USO Overview

The United States Oil Fund, LP (USO) is the Britney Spears of ETFs: It has a singular schtick, which it performs very, very well—and for which it has earned both the scorn of market pearl-clutchers and the delight of doomsayers, who revel over every dip and tumble.

But just as Britney Spears is a pop star, not the embodiment of societal ruin, USO is just an oil fund, not a Horseman of Market Apocalypse.

USO turns twenty this month, and for all its ups and downs—and there have been many—the fund itself has shown remarkable persistence in an ETF landscape that has grown more ephemeral by the year. USO might not be the fresh-faced pop ingenue it once was. But it remains the queen of commodities, the biggest and best-known futures-backed single commodity ETF, one that’s spawned a generation of copycats and competitors.

Scroll through as we look back at USO’s most iconic moments over the past two decades—but don’t blame us if you start humming “Oops, I Did It Again”

Chart: USO vs. Front-Month WTI Futures, sourced from ETF.com. Data as of March 23, 2026

1. April 2006: The World’s First Oil ETF

Launched nearly 20 years ago in April 2006, the United States Oil Fund LP (USO) was a game changer for the ETF industry.

The fund, which tracked the performance of near-month West Texas Intermediate (WTI) light, sweet crude oil futures, was the first oil ETF on the market, as well as the first single-commodity futures-based ETF.

USO bridged a real market gap: Trading commodity futures was (and is) complex, costly and out of reach to most investors. With USO, though, anybody could take a stance on oil, no margin account required. It made trading oil as simple as trading stock.

Alongside its sibling funds (UNG, UNL, and others), USO threw open the gates to the commodities markets for the masses. The fund’s smash success—within months, USO had added nearly $1B in net new assets, then a mind-boggling sum—cemented issuer U.S. Commodity Funds (USCF) as the reigning monarchs of commodity ETFs for years to come.

2. April 2007: USO Accused of Breaking the Market (For the First Time)

One year after USO’s debut, the Wall Street Journal published a front-page banger, “Why Hot Funds Are Tripping Up Some Investors,” in which the outlet accused many top ETFs of diverting significantly from their benchmarks.

Exhibit A: USO.

As far as we can tell, this article marks USO’s first—but by no means last—media firestorm. And it was largely unwarranted, for the WSJ article claimed USO had “fallen more than 15 percentage points behind the oil price it was designed to track.” Which was true, but also not. While yes, USO’s returns and spot oil prices had diverged, the ETF tracks front-month oil futures, not spot oil—a subtle, but relevant difference.

The article became such a thorn in USCF’s side that the issuer actually filed with the SEC just to correct the record. In it, they argued the author had either mischaracterized USO’s investment objective or miscalculated its total returns.

This was the first of many, many SEC filings USCF would make just to respond to negative press, as the issuer tried to stay on regulators’ good side.

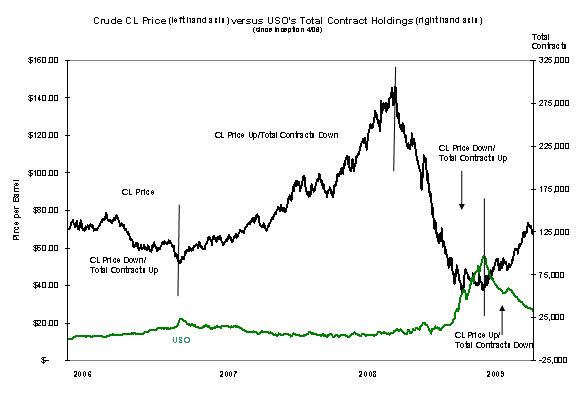

3. July 2008: Commodities Bubble, Then Pop

During the 2007–2008 commodity boom, oil prices surged to record highs. By July 2008, WTI had soared to $145, only to collapse to the low-$30s by year’s end, thanks to the Global Financial Crisis (GFC). Since USO exclusively tracked front-month oil futures, the ETF rode this volatility like a wind surfer, spiking and crashing right alongside crude prices.

As oil rose, the Commodity Futures Trading Commission (CFTC) established a task force to investigate whether speculative investors like USO were driving up oil prices. But the task force’s report largely exonerated speculators:

“While these increases broadly coincided with the run-up in crude oil prices, the Task Force’s preliminary analysis to date does not support the proposition that speculative activity has systematically driven changes in oil prices.”

Not that these findings shifted public opinion, however.

4. February 2009: Panic! At the Roll Period

An ETF that holds futures contracts is constantly in flux. Periodically, the portfolio manager must sell out of contracts about to expire and buy new ones to take their place, in a process known as “rolling.”

In USO’s case, rolling is a monthly affair: Each month, the fund must sell out of the expiring front-month contracts and buy the next-nearest “second” month contracts instead.

Initially, USO completed this trade in a single day. But in February 2009, USCF introduced a four-day “roll period,” progressively spreading the trade over several days.

Today, a rolling period sounds like a no-brainer. But the change raised eyebrows at the CFTC, especially after an employee at UBS Securities, USO’s futures broker, was caught misreporting large block trades during the ETF’s first roll period.

UBS was fined for the infraction, but it was clear the CFTC was watching USO closely, as well.

5. 2009-2011: USO Would Like to Speak to the Manager, Please

As oil prices recovered over the next few years due to inventory shortages and the Arab Spring, critics’ fixation on USO as the driver of higher prices continued.

USCF tried to swat away the negativity with—what else?—SEC filings, with the issuer filing nearly ten 8-Ks over three years to counter the claims.

One popular media theory suggested that USO’s sizable purchases of oil contracts must have increased market demand, thus pushing up prices. But as USCF pointed out (again and again and again and again and again), USO’s futures holdings actually declined as oil prices peaked. Only when prices began to drop did USO begin to increase its holdings:

Source: USCF 8-K, dated July 9, 2008

Another theory argued that persistent oil market “contango”—or a market condition in which futures contracts closer to expiry are cheaper than those farther from expiration—meant USO elbowed oil prices higher with each roll period. USCF countered by pointing out that USO’s roll, which occurred two weeks before expiration, had little demonstrable impact on the price spread between front- and second-month contracts.

Ironically, though, contango was a problem for USO, as it forced the fund to buy high and sell low, leading to a persistent drag on returns. More on that later.

The most disquieting media theory, however, was that USO’s large position size could distort the underlying oil market, if it had to liquidate quickly—a concern echoed by the CFTC. USCF pointed out that even on the fund’s single highest volume days, USO had only bought and sold less than 2% of the oil market’s total daily volume of contracts. Still, in retrospect it’s clear that USO’s position size was a Chekov’s gun primed to fire.

6. October 2011: CFTC Introduces New Position Limits

In late 2011, the CFTC introduced new position limits that prohibited any one trader—including ETFs—from holding more than 25% of the deliverable spot month supply for 28 commodity futures contracts, including crude oil.

The order also introduced limits on how much traders could hold in any given month, as well as in all contracts combined. Traders were limited to 10% or less of all open interest on the first 25,000 contracts in a given month, then to 2.5% thereafter.

The 25% limit was a preventative measure, designed to reduce risk any single trader could amass enough control to manipulate prices, particularly in volatile markets. And oil markets had become volatile indeed, due to ongoing disruptions from the Arab Spring and NATO’s intervention in Libya, which had widened the gap between Brent and WTI prices to historic levels.

7. 2014-2016: U.S. Shale Transforms the Oil Market

For several years, oil prices remained at a (relative) steady-state around $100. But in 2014, new technologies like hydraulic fracking and horizontal drilling enabled U.S. oil producers to tap into the vast, previously inaccessible shale oil reserves located in the United States.

U.S. oil production surged, turning the country into one of the world’s top oil producers overnight. OPEC+ countries, however, refused to cut their own output, hoping to pressure the new upstart with low prices. Worldwide inventories overflowed, and the strategy backfired, as oil prices crashed to as low as $26.

Meanwhile, investors plowed into USO, hoping to buy the dip. The fund added more than $3.7 billion in new net flows from the start of 2014 to year-end 2016.

8. May 2015- December 2016: Musical Chairs in the C-Suite

USCF isn’t a giant like BlackRock or Vanguard, but a small, scrappy firm where every personnel departure can be a seismic event. In May 2015, there were two: John Hyland, the public face of USO for nearly a decade, left as Chief Investment Officer, and Chief Financial Officer Howard Mah followed him out the door.

What followed was a year of executive reshuffling. Former CEO Nicholas Gerber stepped in as Vice President, while long-time portfolio managers John Love and Andy Ngim took over as CEO and COO, respectively. USCF also added Kevin Baum, ex-Invesco Powershares, as Chief Investment Officer—a nice get for USCF, given Baum’s background in launching the first commodities mutual fund at Oppenheimer Funds.

Gerber was also CEO of Concierge Technologies, a digital video equipment manufacturer. But Concierge acquired the sole member of USCF’s LLC in 2016 as part of an expansion to become a holding company. Rebranding to Marygold Companies, the firm later acquired such diverse companies as a Canadian alarms maker and a New Zealand meat pie manufacturer.

9. Spring 2020: Everything Everywhere All At Once

In March 2020, the COVID-19 pandemic sent the world into lockdown mode, closing schools, businesses, and markets. But as oil demand collapsed, major oil producing states like Saudi Arabia and Russia actually increased output, glutting an already saturated market. The result was a historic rout in oil prices, where the price of near-month WTI crude futures briefly went negative and touched -$37.63 on April 20, 2020.

Meanwhile, cooped-up retail investors armed with a Robinhood account and time to kill poured record cash into meme stocks. USO became a favorite rebound play, pulling in more than $5.9 billion in new net assets throughout March and April.

But remember: When oil prices are falling, that’s when USO buys more contracts. Why? Because the ETF must maintain constant exposure to oil prices (i.e., exposure = number of contracts x contract price). So when oil prices drop, USO must buy more second month contracts during its roll to ensure exposure remains undisrupted. USO now found itself in real danger of cornering the futures market, just as they’d been accused of doing ten years prior.

Factor in the oil market’s persistent contango, which forced USO to sell low and buy high on every roll, and USO was in deep doo-doo. The fund still had to meet its investment objective, even as regulators had begun to send stern warnings to USCF not to exceed position limits.

So USCF did the only thing they could: Change USO.

10. April-May 2020: Rapid-Fire Makeovers for USO

Over a two week period, USCF implemented several rapid-fire portfolio changes, broadening USO’s exposure across the futures curve to avoid breaking position limits.

For a brief period, USO even ended up effectively actively managed, with its portfolio managers allowed discretion to invest in any futures contract “in any month available or in varying percentages,” and even in non-crude instruments, “without further disclosure” to investors. The standard four-day roll period was also stretched to ten days, with added flexibility to sell contracts both to track portfolio changes and to satisfy redemption orders.

Concurrently, USO suspended creations, after surging investor demand left it with barely any shares left to issue. USCF petitioned the SEC to allow it to issue another four billion shares.

As if all this wasn’t enough, one day later USO announced a 1-for-8 reverse share split, reducing the number of shares outstanding by a factor of eight, while USO’s share price rose eightfold.

Finally, on May 1, USO adopted a unique ‘waterfall’ portfolio strategy, one that was simple in concept but sprawling in execution.

First, managers would attempt to buy/sell front-month WTI contracts. If position limits or market conditions prevented them from being able to do so, the fund would shift to second- and third-month contracts; and if that wasn’t possible, then several successive configurations of blended-month portfolios spanning the entire twelve month futures curve. And if that wasn’t possible, then the fund could move into Brent oil, diesel oil, RBOB gasoline, and even certain local market contracts. The ten-day roll period remained in place, though USO reserved the right to adjust the timing as needed, even intraday (so long as they published the changes by the end of day). (The ten-day window would eventually shorten to five at the start of 2026.)

The strategy wasn’t perfect, but it was good enough: About six weeks after the waterfall portfolio debuted, the SEC authorized the creation of an additional one billion shares and creations were unsuspended.

11. Summer 2020: Legal Trouble Floods In

The dust had barely settled before a wave of class action lawsuits hit USO.

The suits claimed USCF had not only failed to disclose the extraordinary conditions driving oil demand’s collapse, including the COVID pandemic and the Saudi-Russian price war, but that the issuer had inside knowledge about how these events would impact USO, yet failed to communicate the risks until well after significant losses had occurred and the fund had shifted strategies.

Then the charges came. In August, the SEC sent a Wells notice to USO, USCF, and CEO John Love; the CFTC did the same a few days later. (A Wells notice is a letter sent by a securities regulator informing recipients of impending charges.) Both letters indicated the regulators had found USO and USCF in violation of security laws against fraud and deceit during the brief window when creations had closed and USO’s portfolio had been in flux.

In November of 2021, USO paid a $2.5 million fine to settle the regulators’ charges without admitting fault or guilt. The class action lawsuits were ultimately consolidated and eventually dismissed in September 2025.

12. August 2023: USO Once Again Becomes a Front-Month Fund

While USO’s waterfall strategy remained in place for more than three years, eventually USO reverted to its original strategy. The shift wasn’t instantaneous, however; the transition spanned from the September 2023 to the January 2024 roll.

Even then, the return wasn’t a full reset. USO retained the flexibility to invest beyond the front month and in other oil-related instruments, such as swaps, when needed for liquidity or regulatory reasons.

What didn’t change was the scale or pace of investor flows. By this point, massive creations and redemptions had become routine, with hundreds of millions of dollars moving in and out of the fund in a single day based on swings in the oil market.

Which is why it was almost inevitable that USO would attract attention from the “hot sauce” ETF issuers. In May 2004, Defiance launched the Defiance Oil Enhanced Options Income ETF (USOY), which uses weekly put options on USO to offer investors income, as well as indirect exposure to the underlying ETF. This was in addition to leveraged -/+2X takes on USO, available as early as 2022.

13. 2025: Oil Hits Backwardation

For much of its life, USO had operated under the shadow of contango, leading to a persistent drag on return. In July 2025, however, oil markets flipped to backwardation, as fears of large production disruptions due to the Iran-Israel 12 Day War led consumers to scramble to secure oil for immediate delivery.

When oil is backwardated, expiring front-month contracts are priced higher than those with farther out expiries. Therefore, instead of losing money on the roll, USO began generating a positive roll yield that boosted returns independently of surging oil prices.

In addition, higher interest rates meant USO could earn meaningful income on its collateral, which now began to make a material contribution to its total return.

As a result, USO performance began to outpace that of its underlying WTI front-month contracts—a condition that, thanks to the conflict in Iran, continues even today (in April 2026).

14. 2026: A Wild Start To the Year So Far

So far, 2026 has proved to be just as fast and furious as 2025. On February 28, Operation Epic Fury began in Iran, a joint U.S.-Israeli campaign featuring massive airstrikes on Iranian regime leadership, missile sites, air defenses—and oil fields.

Oil prices sprinted upwards. WTI surged from $65 prior to the conflict to an intraday high near $120 on March 9 (prices settled before the close back to $85). That same day, USO had its biggest trading volume day ever, with $16 billion exchanging hands.

Year-to-date, USO is up roughly 70% as of the beginning of April, with more than $828 million in new net assets flowing into the fund. Notably, it’s also outpacing the WTI front-month contract, which is up about 66%. The same backwardation that powered USO in 2025 remains in place today, and the fund continues to see positive roll yields. (Read: “Surging Oil ETFs Get Extra Boost From Backwardation”)

Where USO goes from here depends largely on geopolitics, though, particularly how the Iran conflict resolves and what it means for global supply. But if history is any guide, you can be assured that whatever happens, USO will be front and center of the action.

And it sure as heck won’t be boring.