4 ETF Bond Managers Share Their Top Picks

In the ETF space, actively managed bond funds are popular, and their managers have very different ideas of where opportunities lie.

What to do about a fixed-income allocation remains a lingering question for many investors.

On one side, the 30-plus-year bond rally is said to be over, and the outlook for returns in bonds is on the decline. On the other hand, Treasury yields continue to drop even as the Federal Reserve remains committed to pushing rates higher (yields drop when bond prices rise). So far this year, 10-year Treasury yields have slipped 5.3%.

So what’s an investor to do? Baby boomers retiring en masse will continue to need income; foreign investors will continue to look to the relative appeal of U.S. yields over their own; and the need for diversification, for de-risking portfolios and for preservation of capital isn’t going anywhere. All these trends will keep the bond market underpinned, bond managers say.

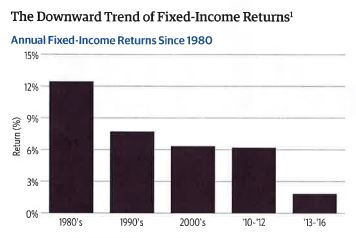

But consider broad fixed-income returns based on the Bloomberg Barclays Aggregate Bond Index (the Agg), in the past several years, as illustrated below. The trend is clearly downward:

Sources: Morningstar, Bloomberg

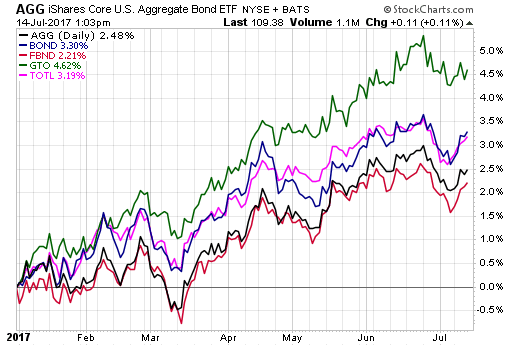

The Agg is one of the most widely used bond benchmarks in the fixed-income space, anchoring the largest bond ETF in the market today, the iShares Core U.S. Aggregate Bond ETF (AGG), with $48 billion in assets.

Active managers have been looking beyond the Agg benchmark in search of higher returns to meet investors’ income needs. Here’s how the price performance of the four most popular total bond ETFs stack up this year relative to iShares’ AGG. They include:

- SPDR DoubleLine Total Return Tactical ETF (TOTL), $3.4 billion in total assets; 0.55% expense ratio

- PIMCO Active Bond ETF (BOND), $2.04 billion in total assets; 0.56% expense ratio

- Fidelity Total Bond ETF (FBND), $278 million in total assets; 0.45% expense ratio

- Guggenheim Total Return Bond ETF (GTO), $37 million in total assets (the newest of the funds, having launched in 2016); 0.50% expense ratio

Source: StockCharts.com

For the most part, on a price return perspective, they are all outpacing AGG, with FBND the laggard of the group this year. (Last year, FBND was the top performer.)

The active managers behind these ETFs tell us their best ideas—where they are finding alpha these days, and what parts of the fixed-income market they are avoiding.

Guggenheim’s GTO Portfolio Manager Steve Brown

According to Guggenheim data, at $17.4 trillion, the Agg index benchmark represents less than half of the total U.S. fixed-income universe. That leaves out some $21.7 trillion in fixed-income securities that don’t meet the Agg’s requirements for inclusion, including a lot of agency-backed securities, nonagency residential mortgage-backed securities and bank loans.

GTO scours this much-broader universe in search of higher risk-adjusted returns. Where the Agg is currently concentrated in low-yielding Treasury and agency securities, GTO is looking elsewhere for alpha

The AGG ETF right now is 37% allocated to Treasuries and 28% to pass-through mortgage-backed securities (MBS). That compares to roughly 10% Treasuries and 11% MBS for GTO, which also has a 4% allocation to bank loans.

The portfolio is largely allocated based on the macro view that the Fed will raise rates at a more aggressive pace than currently priced by the market. Guggenheim expects another five rate hikes by year-end 2018, and for a flattening of the yield curve.

The firm says 10-year yields could remain below the 3% mark for years ahead, if history is any indication. GTO is also positioned for caution when it comes to risk. Only 1.3% of the portfolio is in high-yield bonds, but it’s also designed with a generally positive view of credit markets.

“GTO employs a barbell strategy targeting floating-rate securities, seeking to avoid intermediate-duration risk and overweighting the long end of the interest rate curve relative to its benchmark, Brown said. “We continue to believe the interest rate curve will flatten.”

“GTO looks to invest in credit securities, including structured credit, typically with spreads that are generally wider than that of similar-credit-quality corporate bonds or agency MBS,” he added. “In many cases, GTO invests in the senior part of capital structure within the structured credit markets.”

Fidelity’s FBND Portfolio Manager Ford O’Neil

FBND has taken a different route this year. Since last fall, the fund has practically doubled its exposure to U.S. Treasuries, looking to buy safety as it awaits value opportunities to pop up in other segments seen as overvalued, such as spread products that include high yield, leveraged loans and emerging market debt. Some investment-grade corporate bonds also fall in the camp of pricey.

“Anything that involved a risk aspect to the security, you’ve been well-compensated for the last 15 months,” O’Neil said. “But as securities we bought last year reached fair value targets relative to our expectation for the sectors, we’ve been reducing exposure to those areas.”

That reduction doesn’t mean the portfolio is completely rid of these securities; it’s just less allocated to risk-type assets. FBND still has about an 11% allocation to high yield. The fund also has a 15% weighting to financials and 20% to industrials—corporate sectors seen benefiting from the current macro environment.

“Last year, everything was very cheap, but today most spread products are fair-valued or just moderately cheap,” O’Neil said.

The key change has been the fund’s Treasury exposure in recent months.

“Instead, we’ve been adding Treasuries to the portfolio, not because they’re undervalued, but we’re building dry powder in the portfolio for the next time spread sectors underperform and create opportunities for us,” he explained. “We’re also keeping our TIPS position.”

PIMCO’s BOND Portfolio Manager David Braun

There are four key themes driving BOND’s allocations right now. The first is an overweight to agency mortgages due to positive technicals, high liquidity valuations and attractive yields relative to similar-duration Treasuries and corporates, according to Braun.

“We expect U.S. interest rates to be range-bound over the next few years as secular forces such as aging demographics, automation and supply gluts keep a lid on inflation and wages in the medium term, while a relatively dovish Fed will be gradual in monetary policy normalization,” Braun said. “Agency MBS also act as an attractive diversifier, and have historically done well during periods of market weakness.”

Secondly, BOND is “significantly underweight” investment-grade corporates because valuations are high relative to fundamentals, and PIMCO sees “balance sheets broadly moving toward higher leverage and late cycle behavior.” Still, the firm likes financials and asset rich sectors.

Third, BOND has a “bias to source our income from ‘bend but not break’ securitized credit,” Braun said. That means “buying cash flows that are remote from risk of principal loss even in scenarios of significant stress in the economy.” An example of this is in senior tranches of structured credit such as nonagency residential MBS, commercial MBS and select consumer ABS.

Finally, “we have a favorable view of select emerging markets and have modest exposure to Mexican and Brazilian government bonds, which are trading at attractive yields of 7-9% and benefit from a deflationary tail wind and improving domestic fundamentals,” he added.

BOND has 28% of its market value tied to Treasuries and 43% tied to mortgage securities—a different split from the Agg index benchmark. The fund also has a 6% allocation to high-yield bonds and 3.3% to emerging market bonds—riskier types of assets. The Agg is a U.S. investment-grade-only benchmark.

SPDR DoubleLine’s TOTL Portfolio Manager Jeffrey Gundlach

Gundlach has long been calling for Treasury yields to drop—at least initially—instead of rise this year. DoubleLine declined to comment for this story, but according to a series of webcasts he’s done in recent months, Gundlach expected a rally in 10-year bonds due in part to a record short position in Treasuries. That rally would push yields lower.

That doesn’t mean Gundlach is investing for an enduring bond rally. On the contrary, he’s said he expects 10-year yields to near 3% before year-end, and for the Fed to continue to raise rates in the face of a positive macroeconomy.

TOTL’s allocation to Treasuries today is less than half that in the Agg benchmark—only 16.7%.MBS, on the other hand, represent a whopping 52% of TOTL’s mix—compared to 28% for the Agg index.

One of the persisting themes in TOTL is Gundlach’s focus on MBS, as well as their U.S.-centric approach to a total bond portfolio. He continues to argue that “the risk/reward on a yield versus duration perspective is so very bad" for developed-market bonds other than the U.S.

He also recently said that yield-to-duration ratio in the Agg index, as well as for Treasuries and investment-grade corporate bonds, remains poor.

Contact Cinthia Murphy at [email protected]