Small Junk Bond ETF Sees Mighty Gains

This relatively small high-yield fund is delivering outsized returns this year relative to the segment’s giants.

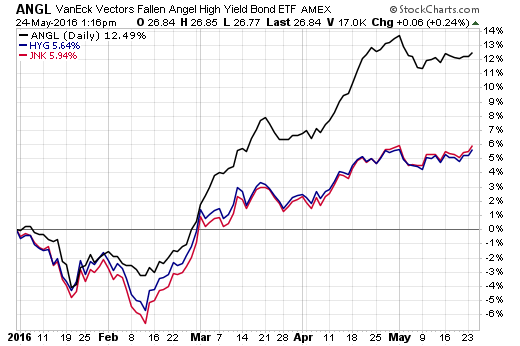

The VanEck Vectors Fallen Angel High Yield Bond ETF (ANGL | C-51), which has fathered $160 million in total assets since it came to market four years ago, is up more than 12% year-to-date.

By comparison, the behemoths in the space—the $14 billon iShares iBoxx $ High Yield Corporate Bond ETF (HYG | B-68) and the $12 billion SPDR Barclays High Yield Bond ETF (JNK | C-68)—have delivered less than half those returns in the same period:

Chart courtesy of StockCharts.com

There are several reasons these funds are doing what they’re doing. ANGL hunts for "value" in the high-yield space by targeting "fallen angels"—bonds rated investment grade at issuance that have since been downgraded. The bulk of its holdings—75%—are bonds rated BB.

HYG has about 49% of its portfolio tied to bonds of that same credit rating, while JNK has 42% of its portfolio tied to debt rated BB. In the first quarter, all high-yield credit ratings delivered gains, but bonds rated BB bonds led the way, rising 3.5%, according to Guggenheim data. That compares with 2.8% gains for debt rated B and 3.0% for bonds rated CCC.

Energy Rebound Fueling Gains

Perhaps more importantly, it was ANGL’s hefty allocation to the energy sector that really allowed the fund to stand out. ANGL currently has energy-sector debt representing more than 25% of its portfolio. That allocation grew from 13% at the end of 2015, significantly higher than HYG’s 11% energy weighting. JNK’s allocation to energy is negligible, which doesn’t even list energy as one of its key sector exposures. In JNK, industrials represents some 88% of the fund.

VanEck’s fixed-income portfolio manager Fran Rodilosso said that ANGL’s success hinges on the fund’s “contrarian investment approach,” meaning the portfolio tends to increase weights in sectors that are still under ratings pressure.

"One of the reasons fallen angel high-yield bonds have performed well in the past is that the bonds have tended to come into [ANGL's underlying index] already pricing in a high degree of risk," he recently said.

Value Play

In other words, ANGL is designed in a way as a value opportunity, acquiring bonds that are oversold on their path of being downgraded. The plunge in oil prices last year wreaked havoc in the energy sector, and pushed many investment-grade corporate debt into downgrade territory.

Those bonds, which were cheaply valued once they became high yield, put ANGL in a great spot to benefit from the gains in the oil market—and the energy segment—this year.

In fact, energy bonds have delivered their best performance ever in the first quarter, as oil prices rose and the dollar weakened, according to Thomas Hauser, managing director of Guggenheim’s investment team led by Scott Minerd. A relatively dovish Federal Reserve has also helped the high-yield segment in general, Hauser said in the firm’s more recent quarterly outlook.

Reversal Of Sentiment

“Initially headed for its worst quarter on record, the high-yield corporate bond market ended up posting its best first quarter since 2012 after a reversal in sentiment drove a risk-asset rally,” Hauser said.

“Despite the expectation of higher volatility [in the months ahead], we expect to use market weakness to find attractive entry points in energy bonds,” he said. “A stabilizing oil market in the second half of 2016 should pave the way for energy bonds to perform well over the course of the next 12-24 months.”

Since the beginning of the year, ANGL has attracted nearly $94 million in net creations—that’s three times the inflows the fund saw in all of 2015.

HYG has now lost $738 million in assets year-to-date, while JNK has gathered $2.1 billion in net assets in the same period.

“I believe that the market had an incomplete understanding of the differences between ANGL, HYG and JNK, and the underlying exposures across sectors and credit quality, ” said Kim Nordmo, managing partner at Artience Capital Management.

“Most of the energy exposure in ANGL is midstream B-range credits, which was relatively insulated versus lower-credit-quality, original junk, which proved to be more vulnerable. That illustrates the value proposition of ANGL,” she noted.

“Remember, ANGL is composed of bonds that are purchased at discounts that have higher-credit-quality orientation to begin with, and they simply default less," added Nordmo. "Maybe, now that the ANGL ETF has had some time to reveal its nuances, investors will catch up.”

Contact Cinthia Murphy at [email protected].