ETF Univ: Explaining ETFs’ Greater Tax Efficiency

The reasons why ETFs are so tax efficient.

ETF UNIVERSITY

One of the big selling points for ETFs as investment vehicles is that they’re far more tax efficient than competing mutual funds.

If a mutual fund or ETF holds securities that have appreciated in value, and sells them for any reason, they’ll create a capital gain. These sales can result either from the fund selling securities for a tactical move, due to a rebalancing effort, or to meet redemptions from shareholders. By law, if funds accrue capital gains, they must pay them out to shareholders at the end of each year.

Capital Gains

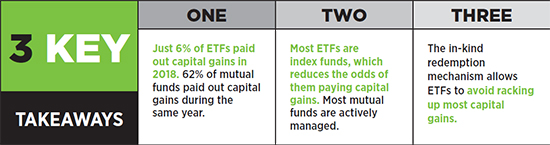

As a general rule, ETFs do much better than mutual funds when it comes to paying out capital gains. In fact, the vast majority of ETFs don’t pay out any capital gains. According to a blog post on the SPDR ETF website, Morningstar data indicates just 6.2% of U.S.-listed ETFs paid out a capital gain in 2018, but more than 60% of mutual funds did so.

Further, during the past decade, the blog notes, the level of ETFs paying capital gains has remained below 10%. Meanwhile, during the same time period, between 16% and 62% of mutual funds have paid out capital gains during those years, and the trend seems to be moving higher over time.

Why such a huge difference? For starters, because they’re index funds, most ETFs have very little turnover, and thus amass far fewer capital gains than an actively managed mutual fund would. And, as the blog notes, 70% of mutual funds are actively managed. However, ETFs are also more tax efficient than index mutual funds, thanks to the magic of how new ETF shares are created and redeemed.

When a mutual fund investor asks for her money back, the mutual fund must sell securities to raise cash to meet that redemption. But when an individual investor wants to sell an ETF, he simply sells it to another investor like a stock. No muss, no fuss, no capital gains transaction for the ETF.

Even Better With APs

What happens when an authorized participant (AP) redeems shares of an ETF with an issuer? Actually, it gets better. When APs redeem shares, the ETF issuer doesn’t typically rush out to sell stocks to pay the AP in cash. Rather, the issuer simply pays the AP “in kind”—delivering the underlying holdings of the ETF itself. No sale means no capital gains.

The ETF issuer can even pick and choose which shares to give to the AP—meaning the issuer can hand off the shares with the lowest possible tax basis. This leaves the ETF issuer with only shares purchased at or even above the current market price, thus reducing the fund’s tax burden and ultimately resulting in higher after-tax returns for investors.

The system doesn’t work so smoothly for all ETFs. Fixed income ETFs, which have more turnover and often have cash-based creations and redemptions, are less tax efficient than their equity brethren.

But all else equal, ETFs win hands-down, with two decades of history showing they have the best tax efficiency of any fund structure in the business.

SELECTED TERMS

Authorized Participant

He or she is the protagonist of the ETF creation/redemption process most investors will never know. Designated by an ETF issuer, the AP is someone with purchasing power who creates and redeems shares of an ETF, keeping the supply elastic to meet demand. When there’s new appetite for a given ETF, the AP will create shares of that ETF through the in-kind creation/redemption mechanism, keeping supply ample and helping the ETF trade in line with its net asset value (NAV). Ample supply means no need for steep premiums. When demand dries up and ETF share prices face a discount, the AP can redeem shares of the ETF from the market, reducing supply, allowing the ETF to trade back in line with its NAV. The AP plays a crucial role in ETF liquidity and trading.

Bid/Ask Spread

ETFs trade like single stocks, so bid/ask spreads are a part of daily life for an ETF. The spread is simply the difference between the price someone is willing to pay for an ETF (the bid) and the price someone is willing to sell that ETF for (the ask). The most important takeaway here is that the wider the spread, the more expensive it is to trade that ETF. That’s why we list the “average spread” for all ETFs in our fund pages (etf.com/ticker) along with other crucial data points such as expense ratio, assets under management and average daily volume. This metric should be part of your ETF due diligence if costs are important to you.

Creation/Redemption Mechanism

It’s how ETF shares are created and redeemed, in a process that’s unique to the ETF structure. When there’s demand for new shares of an ETF, an authorized participant buys the securities the ETF holds, and hands that basket of securities to the ETF issuer in exchange for ETF shares. This is known as an in-kind transaction—securities for shares. In the case of a redemption, this process works in reverse. The in-kind nature of the creation/redemption mechanism is crucial to how ETFs trade because it allows them to trade throughout the day in line with the value of their underlying holdings (their net asset value).

Market Maker

Also known as a liquidity provider, a market maker is someone who facilitates ETF trading, ensuring tight bid/ask spreads, depth and smooth trading throughout the day. Every ETF has a lead market maker, many of which are incentivized by exchanges to keep markets humming along.