for stock pickers. Unfortunately, next year never comes.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.