ORR ETF Blows Past Market With Strong 2026 Returns

After strong gains in its first year and a fast start to 2026, David Orr’s long/short ETF is pulling in assets.

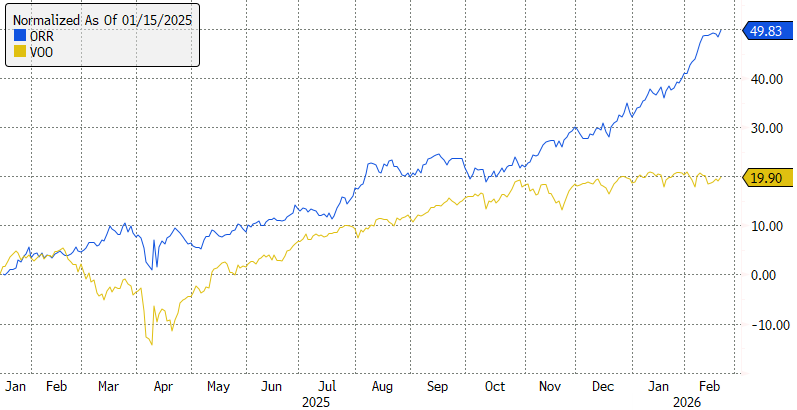

The Militia Long/Short Equity ETF (ORR) has surged out of the gate in 2026 and investors are starting to notice. The long/short ETF is up 13.4% this year on top of last year’s 32.2% gain. The fund launched on Jan. 14, 2025.

Managed by David Orr, founder and CIO of Militia Investments, ORR is the public-market version of a strategy he also runs in a long/short global hedge fund. Investors have been adding capital at an accelerating pace. The ETF has pulled in $220 million in less than two months this year, building on the $163 million of inflows it saw in all of last year. Assets now stand at $443 million.

Orr’s hedge fund oversees more than $160 million. The two vehicles overlap heavily, but they are not identical. The hedge fund invests in more illiquid opportunities and runs higher leverage, while the ETF focuses on positions that can scale inside the ETF wrapper.

“Many of the investments in my hedge fund are illiquid and I won’t be able to trade them if my hedge fund grows too big. However, well over half of my bets scale well and ORR will invest in that portion,” Orr wrote when the ETF launched.

According to Militia Capital’s website, the hedge fund has delivered annualized returns of 50.2% since inception in 2021, with a 15.7% maximum drawdown and a 0.12 correlation to the S&P 500.

Despite the ETF’s structural constraints, its early results have been strong at roughly 2.5 times the S&P 500’s return over the same timeframe.

An Expense Ratio That Isn’t What It Looks Like

One of the more jarring figures tied to ORR is its 14.2% expense ratio.

But only 1.3% represents the management fee paid to Militia Investments. The rest reflects the mechanics of running a leveraged long/short strategy, including dividend expenses on short positions, borrow costs and margin interest.

When a fund shorts a stock or ETF, it must pay that security’s dividend. Economically, however, the underlying typically declines by roughly the same amount when the dividend is paid. Shorting also involves paying to borrow shares, though the fund earns interest on the cash generated from short sales, potentially offsetting that cost.

So while the headline expense ratio number looks extreme, much of it reflects the accounting mechanics of shorting and leverage rather than the fee paid to the fund manager.

Positioning and Philosophy

The ETF typically targets 150% long and 100% short exposure. The hedge fund has generally operated closer to 200% long and 100% short, meaning the ETF carries less gross leverage.

“My strategy exploits two market anomalies. First, less volatile stocks have higher returns. And second, small stocks also have higher returns,” Orr said.

He avoids rigid labels and complex modeling, instead boiling ideas down to "a key variable or two.” On the short side, he looks for failing businesses and catalyst-driven setups.

“Most shorts are simply failing businesses where liabilities exceed assets and future cash flow. I see these companies as melting ice cubes.”

Risks

Orr is explicit about the two biggest risks facing his strategy: leverage risk and short risk.

“It’s possible that longs drop and shorts rise at the same time. If 200% long drops 20% while 100% short rises 20%, the fund would lose 60%,” he said of his hedge fund.

Meanwhile, shorting carries asymmetric risk.

“Shorts have unlimited upside potential and bad companies sometimes spike hundreds of percent for seemingly no reason,” he wrote, recounting a Chesapeake Energy short that jumped 700% and forced him to reduce exposure.

Portfolio Snapshot

ORR’s top holdings currently include Taiwan Semiconductor (7.9%), Sprouts Farmers Market (7.5%), Hikari Tsushin (6.3%), Energy Transfer (6.1%) and Grupo Aeroportuario del Centro Norte (5.1%).

Alphabet is the largest U.S. big tech name at 4.5%. The fund holds about 21% in cash.

On the short side, the largest positions are ETFs, like the iShares Russell 2000 ETF (IWM) at 20% of assets, Invesco QQQ Trust (QQQ) at 20% and Global X SuperDividend ETF (SDIV) at 6.1%.

At launch, Orr cautioned that the strategy might lag in a strong bull market.

“This strategy will typically have lower correlation and beta to the market than most public investments. This means that during a strong bull run ORR will have a tough time keeping up. But in a weak market ORR is expected to outperform,” he said.

So far, however, ORR has outperformed even in a strong tape while maintaining relatively muted volatility.

It remains early. As with any active strategy, continued success will depend on disciplined execution, risk management and ORR’s ability to maintain his edge as assets scale.

But the ETF has quickly positioned itself as one of the more distinctive entrants in the growing active ETF space.