JEPI, MSTY Under Fire: Hedge Fund Manager Slams Covered Call ETFs

Benn Eifert warns against crowded option strategies, a category that includes blockbuster funds like JEPI and MSTY.

Hedge fund manager Benn Eifert didn’t mince words when it came to covered call strategies, like those powering some of the most popular ETFs.

“Systematically, blindly selling options is a BAD IDEA. Underperforms owning equities by a lot,” Eifert wrote on X, accusing “charlatans” of trying to “farm retail investors.”

Eifert, managing partner and co-CIO at QVR Advisors, said these strategies looked good before 2010, when options markets were “sort of a backwater” and risk premiums were relatively high.

But by 2012, that edge had eroded. Pension consultants began pitching “equity-like returns with lower risk via options selling” to massive institutional clients, pulling tens of billions of dollars into the strategies.

Retail investors—both DIY traders and those buying through wealth managers—piled in as well.

More recently, covered call and other option‐selling strategies have proliferated within ETFs, turning what was once a niche institutional tactic into a mainstream income play for retail investors and advisors alike.

That flood of capital into one-month, near-the-money options changed the market structure, Eifert argued, depressing premiums and shifting the performance gap in favor of simply owning equities.

“Selling that call is just a trade. You’re going to lose money on that trade if the stock goes up enough,” Eifert said. “And if the stock is volatile—goes up a lot and then down a lot—you’re going to get hosed. Because when it goes down a lot, you just collect a small premium, but when it goes up a lot, you get your face ripped off. This is the precise nature of a short volatility trade.”

The Return Gap

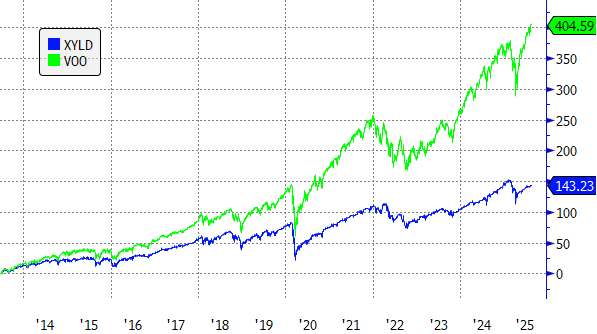

The numbers bear out his point. The Global X S&P 500 Covered Call ETF (XYLD), which writes monthly at-the-money calls on the S&P 500, has returned 143% since its 2013 inception. The Vanguard S&P 500 ETF (VOO) is up 405% over the same period.

The Global X Nasdaq 100 Covered Call ETF (QYLD) shows a similar pattern: 138% since launch versus 639% for the Invesco QQQ Trust (QQQ).

JEPI Makes The Same Trade-Off

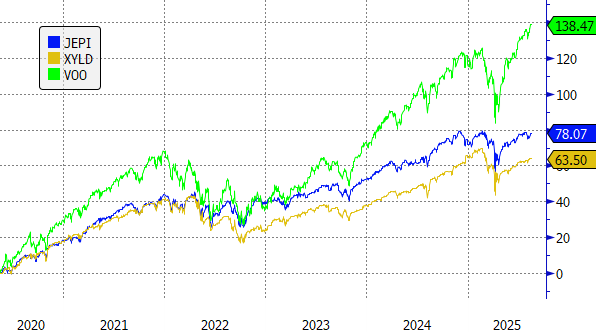

Even the JPMorgan Equity Premium Income ETF (JEPI), the largest actively managed ETF with $41 billion in assets, can’t escape the structural drag of continuously selling calls.

JEPI holds an actively managed, low-volatility, value-tilted portfolio, then uses equity-linked notes (ELNs) to write one-month, out-of-the-money calls on the S&P 500.

According to JPMorgan marketing materials, JEPI aims for roughly 6–10% in annual distributions plus some equity upside. Since its 2020 debut, it’s up 78%, beating XYLD’s 64% but still well behind VOO’s 138%.

Some fans argue these funds are “yield plays” and shouldn’t be compared directly to standard stock funds. Indeed, JEPI’s own site compares its yield to U.S. high-yield bonds and the 10-year Treasury.

But unlike bonds, JEPI remains exposed to much of the downside of equities (minus the premium captured from selling calls).

When the S&P 500 fell 19% from February to April during this year’s tariff turmoil, JEPI slid 14%.

By comparison, the iShares MSCI USA Min Vol Factor ETF (USMV), which also targets low-vol stocks but without selling calls, fell just 9.7% in that span (incidentally, since JEPI’s inception, USMV is up 73%, not that different from JEPI’s 78%).

Single-Stock Covered Call ETFs

Eifert also took aim at the boom in single-stock covered call ETFs, such as those from YieldMax.

“There are tons of YieldMax ETFs doing covered calls on single names now. Look at every single one of them and compare it to owning the underlying. You’re just losing money.”

One of the most popular, the YieldMax MSTR Option Income Strategy ETF (MSTY), writes calls on MicroStrategy. It boasts a headline 84% distribution rate and has pulled in $5.3 billion of its $5.6 billion in assets this year alone.

But since launching in February 2024, it’s up 272%, sharply lagging the 420% gain for MSTR stock.

Eifert stressed he wasn’t saying investors should never sell options. “But don’t blindly sell the same options that everyone else is selling, because YouTube and Instagram influencers are telling you to and pasting MS Paint screenshots of fake PNL.”