Congress May Complicate ETFs That Track Lawmakers’ Trades

A House bill aimed at curbing congressional stock trading is advancing, and it could undermine the strategies behind ETFs built on lawmakers’ disclosures.

For years, investors have been able to piggyback on the stock trades of U.S. lawmakers. But a bill advancing in the House this week could make that much harder, potentially undermining the strategies behind two of the market’s most controversial ETFs.

On Wednesday, the Stop Insider Trading Act cleared the House Committee on Administration, marking rare progress in Congress’s long-running, and usually fruitless, effort to curb lawmakers’ stock trading. The bill would ban members of Congress, their spouses, and their dependent children from buying individual stocks and require advance public notice before selling existing holdings.

The legislation still faces steep odds. It must pass the full House, survive the Senate, and be signed by the president. But its movement alone is notable in a space where many similar bills have gone nowhere.

If it ever became law, it could strike at the heart of two ETFs built entirely around congressional trading activity: the Unusual Whales Subversive Democratic Trading ETF (NANC) and the Unusual Whales Subversive Republican Trading ETF (GOP).

How These ETFs Work

NANC and GOP are actively managed ETFs that hold stocks based on trades disclosed by sitting members of Congress and their families under the STOCK Act.

That law, passed in 2012, requires lawmakers to file Periodic Transaction Reports disclosing stock trades within 30 to 45 days. Using those disclosures, the fund manager builds portfolios based on which stocks lawmakers bought or sold while in office.

Stocks that see larger or repeated purchases, or activity from multiple lawmakers, tend to be overweighted. One off or small trades may be underweighted or excluded entirely. The ETFs typically aim to hold between 100 and 200 stocks.

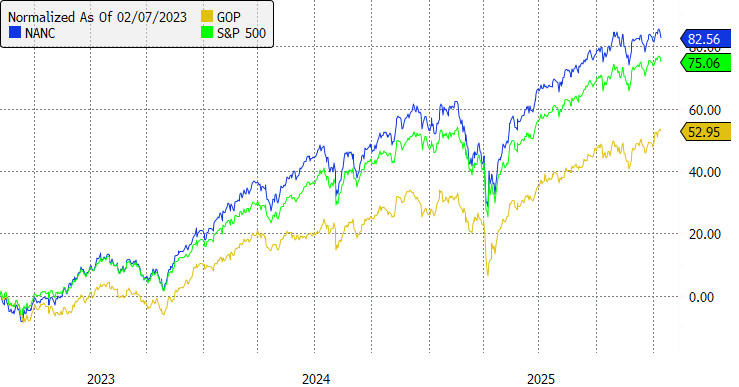

So far, the funds have produced mixed results. Since inception, NANC has gained roughly 82%, outperforming the S&P 500’s 75% return over the same period, while GOP has risen about 53%.

Investor interest has largely mirrored performance. NANC has attracted about $268 million in assets, compared with roughly $67 million for GOP. Both charge expense ratios of 0.74%.

The portfolios look very different. GOP’s top holdings currently include Comfort Systems USA, JPMorgan, the iShares Bitcoin Trust ETF, Intel, and Nvidia. NANC’s largest positions skew toward mega cap technology stocks, with Nvidia, Microsoft, Alphabet, Amazon, and Apple dominating the top of the portfolio.

Issues With the ETFs

While the strategies behind NANC and GOP sound compelling, and in NANC’s case have worked well enough to outperform the broader market, there are important caveats.

For one, even though the strategy aims to be systematic by following what politicians buy and sell, the actual implementation requires a significant amount of subjective judgment. Portfolio managers decide how aggressively the funds respond to new disclosures, how trades are netted, and which positions are filtered out.

We have seen a similar dynamic before. The now defunct Long Cramer Tracker ETF (LJIM) and Inverse Cramer Tracker ETF (SJIM), which bet on and against CNBC personality Jim Cramer’s long list of stock picks, struggled following poor performance and limited investor interest.

In this case, performance has been stronger, at least for NANC, and investor interest has been solid. That suggests some investors remain comfortable with the tradeoffs involved in the strategy.

Still, the ETFs carry a unique risk. If Congress ever imposed a true stock trading ban, the strategy behind NANC and GOP would become effectively unworkable. No trades would mean no disclosures, and no disclosures would mean no usable signal.

For now, the ETFs will continue to operate as they do today. But if legislation meaningfully restricting congressional stock trading were to gain traction, their long term viability would come into question.

Why This Debate Keeps Coming Back

The STOCK Act made congressional trading more transparent, but it never banned it outright. Enforcement has been uneven, penalties are modest, and late filings are common. Some lawmakers continue to profit from trades that, at a minimum, raise questions about conflicts of interest, fueling public anger.

Since 2020, multiple bipartisan bills have been introduced to ban or restrict lawmakers’ stock trading. Most stalled in committee, and none became law.

The Stop Insider Trading Act takes a narrower approach than many prior proposals. Rather than forcing lawmakers to divest existing holdings, it focuses on banning new stock purchases while tightening disclosure requirements around sales. It also targets individual stocks rather than all financial assets, which may help explain why it has advanced further than past efforts.