UnitedHealth Rout Sends Shockwaves Through Health Care ETFs

UnitedHealth’s steep decline rippled through healthcare ETFs.

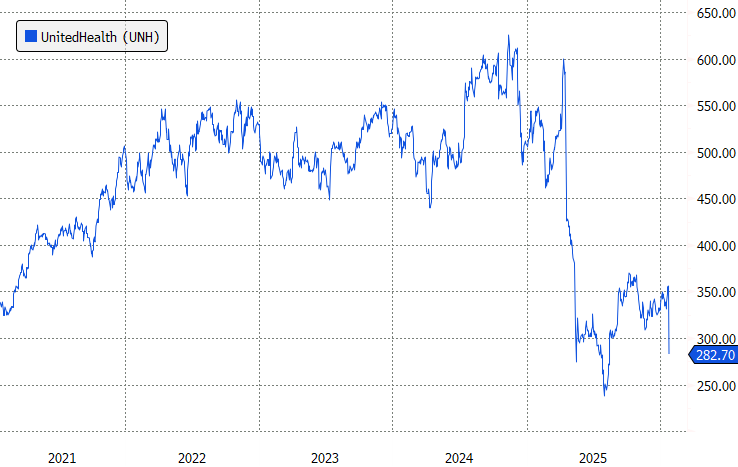

Shares of UnitedHealth Group plunged nearly 20% Tuesday after investors reacted to a one-two punch of Medicare Advantage payment pressure and company guidance pointing to its first annual revenue decline in decades.

The quarterly results themselves were not the primary issue. UnitedHealth reported adjusted earnings of $2.11 per share for the fourth quarter, roughly in line with expectations, while revenue of $113.2 billion came in slightly below estimates. For full-year 2025, revenue totaled roughly $448 billion, up 12% from the prior year.

The shock came from the outlook.

UnitedHealth said it expects 2026 revenue of about $439 billion, implying a roughly 2% year-over-year decline. Management attributed the drop to “planned right-sizing across the enterprise.” If realized, the decline would mark UnitedHealth’s first annual revenue contraction since 1989.

The Medicare Advantage Drag

At the center of the selloff is Medicare Advantage, the privately run alternative to traditional Medicare in which insurers are paid by the federal government to manage healthcare for seniors. On Monday, regulators proposed keeping Medicare Advantage payment rates roughly flat next year, a move that falls well short of Wall Street expectations.

For years, insurers were able to rely on steady payment increases and rapid membership growth to boost earnings. In more recent years, however, rising medical utilization, increased government scrutiny, and a crackdown on billing practices have turned Medicare Advantage from a tailwind into a growing drag on profitability.

The latest policy proposal only adds to those pressures. UnitedHealth said it now expects Medicare Advantage membership to contract by roughly 1.3 million to 1.4 million members in 2026.

EPS to Grow

Despite the revenue decline, the company expects adjusted earnings per share of at least $17.75 in 2026, representing growth of more than 8.6%.

The guidance reflects a shift from growth toward profitability, with management prioritizing margins and operational discipline over top-line expansion.

“[We are] focusing on what is working, what needs more attention, and what no longer makes sense for us. We are driving greater operational disciplines in all our business practices, leveraging the use of technology and artificial intelligence broadly, and renewing our commitment to innovation, agility, and accountability. We have removed assets that are not aligned with our focus on serving the US health system,” Stephen J. Hemsley, CEO of UnitedHealth Group said on the conference call.

Sector-Wide Fallout Hits Insurers and ETFs

The selloff quickly spread beyond UnitedHealth. Other insurers with heavy Medicare Advantage exposure were also hit hard on Tuesday. Humana, the most Medicare-focused of the large insurers, fell more than 20%, while CVS Health and Elevance Health posted double-digit declines.

That pressure impacted healthcare ETFs. The $800 million iShares U.S. Healthcare Providers ETF (IHF) fell roughly 10% on the day, dramatically underperforming both the broader healthcare sector and the overall market.

Despite its name, IHF is dominated by insurers. UnitedHealth alone accounts for about 23% of the portfolio, followed by CVS Health, Elevance Health, Cigna, and Humana. With little exposure to pharmaceutical or medical device companies that can help offset insurer weakness, the ETF is especially sensitive to movements in the stocks of health insurers.

Meanwhile, broader healthcare ETFs weren’t spared, though the damage was more limited. The Health Care Select Sector SPDR Fund (XLV) fell 1.7% on the day, sharply underperforming the S&P 500’s 0.4% gain. Over the past year, XLV has gained about 5.4%, well behind the broader market’s roughly 16.1% return.

A Long Fall From the Peak

While still a giant, UnitedHealth’s influence in major indexes has declined sharply. At its peak in 2024, the company carried a market capitalization of roughly $575 billion. After Tuesday’s collapse, that figure has fallen closer to $260 billion.

Last year, Berkshire Hathaway disclosed a small position in UnitedHealth, representing roughly half a percent of Berkshire’s publicly traded equity portfolio. While Berkshire’s exact purchase price is unknown, the timing suggests the stake was likely initiated in the low-$300s, meaning the investment now appears underwater following the recent selloff.

For a stock once viewed as one of the safest compounders in corporate America, the reversal has been dramatic.

While UnitedHealth shares remain above last year’s lows, when concerns around Medicare payments, utilization, and regulatory scrutiny first surfaced, Tuesday’s move underscores that investors are still uneasy with the stock in a slower-growth, more tightly regulated environment and are continuing to reassess what the company is worth under those conditions.