As Mega Caps Stall, Equal Weight Makes a Comeback

After years of lagging a top-heavy S&P 500, RSP is outperforming in 2026.

Concentration risk has been a concern for investors for years.

As the biggest companies have grown larger, an increasing share of market-cap-weighted indexes has become concentrated in a handful of stocks. Today, roughly 39% of the S&P 500 is accounted for by its 10 largest constituents, including Nvidia, Alphabet, Apple and others.

That has led some investors to worry that if just a few of these stocks stumble, the entire index could suffer.

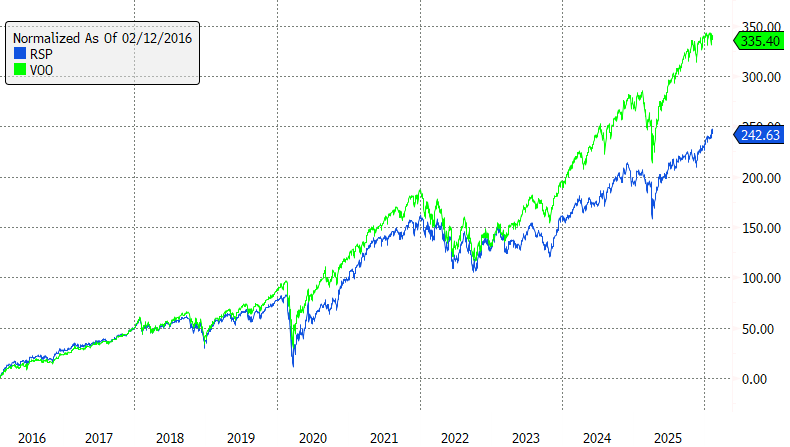

So far, that fear hasn’t materialized. In fact, attempts to reduce concentration risk through equal-weight strategies have largely backfired. Over the past 10 years, the Vanguard S&P 500 ETF (VOO) is up 335%, compared with 243% for the Invesco S&P 500 Equal Weight ETF (RSP).

A Shift in Performance

This year, the narrative has shifted slightly.

Mega-cap technology stocks have taken a hit amid concerns about AI-related overspending and rising capital expenditures. At the same time, smaller stocks have benefited as investors rotated into other parts of the market.

As a result, the mega-cap-heavy S&P 500 is barely positive this year, while RSP is up more than 5%.

That doesn’t amount to vindication just yet. Equal weight has a lot of ground to make up. But if performance continues to hold up, investors worried about concentration risk may keep gravitating toward the strategy.

So far this year, $6.5 billion has flowed into RSP, bringing total assets to roughly $87 billion.

Different Philosophies

RSP effectively follows a buy-low, sell-high strategy. It systematically rebalances, trimming winners and adding to laggards. The traditional S&P 500, by contrast, lets winners ride. They reflect two very different philosophies.

Under equal weighting, Apple, with a market cap of roughly $4 trillion, has the same weight as Best Buy, with a market cap of about $13 billion, at approximately 0.18% each.

In the standard S&P 500, Apple represents about 6.9% of the index, while Best Buy is closer to 0.02%. Equal weight is therefore significantly underweight mega caps and overweight smaller constituents relative to the benchmark.

A Historical Weight Alternative

Another newer fund takes a different approach to concentration risk.

The Tema S&P 500 Historical Weight ETF (DSPY) uses historical averages to determine position sizes. For example, since 1989, the largest stock in the S&P 500 has averaged a 4.2% weighting. DSPY weights today’s largest stock at that historical level. Nvidia, which sits at roughly 7.8% in the traditional index, is weighted at about 4.2% in DSPY.

The strategy appears to be gaining traction. The fund has accumulated $807 million in assets just 10 months after launch.

Performance has landed between VOO and RSP so far this year, with DSPY up about 2.3%.

Whether investors choose to let winners run, systematically rebalance into laggards, or anchor to historical norms will depend on how concerned they are about concentration, and what they believe is the right way to address it.