Akre ETF Is Betting the Market Is Wrong on AI

The fund has lost nearly a fifth of its value since converting from a mutual fund in October. Manager John Neff isn't backing down.

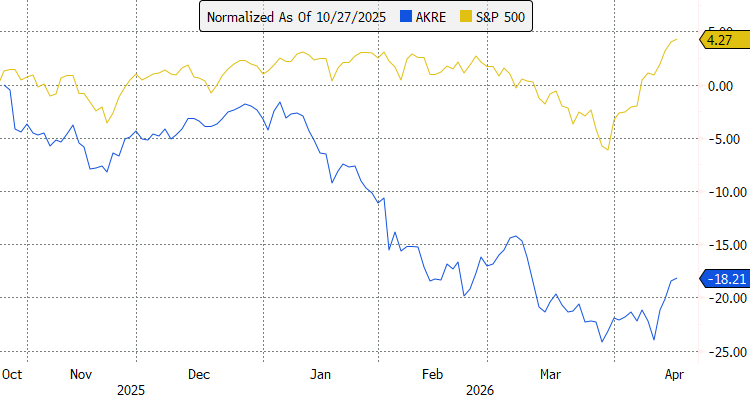

The Akre Focus ETF (AKRE) picked a rough moment to become an ETF.

Six months after converting from a mutual fund in late October, the fund has been battered by a combination of poor performance and outflows.

It became an ETF with just under $11 billion in assets and now sits at roughly $6.7 billion. Since the conversion, AKRE is down about 18.2%, while the S&P 500 has gained 4.3% over the same stretch.

The damage is relatively recent. On June 30, 2025, when it was still a mutual fund, AKRE was up more than 20% on a trailing one-year basis, comfortably ahead of the S&P 500. But the fund's bets turned sharply against it in the months that followed.

The pain has dragged longer-term numbers below the benchmark as well. On a five-year basis, AKRE has returned 2.8% annualized versus 12.1% for the S&P 500. Since the fund's inception in August 2009, AKRE has compounded at 12.8% against 14% for the index.

AKRE represents the bulk of Akre Capital Management's AUM, with roughly $1 billion more in long/short private investment funds and the remainder in separately managed accounts. The ETF carries a 0.98% expense ratio.

The fund follows what Akre calls a "three-legged stool" approach, buying businesses with durable competitive advantages that can compound free cash flow per share at high rates, strong management teams, and meaningful reinvestment runway.

Two Bad Narratives

The fund’s top holdings tell the story of what has gone wrong. Mastercard is the largest position at 12.4% of the portfolio, followed by Constellation Software at 11.9%, Brookfield Corporation at 9.2%, and KKR at 8.7%.

Beyond those, the fund holds a cluster of software and information services names, including Roper Technologies, ServiceNow, Salesforce, Topicus.com, Moody's, CoStar, and Fair Isaac.

Two market narratives have dragged the portfolio down. The first is AI disruption fear, which has pummeled software and data-services businesses whose moats investors are now questioning. The second is mounting concern over private credit, which has hit alternative asset managers like Brookfield and KKR.

The two themes are connected, since a notable amount of private credit lending has gone to software companies.

Doubling Down On Software

In the fund's first-quarter letter, John Neff—Akre's CEO, CIO, and portfolio manager—defended his stocks.

"While we have not owned the AI 'poster children' (e.g. chips, chip equipment and memory makers, etc.) our portfolio is not anti-AI; quite the opposite. We believe the businesses [we own] stand to be enormous beneficiaries of AI tools and efficiencies without incurring or depending upon the enormous buildout costs associated with AI infrastructure," he said.

Neff suggested that AI models and coding tools will be largely commoditized, which will benefit traditional software companies that can use them at low cost.

That view is essentially the opposite of where the market has landed. The prevailing narrative is that AI model developers and AI-native application builders, such as companies like Anthropic, Google, and OpenAI, represent an existential threat to the incumbent software businesses that dominate AKRE's portfolio.

Neff similarly defended his positions in alternative asset managers, noting that only a limited amount of total AUM at KKR and Brookfield is tied to private credit with even less exposed to software specifically.

“KKR recently disclosed that its [software] exposure was just 7% of total AUM while Brookfield recently disclosed that total software exposure comprised just 1% of private equity AUM,” he said.

The upshot is that Neff is leaning into a deeply contrarian bet rather than abandoning it. The letter reads as a defense of the strategy rather than a reassessment of it.

If he's right that AI software disruption fears are overblown and that private credit concerns won't meaningfully impair KKR and Brookfield, the portfolio's compressed valuations offer a lot of upside.

If he's wrong, there isn't much in the fund that isn't exposed to one or both of those narratives. Investors in AKRE should be clear-eyed about the bet he’s actually making.