Smart Beta Grows In Commodity ETFs

A new index from Dow Jones and RAFI addresses a real issue.

A new index from Dow Jones and RAFI addresses a real issue.

Commodities are notoriously hard to index. While rational people argue about how to make an equity index, it’s fairly easy to agree on a few basic principles like “what is a large-cap stock,” or even more fundamentally, “what’s a stock.”

In commodities, there’s no such common ground. Otherwise-rational people in the commodities world rarely agree on things as simple as whether gold is even a commodity that should be indexed, or which version of oil (Brent or West Texas crude oil) should be included.

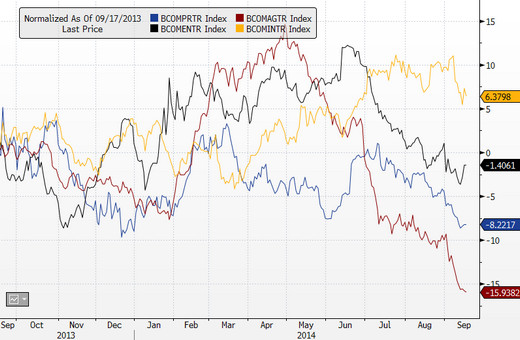

A Nightmare Of Choice

The end result for investors has for the most part been a bit of a nightmare. Consider the returns of the largest commodity ETFs over the last few years:

These are five ETFs all purporting to give you broad exposure to the commodity markets, a classic source of diversification in a sophisticated portfolio. Every one of them is a seemingly logical take on the space.

At the bottom, we have the iPath Dow Jones-UBS Commodities ETN (DJP | B), which has been a pretty consistent underperformer. It’s also extremely odd, in that despite enormous assets of more than $1.5 billion, it tracks an index that no longer exists.

The DJ-UBS commodity indexes became the Bloomberg Commodity Indexes in July, and nobody at Barclays seems to have noticed or bothered to update the ETN’s name, prospectus, fact sheet or website. The index used to and presumably still does track a simple index of 19 commodities using front-month futures and caps on exposure to keep things somewhat balanced.

The Stalwarts

In the middle, we have two long-running and stalwart competitors, the most-quoted iShares S&P GSCI Commodity ETF (GSG | A-100) in brown, and the Greenhaven Continuous Commodity ETF (GCC | A-5) in yellow.

The GSCI is the granddaddy of commodity indexes, weighting mostly on production, which makes energy an enormous part of the portfolio—often more than 70 percent. The Greenhaven index takes exactly the opposite approach, equal-weighting a basket of 17 commodities with an enormous skew toward agriculture—currently almost 15 percent.

In a sense, these are all naive indexes—I won’t call them “dumb,” because to be honest, a lot of very real thinking went into the construction of their answer to the question “what’s the market cap of wheat?”.

Getting Smart In Commodities

The black line is where things start getting interesting—and perhaps a little smarter. The black line is the PowerShares DB Commodity Tracking ETF (DBC | B-90). It not only hedges on the commodity weighting—still using production but creating caps on energy to make it a bit more balanced, it then addresses the really serious problem of commodities investing—contango.

If you’re new to commodities, contango is the condition in which the futures contract for a month down the road is more expensive than the one closest to today. If you hold the December corn contract at $3.42 a bushel, and the March contract is trading at $3.55, and that situation persists right up until December, you have a problem.

Unless you really want a truckload of corn, you have to sell your December contract. If you want to maintain your exposure, you’re going to have to buy something, and you’ll most likely buy March. And as anyone who’s ever played Monopoly will tell you, selling low and buying high is a terrible way to make a living.

While there are exceptions, for the past 10 years, most commodities have been in contango most of the time. That means naive structures like the GSCI get hit right on the head with contango, month after month.

Mitigating Contango

DBC was one of the first ETFs to implement a different approach. DBC tries to mitigate the effect of contango by using a formula to select contracts (further out the curve) that will generally be less impacted by contango. It’s generally worked well, but can sacrifice some responsiveness to changes in spot prices in exchange for this contango-beating selection.

The top line (which I will acknowledge I own) is when the industry really started getting smart. The United States Commodity Fund (USCI | C-10) doesn’t even try to pretend it’s providing exposure to an asset class. And honestly, I think that’s pretty reasonable. The correlation between different parts of the commodity universe is tenuous at best. Consider how the major commodity sectors have done just this year:

It’s a mess. Sure, sometimes the energy commodities (the black line represents the Bloomberg Energy Index) and, say, industrial metals (the yellow line) go in the same direction, but other than broadly participating in the global economy, there’s no real reason to expect zinc and natural gas to have anything to do with each other.

So USCI takes the approach of just saying “commodities is our playground, let’s go try and make some money.” Every month, it picks the seven commodities that have the least contango—in other words, the ones in backwardation, where instead of paying to roll, you get paid to roll—and adds the seven commodities with the strongest price momentum, and then just equal-weights them.

The resulting portfolio changes dramatically from month to month. Sometimes it’s loaded up with agriculture. Sometimes it’s all about oil. It is, in fact, an active management strategy in snazzy Geert Rouwenhorst indexing clothes.

Is it a guaranteed winner? Of course not, and USCI has had a rocky patch here and there since launch. But it at least acknowledges that indexing commodities is a bit of a mug’s game, and seeks to profit from what’s most interesting about commodities—market structure.

Enter RAFI

Last week, the smart guys at Research Affiliates partnered with S&P Dow Jones Indices to create the Dow Jones RAFI Commodity Index. And more importantly, it’s at the front end of what I expect to be a rash of innovation in commodities.

The approach is fairly simple—RAFI is taking the 23 equal-weighted commodities in the Dow Jones Commodity Indexes (not to be confused with the old Dow Jones-UBS indexes that are now the Bloomberg Commodity Indexes) and then reweights them based on momentum and roll yield.

If that sounds familiar, it’s because it’s fundamentally (pardon the pun) the same strategy being used by USCI—the main difference being that USCI doesn’t really care whether it’s “representative” of the commodity markets, and this new index will at least try and maintain some broad exposure to commodities.

It’s a great threading of the needle between DBC and USCI for investors. There are no ETFs currently trading on this brand-new index. In fact, you’ll be hard-pressed to find much data on whether the strategy works, or really anything beyond its methodology documents at the moment.

But I still think it’s enormously exciting. If there’s one part of the market that really needs smarter beta, it’s commodities.

At the time the article was written, the author held a position in USCI. You can reach Dave Nadig at [email protected], or on Twitter at @DaveNadig.