Currency-Hedged ETFs: A Double-Edged Sword

As the U.S. dollar reaches a peak, has the currency hedged fad already run its course?

Currency hedged ETFs have gained favour in recent years as the euro and yen fell against the dollar and sterling while the Swiss franc skyrocketed, driven largely by central bank policy. However, with the dollar's rise appearing to have peaked and the effect of the European Central Bank's quantitative easing now priced in, has the opportunity for currency hedged ETFs already run its course?

In recent years, currency hedged ETFs have clocked up significant gains over and above their un-hedged counterparts. According to Morningstar, for example, in 2013, the MSCI Japan gained 55 percent in yen terms, but the 18 percent fall in the yen versus sterling resulted in a much more meagre return for the iShares MSCI Japan ETF in pound sterling, which advanced by less than half that amount at 24 percent. By contrast, the iShares MSCI Japan GBP Hedged ETF returned 52 percent.

More recently, the UBS MSCI EMU 100% hedged to GBP UCITS ETF gained 11.08 percent over one year by the end of May, far outstripping its un-hedged counterpart, the MSCI EMU UCITS ETF, which fell 0.81 percent.

Currency Awareness On The Rise

As investors' become increasingly globally diversified in their allocations across asset classes, the perception of currency risk has increased markedly, which has fuelled the popularity of currency-hedged ETFs.When a proportion of a portfolio's assets are invested in foreign securities, the portfolio indirectly acquires an implicit underlying exposure to currency movements. In other words, there is an inherent currency bet in investing in foreign assets, which, if ignored, can distort the risk-return profile of the portfolio.

A currency hedged ETF allows an investor to effectively separate the risks associated with currency fluctuations from those of the underlying assets, creating a more pure exposure.

According to Andrew Walsh, head of UBS ETF sales UK: "People are much more aware of currency risk and it is part of how they are judged. Previously they just had to bear it, but now they can separate the equity from the implicit currency bet."

From a risk management perspective they also have an important role to play. "By no means are we suggesting that every foreign investment should be currency hedged," said Townsend Lansing, head of short/leveraged & FX platforms at ETF Securities. "We do however believe that currency hedging can be a useful tool to ensure that a portfolio's broader currency exposures meet its risk limits."

Closing The Barn Door After The Horse Has Bolted?

However, with the euro appearing to have bottomed out against both sterling and the dollar after its dramatic fall in January when the ECB announced its QE program, and another slide as tensions rose in recent months around a potential Grexit, has the opportunity for currency hedging already passed?

There is also a school of thought that, given currencies tendency to revert to the mean over the long-term, and that a broad and diversified portfolio would also likely be more balanced from a currency perspective, the currency effects at the portfolio level effectively cancel each other out, leaving little point in hedging.

"Regardless of whether this argument is true or false, it doesn't undermine the value of currency hedged ETFs," argued Mehdi Alighanbari, vice president, equity applied research, at MSCI. "Equity investors are subject to short-term fluctuations of currencies. The recent large moves in the Swiss franc and euro, and their effect on investors, show that even long-term investors are affected by short-term events."

Take Notice Of The Short Term

In effect, investors should care about the effect of currency on their investments in the short term the same way they would care about the volatility of returns in their equity portfolio even if they are long-term investors.

"If you think currencies are going to move versus each other in the future, which is fairly uncontroversial, and hold foreign currency equities in your portfolio, and don't want them to be affected by these currency moves, then the case for using FX-hedged indexes is still valid," said Alighanbari.

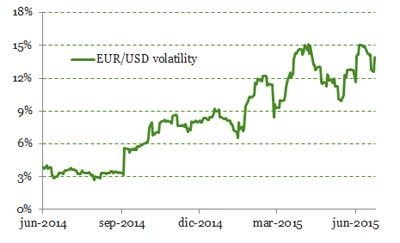

Currency volatility has picked up markedly in recent years on the back of central banks' more active monetary policy. This is forcing international portfolio managers, who may previously have ignored the impact of currency volatility, to recognise its more considerable impact on the risk-adjusted returns of foreign assets.

EUR/USD volatility, for example, has more than trebled from around 4 percent in June 2014 to nearer 14 percent in June 2015, but peaked at 15 percent twice in the last three months.

In view of that raised volatility, ETF Securities' Lansing argued: "For investors that possess a macro strategy that incorporates international investments, now is the most important time to consider currency hedged ETPs."

Look At Correlations Between Assets And Currency

It is also important to consider how closely assets are correlated to their home currency as the link between the two should play a key role in determining whether or not a foreign investor wants or needs a more pure exposure to the asset in question.

For example, for a UK investor tracking a global market cap index such as the MSCI World, less than 8 percent of the underlying companies in the index would derive their revenues in the UK. For a U.S. investor, that increases to over 57 percent, but for a French investor it falls to less than 4 percent.

Tim Huver, ETF product manager at Vanguard, said the results of currency hedging were "highly reliant on the correlation between the underlying asset and the currency".

Even within a more concentrated index, such as the MSCI Europe, investors need to consider how closely companies within the index are likely to track the fortunes of the single currency. The top 10 holdings of the MSCI Europe, which represent over 18 percent of its total weight, include massive international organisations such as Nestle, Novartis, HSBC, BP and Royal Dutch Shell that generate revenue from operations across the globe, making them less sensitive to moves in the euro.

UBS' Walsh argued that where a disconnect between an underlying equity market and the home currency existed, that was a "perfect case for hedging."

Currency Hedging Means You Could Lose Out

However, the shortcomings of currency hedged ETFs also need to be recognised – not least due to their potential to dampen upside return potential where currencies rise. This means currency exposures will need to be carefully managed over time.

As Morningstar's passive fund analyst Kenneth Lamont said: "The main [issue with currency hedged ETFs] is that investors may miss out on gains should the foreign currency appreciate in value against the home currency."

UBS's Walsh referred to this as a "double edged sword".

"It goes without saying," he said, "that while you can protect yourself using currency hedged ETFs, you can also forgo the upside if the currency appreciates while you're in the bet."

For example, a German investor buying U.S. equities a year ago would have been "crazy to hedge", Walsh said, as they would have been able to ride positive gains on both the underlying equities and the currency as the euro fell 17 percent against the dollar from 1.36 on 25 June 2014 to 1.12 a year later.

The potential for limiting potential gains means currency hedged ETFs are more of a short-term tactical investment tool. Walsh said this was something investors would "certainty want to monitor over time", but didn't feel that undermined the important role these ETFs can play for investors.

"You don't always need a Philips head screwdriver," he said, "but you'd want to know you have one in your toolbox."