Private Credit ETFs 101: Collateralized Loan Obligations

Confused about CLOs? Wondering how access works via the ETF wrapper or the differences between public market and private credit CLO ETFs? Don't miss this explainer that steps through the genesis of CLOs, the private credit CLO ETF structure, and the pros and cons of exposure for ETF investors.

We’re continuing our exploration of private credit assets used in ETFs. In the previous piece we discussed Business Development Companies (BDCs). This article is going to focus on collateralized loan obligations (CLOs).

So what is a CLO?

A CLO is a securitization or packaging of loans, usually senior secured loans, to companies with varying levels of credit rating. These companies tend to be rated below investment-grade, but the securities purchased by an ETF can be rated anywhere from AAA down to junk. So how does the process work?

For a standard CLO, an initial pool of loans is sourced and packaged into a special purpose vehicle (SPV) by the CLO manager (not the ETF fund manager). The loan pool must be diverse to satisfy regulatory requirements. Traditionally these loans are primarily sourced from the broadly syndicated loan (BSL or leveraged bank loan) market but we’re focused on private credit CLOs. Private credit CLOs differ from their public market brethren and originate their own loans to unrated middle market borrowers.

If this sounds similar to my article on BDCs, that’s because it is! We’re effectively talking about the same type of borrowers but the difference is in how the lending is financed and what exposure to the top, middle, and bottom of the capital stack an investor can get.

History of CLOs

The first real CLOs emerged in the 1990’s. Prior to that, most securitizations had been done on bank balance sheets made up of either loans to corporate borrowers or mortgage-backed securities. These prototype CLOs were created because capital requirements for leveraged loans were imposed on banks that made it really expensive to hold them on the bank’s balance sheet. A natural way to offload this risk was to securitize the loans, slice the assets into tranches based on credit risk and sell those tranches to other investors. The initial versions of CLOs were simpler than their modern contemporaries with little to no standardization for disclosures, portfolio compositions, and transparency. The senior tranches (AAA-AA rated) were utilized heavily by insurance companies, pensions, and other banks seeking capital relief. The returns offered by these tranches were superior to securities rated similarly. Issuance of these first versions of CLOs grew through the 90’s and hit $100B a year in 2006.

In 2008 when the Great Financial Crisis hit, senior tranches of CLOs1 performed admirably with no recorded defaults. It is VERY important to note that a lot of the less senior tranches were wiped out and investors lost everything invested in them. To be clear though, CLOs were not responsible for the crisis. Their cousins, collateralized debt obligations (CDOs) among other things were responsible for that and dragged them (and everything else) along for the ride.

The CLO market completely shut down post-GFC as risk appetite evaporated and the leveraged loan market was effectively frozen. There were regulatory changes to close gaps in lending standards. The Dodd-Frank Act passed in 2010 had extensive provisions for capital and risk retention requirements for banks including CLO managers. Once these regulations were promulgated and released, banks and lenders went to work finding paths back towards leveraged lending. The Fed also kept rates at close to zero and created a credit market-wide hunt for yield. Enter private credit CLOs.

Private credit CLOs are distinct from standard CLOs because of their collateral. Lending to middle-market unrated companies is inherently riskier so higher credit enhancement, stronger covenants and a premium for illiquidity are hallmarks of these deals. The biggest difference, that I alluded to earlier, is that they originate most of their own loans via direct lending platforms. Usually these platforms are internal so the manager is the pivot point for both lending and servicing of these loans.

As investors searched for yield during the Zero Interest Rate Policy (ZIRP) era, banks were unable to lend into markets they had previously dominated like the leveraged loan and middle markets due to these new capital constraints. Non-bank lenders stepped in to lend to these companies. This “private” credit market needed to quickly expand and the CLO structure, which now had much more standardized reporting, stricter collateral requirements, and tighter coverage tests, was a solid fit.

The private side of the CLO market scaled as the rest of the industry did, now taking up between 20-25% of issuance with a notional value of ~$40 billion being lent annually as of 20252.

Product Structure

Ok, now that we know our history we can explore how these private credit CLOs actually work.

Here’s an overview of a theoretical $500mm private credit CLO deal.

| Tranche | Rating | % of Deal | Dollar Amount | Spread (SOFR+) |

|---|---|---|---|---|

| Senior | AAA | 55-60% | $275-300M | 160-180 bps |

| Senior Mezz | AA | 8-10% | $40-50M | 200-225 bps |

| Mezz | A | 5-7% | $25-35M | 250-275 bps |

| Junior Mezz | BBB | 4-6% | $20-30M | 350-400 bps |

| Junior | BB | 3-5% | $15-25M | 550-650 bps |

| Equity | NR | 20-25% | $100-125M | Residual |

The process starts with the CLO manager originating the loans that will go into this pool. Managers will usually have a deal pipeline in place well before any actual origination. A huge part of the business is relationship building and management to be able to source these deals. The manager will underwrite, negotiate terms, and fund the loans. They also usually retain the entire equity portion (20-25% of the entire deal structure). This will be important later.

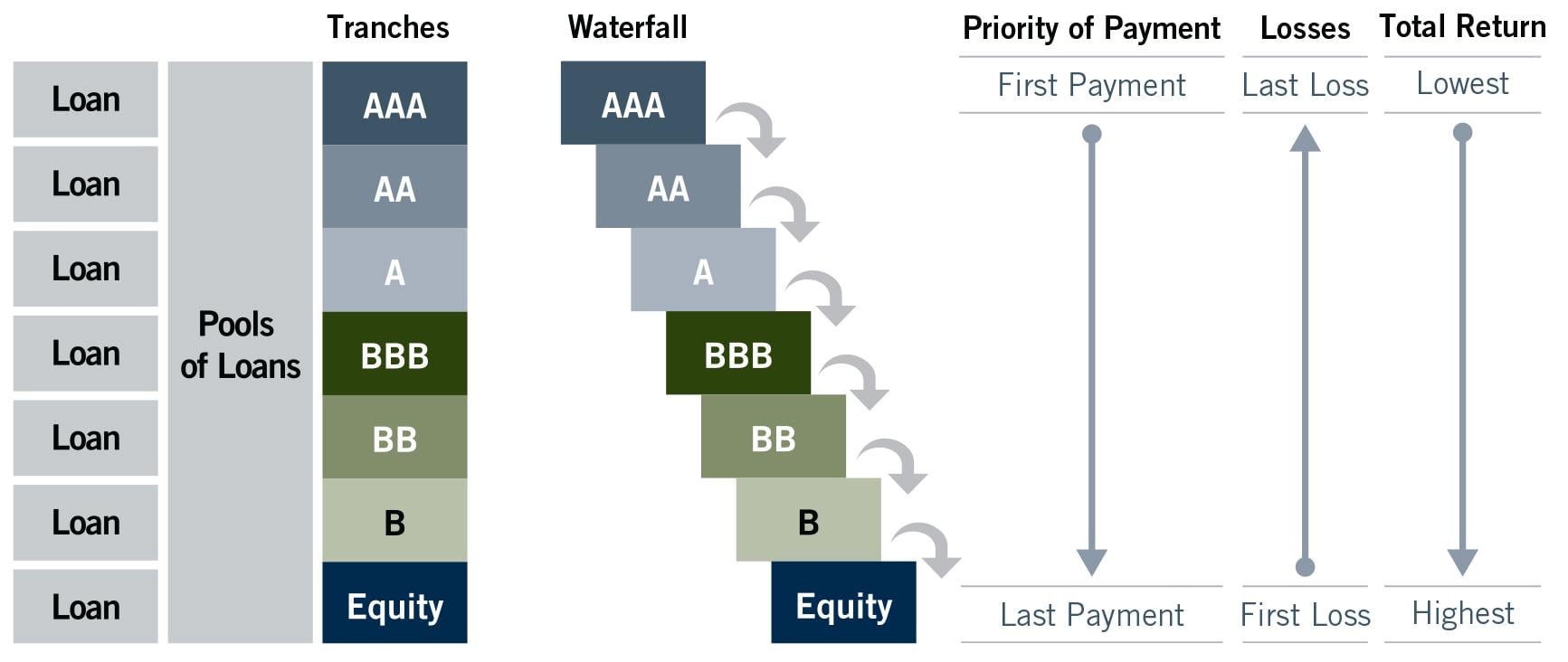

The Waterfall and Cashflows

Figure 1: https://www.virtus.com/our-products/individual-investors/virtus-seix-aaa-private-credit-clo-etf

The CLO is structured so that cash flows from top tranches to bottom equity portion. AAA tranches are paid first, AA second, and so on down to the equity portion which absorbs any remaining income.

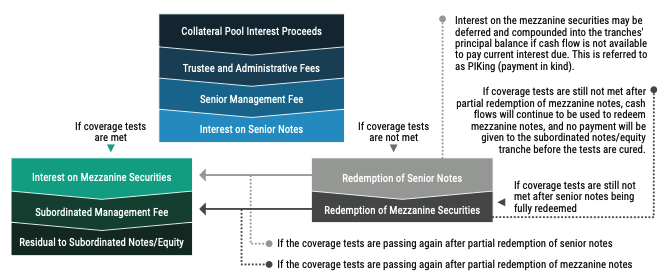

Along the way, there are coverage tests done on the overall portfolio. These evaluate the amount of collateral and interest payments made within the structure. Usually, the income that is generated by the underlying pool of loans must eclipse the interest due on the outstanding debt in the CLO and the principal amount of the underlying pool of loans has to be greater than the principal on the CLO. These tests allow the CLO to be somewhat self-healing. If they fail, there are a number of remediations that can happen from junior tranche cashflow being used to pay down senior principal balance to partial/full redemption of junior notes rolling up the capital stack as severity increases.

Look at the graphic below that can help you visualize what the changes are.

Figure 2: https://assets.pinebridge.com/m/21d36a807f12b5fb/original/CLO-Primer-Nov-2024.pdf

Credit enhancement

Credit enhancement is how much of the existing capital needs to be eaten up by credit losses in subordinated tranches and equity portion before the tranche above it is impacted. The equity portion in private credit CLOs is much larger than the public varieties. As I mentioned earlier, the manager usually retains the entire thing.

In our example, this means the top AAA tranche has between 40-45% credit protection, of which 20-25% is held by the fund manager. This gives the fund manager major incentive to source deals that have both solid borrowers but have a risky enough profile, either due to business structure or market structure, that they’ll offer worthwhile returns.

It also means that investors in the senior tranche have a substantial level of loss protection before any potential cashflow impact.

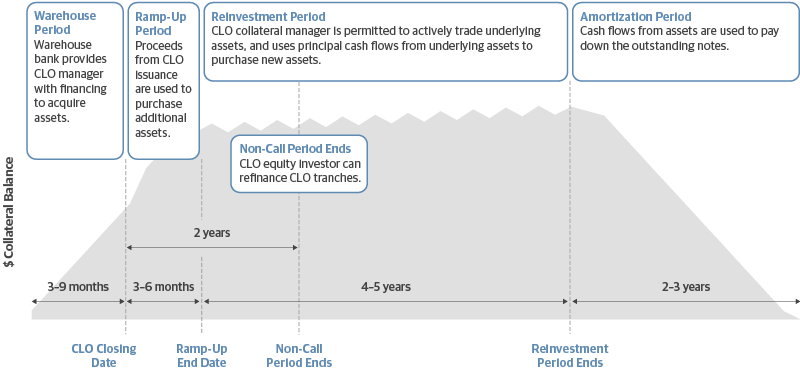

Reinvestment Period

What’s a reinvestment period? It’s the time after a CLO closes its financing round when it is both originating assets and able to adapt to changing credit conditions by refinancing earlier loans. Once the reinvestment period ends, the portfolio is static through the rest of the lifecycle. This period is usually between 3-4 years for private credit CLOs and 5 years for BSL CLOs.

A good ETF manager will be paying close attention to the number of CLOs they have that are “active” in their reinvestment period versus closed. This period is particularly important for private credit CLOs because they can’t simply replace a poor performing loan on the secondary market; they have to originate a replacement or be stuck with this non-performing loan throughout the rest of the lifecycle.

The Good, The Bad, and the Illiquid

Let’s go through the positive and negatives of these securitized ETF offerings.

The obvious advantage compared to regular CLO ETFs is a higher yield. This is due to the illiquid and unrated nature of the underlying collateral. The companies being lent to are risky! This risk means that similar tranches of private credit CLO ETFs can yield up to 40 bps more than their public market CLO ETF brethren.3

It’s also important to know that private credit CLO ETFs operate across all tranches of these securitizations except the equity portion. That said, they tend to concentrate in the senior and investment-grade tranches. Why don’t they go down into equity portion? As I noted above, those are retained by the CLO manager. It’s important to keep in mind that these junior and equity tranches are far less liquid than even the senior portions and that’s largely by design. The junior tranches are usually placed with the manager’s affiliated funds, insurance companies that want to buy and hold, and very sophisticated institutional investors. These tranches offer a higher yield profile but at a major cost of liquidity.

That stands somewhat in contrast to the much more liquid mezzanine and equity portions of a standard CLO, which can be accessed also be accessed within the ETF structure. The majority of these private credit CLO deals are sold based on relationships that are built over years and require heavy trust between the investor and the manager. (CITE)

Another risk factor is credit cycle sensitivity. Yes, senior CLO tranches did not default during the GFC. However, these are significantly riskier and less diversified loan packages than standard CLOs. The actual performance in a recession or major credit event cycle is untested and there’s no guarantee that they’ll avoid a wave of defaults if the markets turn.

Diversity within a private credit CLO, particularly getting exposure to different managers, can also provide a risk buffer. Products that stick with well-established managers that have long track records, large infrastructure, and workout capacity (in the event of a default) are implied to have a better likelihood of investors being made whole and tend to be priced with tighter spreads.Some proven managers could include Golub Capital, Ares Capital Management, and others. This is NOT an endorsement for those firms.

Similar to BDCs, these products are very sensitive to interest rates. All of the underlying loans are floating-rate so if the current rate cutting cycle from the Fed continues it will impact the yield of the portfolio moving forward. A reversal would cause the opposite effect and benefit investors.

There is also a major correlation risk with private equity. Most of the borrowers in the middle-market are PE-backed so any potential slowdown in sponsor activity, exits or anything that could affect borrower cashflows is likely to impact loan performance across the assets class. This also plays into refinancing and reset risks. The loans in these CLOs are fixed-term so inevitably the CLO manager has to decide whether they’re going to reset (aka originate more loans) or wind down the fund. In the case that the CLO resets, the current credit market conditions could drastically change the profile of the portfolio and potentially lead to much lower asset performance. This doesn’t only affect the underlying loan but also secondary market pricing for the ETF itself.

New Kids on the Block

Products in this segment are new. The first private credit CLO ETFs launched in December of 2024. They have a limited track record, but from what we’ve seen they have functioned as advertised. Investor demand has not picked up yet but that can be at least partially attributed to investment managers wanting an established track record of at least a few years before deploying institutional levels of capital.

As I said in my original Private Credit Crash course article, I think these are a great way to allocate to middle market private credit. You can control your level of exposure easily and there is enough diversity and liquidity to assuage most fears. As always, these are risky products so please research the underlying portfolios before investing and always stay up to date with potential issues in credit markets as these floating-rate products are still quite exposed to interest rate risk, default risk, and liquidity risk.

In the next article I’ll discuss the burgeoning Core Plus segment. There’s plenty to go over and I’ll show how some very vanilla funds have been dipping their toes in private credit.

Sources:

1 https://structuredfinance.org/wp-content/uploads/2020/02/SFA-CLO-White-Paper.pdf

2 https://flow.db.com/Topics/trust-and-securities-services/update-on-clos-outlook-for-2026

3 https://www.lsta.org/content/the-rise-of-private-credit-clos/

Discover the news, data, and voices shaping the ETF community. Follow along here.