SpaceX is a Value Stock? Seriously?

Welcome to the whacky world of factor indexes, where everything breaks at the edges.

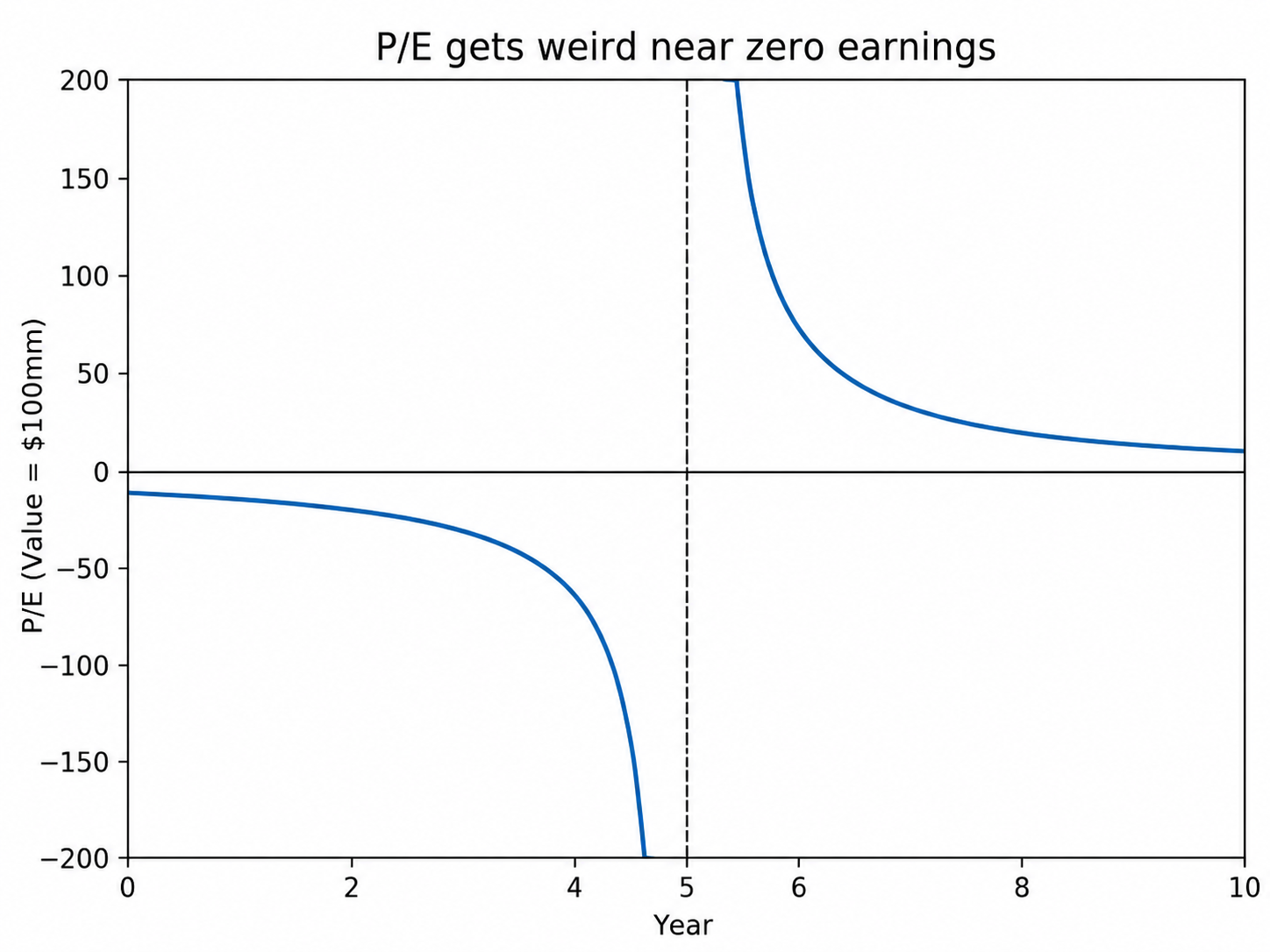

A million years ago, I asked a group of young analysts what they thought about Price-to-Earnings. It's one of the first things investors learn about, so there was immediate engagement. Everyone loved it. So then I asked the next question: "Graph the P/E of a 100mm company that goes from losing 10 million a year to making 10 million a year, over a 10 year window."

And that's when the crying started.

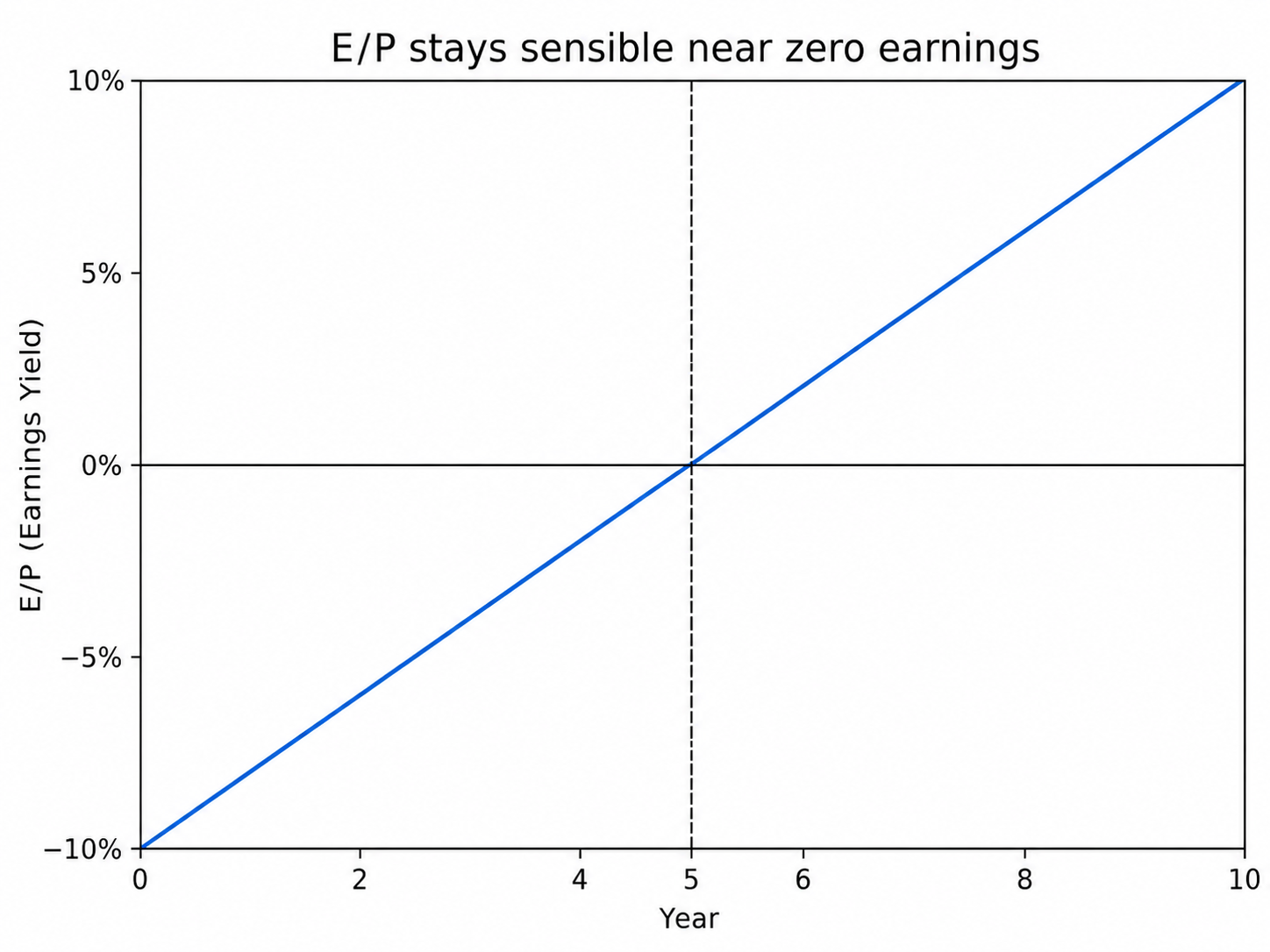

This is why P/E is in general a terrible datapoint from which to make a decision - it's discontinuous. Many smart people simply invert the ratio, which becomes earnings yield which, while containing the same information, at least looks better on a chart.

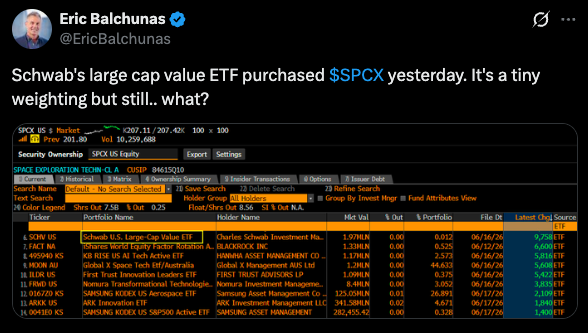

But regardless – pretty much every measurement of a company's value has to be some measurement of price first and foremost. So how then does a brand new IPO like SpaceX fit into growth/value methodologies? The answer is a frustrating "it depends" but let's walk through the specific ETF that sparked this conversation, via Eric Balchunas at Bloomberg about the Schwab U.S. Large-Cap Value ETF (SCHV):

Assuming for a moment that this isn't an error, I couldn't help myself: I had to try and reconstruct how SpaceX could even be considered value.

Index Methodology Matters

From my reading today, most major US style index providers base their earnings analysis on E/P. Thus, a strong negative number means anti-value. Huge E/P means value king. You'd assume the Dow Jones index in question (based on the methodology documents available to the public) would ignore the weirdness factor (meaning a P/E of -100 is more value than a P/E of -1) but the actual methodology is a little more complex.

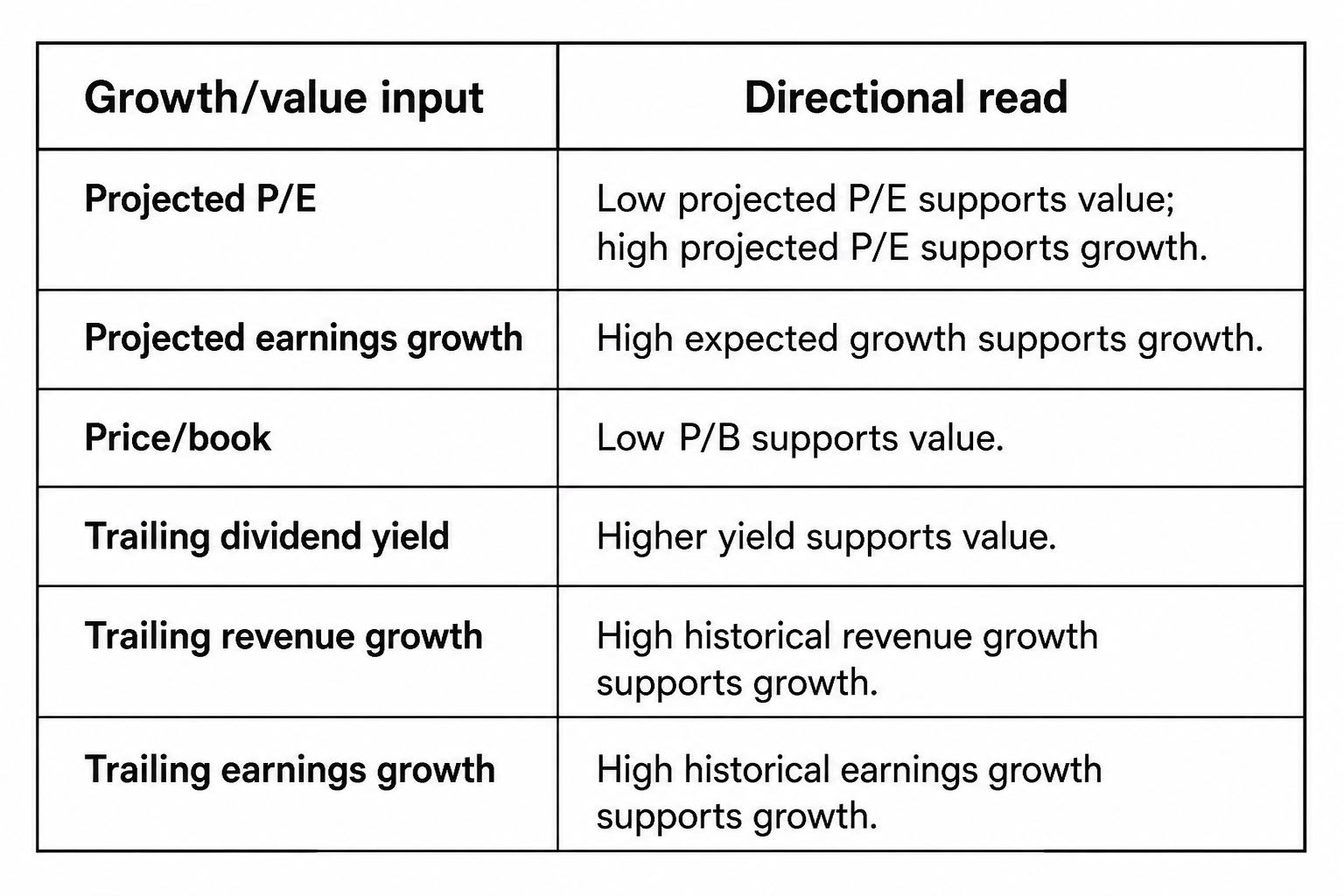

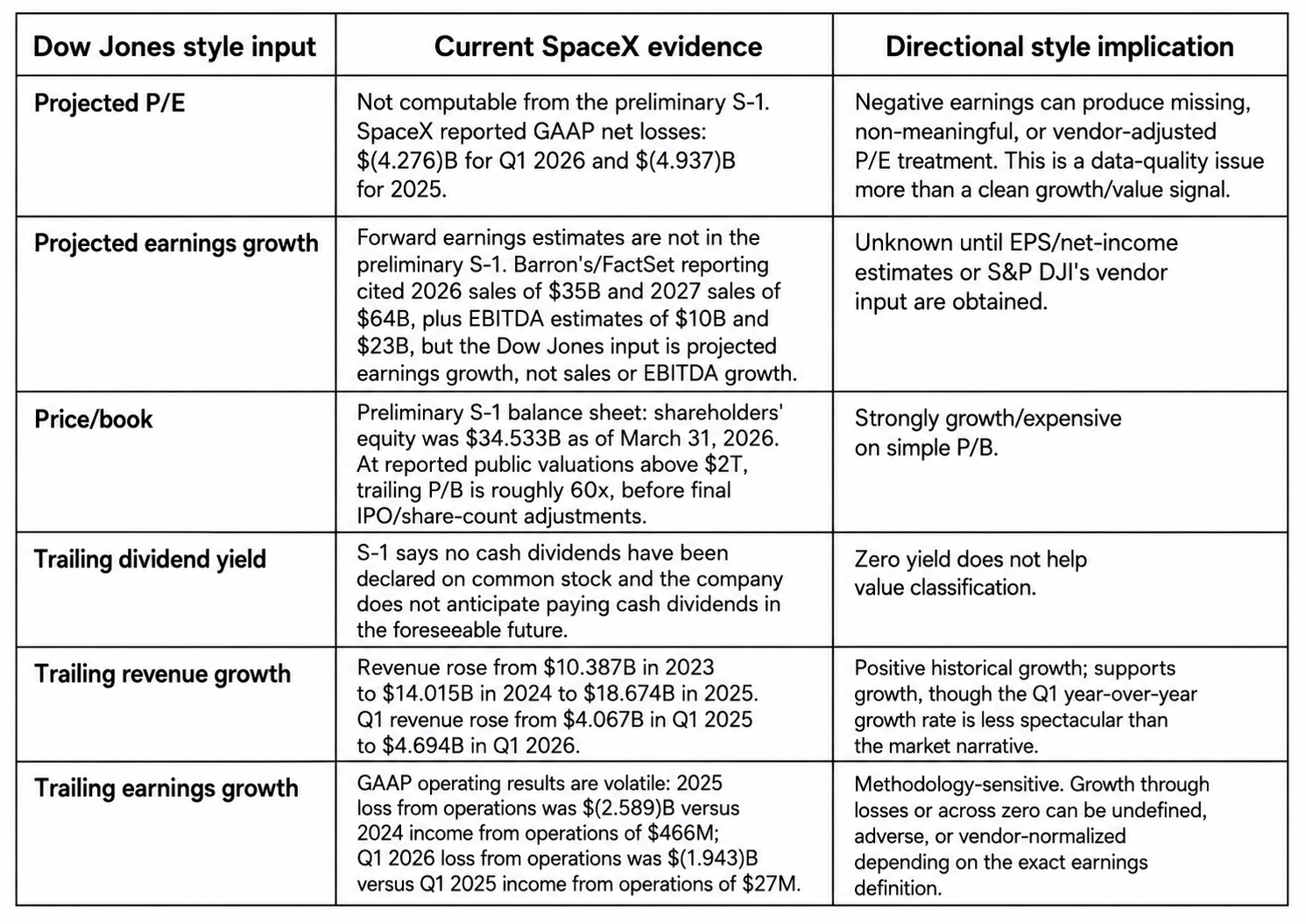

DJ looks at 6 factors to decide whether a single stock is Neutral, Strong/Weak growth, or Strong/Weak Value. We have, right now, no way of knowing what bucket the methodology stuck SpaceX in, but we CAN go through that exercise ourselves. Here are the 6 factors they use as inputs:

You can see the problem already: minimal data to fill these buckets, but I wanted to try and recreate the case here: just HOW does SpaceX go through this set of factors and land as value? Especially when you consider that very first chart – the one that makes people's head explode? That's exactly what SpaceX did over the last few years, sliding across the head-detonation negative earnings line.

Well, after bashing my head at it for a few hours (with LLM help of course), here's my best guess, mostly using the S-1:

So, in almost all cases, this really doesn't help make the case for "value." And that's the whole point. Nobody's picking SpaceX for value. It's just getting locked out of growth.

You can see that in the table: the three strongest growth hooks collapse under the earnings math. Projected P/E? We don't know what they plugged in, but even the most fantastical projections don't get you to instant break-even — so negative earnings blow up the calculation. Projected earnings growth? Same problem, same crater. P/B and trailing revenue growth are both

real growth signals, but they're almost certainly winsorized — clipped at the 5%/95% boundaries — so neither gets to be a strong growth hook. Add it up and SpaceX has no usable strong signal in any direction.

This very lack of signal is locked in with the rest of the methodology: it uses Z-scores to measure how far each stock sits from neutral, then sorts into clusters. A stock with no strong inputs has nowhere to go. It can't reach growth, it can't reach strong value, so it drifts to neutral or weak value almost by default. The problem, in other words, isn't that SpaceX looks cheap. It's that it looks like a mess.

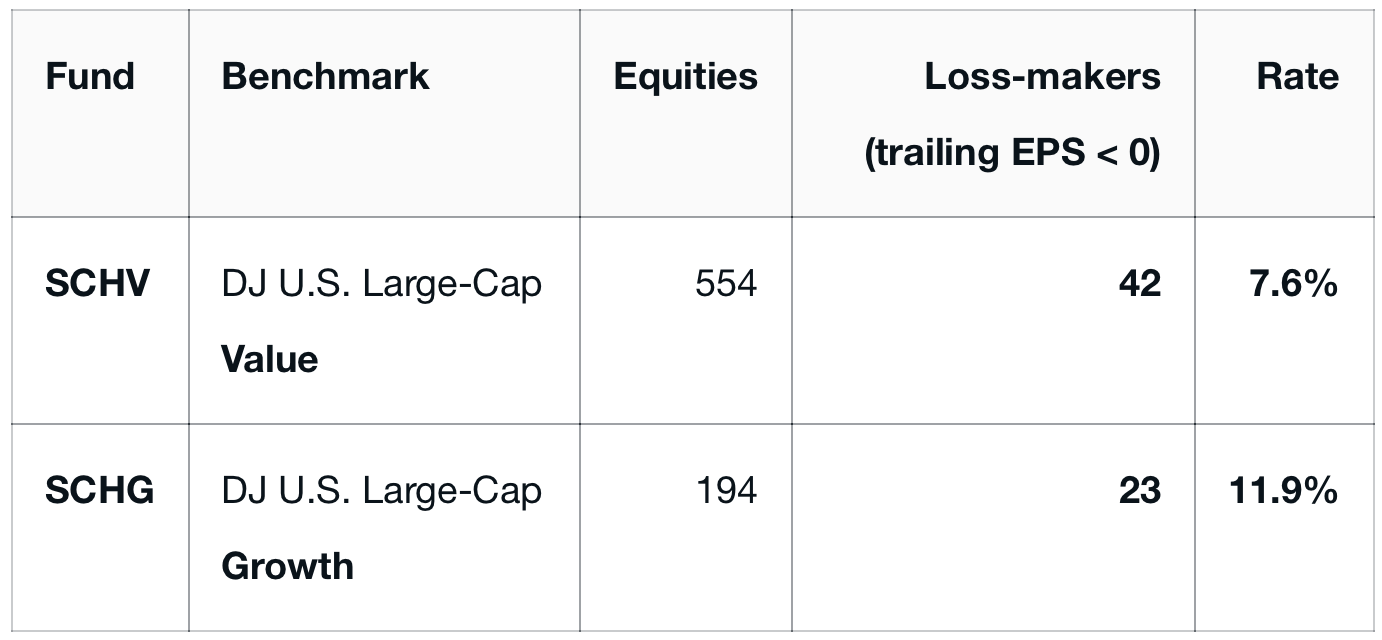

You might think the negative P/E gets clipped to the cheap extreme and SpaceX reads "cheap cheap cheap." Maybe, at the margin, but if that were the real determinant of getting into value then the value index would be stuffed with money-losers. It isn't. The growth index actually has the higher share of them — 11.9% of its names lose money versus 7.6% of the value side. So this isn't fake-cheapness pulling SpaceX in, it's incomprehensibility keeping it out of growth.

It has company. 42 of the 554 stocks in the value index are losing money: CoreWeave, Rivian, Joby Aviation, AST SpaceMobile: capital-hungry, pre-profit, frontier-tech money pits, every one of them filed under value. And the biggest tell? AST SpaceMobile, a money-losing satellite company, is in the value index, while Rocket Lab, also a money-losing space company, is in growth. Same business, same red ink, opposite buckets.

Bad Black Boxes

My point here is not to pick on this one index, or this one fund — although this is to my reading the only one of the five major US style families that uses P/E instead of E/P.

My point is to argue that index methodologies matter. We have beaten to death the changes Nasdaq made to the Nasdaq-100 just to wedge SpaceX in, and S&P choosing the path of righteousness (or at least, sanity) in delaying inclusion for a year (at least). But that's not what's going on here. There is no decision being made about SpaceX. SpaceX hasn't been "chosen" as a value stock, it's been exiled from the land of growth.

Instead we have methodologies developed in more norma" times ... when companies generally went public as smaller, profitable enterprises. Those more-normal times are now running face first into the new-math of modern markets, where anything can happen and the points don't matter. Growth and value have always been a bit squishy and hard to pin down. That's why we have 394 funds promising one or the other -- a substantial percentage of the industry. And sure, some methodologies are better than others. I like the S&P Pure Growth/Value series more than this Dow Jones series, because there's 1/3 of the market that gets ignored for being neither growth nor value enough.

But my honest take? Skip most of them. If you want a real, deep-value contrarian, start hunting for an active manager you actually believe in. If you want shoot-the-lights out momentum growth, well we've got lots of active managers chasing those dollars too.

But don't count on the word value in the name of the fund to comport with your personal definition — it likely can barely comport with its own.