Why Oil ETFs Are Beating Oil This Year

Oil prices are down sharply in 2025, but USO and BNO are holding up far better than the crude benchmarks they track.

It’s been a tough year for crude oil, but thanks to a quirk in the futures market, investors in oil ETFs haven’t felt the full brunt of the sell-off.

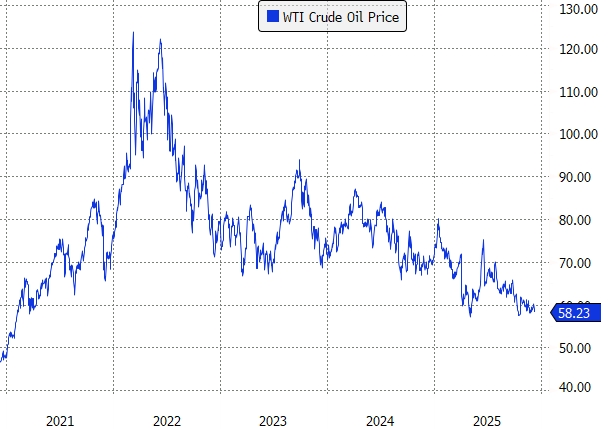

WTI crude oil, the U.S. benchmark, started the year around $72 per barrel. It briefly touched $80 in January before sliding to a low of $57 in May, and it’s now closing out the year not far from that level. For 2025, WTI is down 18.8%, slightly worse than the 17% drop in Brent crude, Europe’s primary benchmark.

Yet the ETFs tied to those markets, the United States Oil Fund (USO) and the United States Brent Oil Fund (BNO), have fallen only 7.7% and 4.6%, respectively.

These funds hold near-month futures contracts in an attempt to track spot oil prices. Because futures contracts expire each month, the funds must “roll” their positions into the next contract. Whether that roll helps or hurts performance depends on the shape of the futures curve.

Understanding the Roll Effect

If the fund must roll into a higher-priced contract—a situation known as contango—it results in selling low and buying high. That drag compounds over time.

If the next contract is lower-priced, a condition called backwardation, the fund effectively sells high and buys low, creating a tailwind.

This year, the oil futures curve has consistently been in backwardation. That dynamic boosted the returns of USO and BNO relative to spot crude, cushioning investors against the steep drop in prices.

The geopolitical backdrop—tensions involving Russia, ongoing OPEC+ supply management, and concerns about shipping routes— kept spot barrels in high demand for much of the year, supporting backwardation.

But the fundamentals are shifting.

A Shift in the Supply–Demand Balance

Oil supplies are ample today. The International Energy Agency estimates global oil supply increased a massive 6.2 million barrels per day from January through November. It expects production to rise another 2.5 million barrels per day next year. Demand growth, meanwhile, is forecast at less than 1 million barrels per day.

Inventories are building, easing worries about disruptions and putting sustained pressure on crude prices.

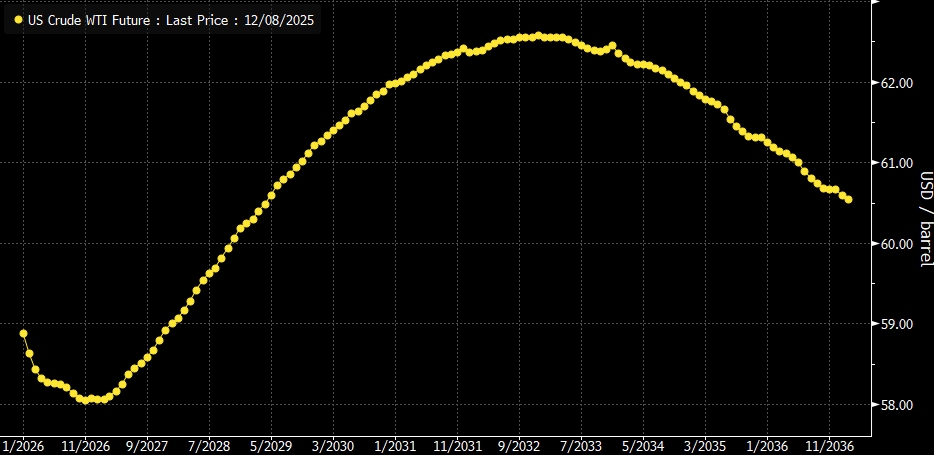

For now, the front end of the futures curve remains in backwardation, but only marginally. Farther out on the curve, contango has already returned.

Source: Bloomberg

The Backwardation Boost

Backwardation has been a huge boon for oil ETFs. Over the past five years, USO and BNO are up 117% and 128%, respectively, compared to gains of 24.5% and 23.3% for front-month WTI and Brent futures. That performance gap is almost entirely due to persistent backwardation.

If the curve flips decisively into contango, that tailwind turns into a headwind. And given the supply outlook, that’s a real risk heading into 2026.

For now, ETF investors are still benefiting from the roll yield. But the futures curve, more than the price of oil itself, may dictate where returns go next.