Swedroe: Opinion Shift On Hedge Funds

Investors seem to be wising up to the fact that hedge funds have consistently underperformed.

Hedge funds entered this year coming off their ninth-straight year of trailing U.S. stocks (as measured by the S&P 500 Index) by significant margins. And for the 10-year period ending 2017, one that included the worst bear market in the post-Depression era, the HFRX Global Hedge Fund Index produced a negative return (-0.4%), underperforming every single major equity and bond asset class.

The market is starting to take notice as well. At the end of the second quarter, there were 8,413 hedge funds, down slightly from a peak of 8,474 in 2015. During the last quarter, two large hedge funds announced they will be liquidating and returning capital to investors.

The larger of the two, Highfields Capital, plans to return $12.1 billion to investors. Tourbillon Capital Partners will be returning roughly $1 billion after six years in operation, citing a lack of distinct advantages. In 2015, the fund was managing about $4 billion. In addition, Criterion announced recently that it was closing its $2 billion fund.

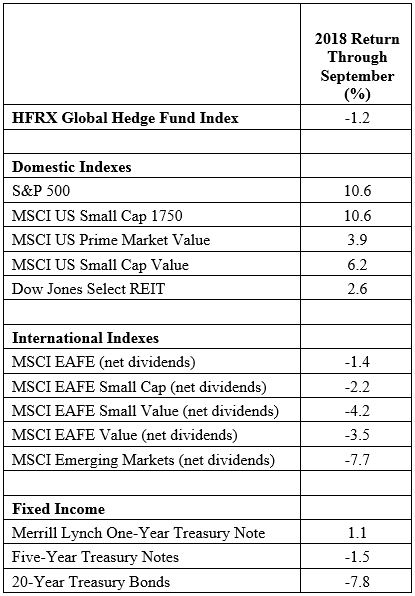

The following table presents returns through the first nine months of 2018 for various equity and fixed-income indexes. The HFRX Global Hedge Fund Index returned -1.2% over that period.

As you can see, the hedge fund index underperformed all five U.S. equity asset classes, but outperformed all five of the international equity asset classes and two of the three bond indexes (one by just 0.3 percentage points). We can take our analysis a step further, however, and determine how hedge funds performed against a globally diversified portfolio.

Key Comparisons

An all-equity portfolio allocated 50% internationally and 50% domestically, equally weighted among the indexes from the table within those broader categories, would have earned 1.5% through September, outperforming the hedge fund index by 2.7 percentage points.

Another comparison we can make is to a typical balanced portfolio of 60% equities and 40% bonds. Using the same weighting methodology as above for the equity allocation, the portfolio would have earned 1.3% using one-year Treasuries (outperforming the hedge fund index by 2.5 percentage points), earned 0.3% using five-year Treasuries (outperforming the hedge fund index by 1.5 percentage points), and lost 2.2% using long-term Treasuries (underperforming the hedge fund index by 1 percentage point).

Given the results, and the wide dispersion of returns between U.S. and international equities, one might think hedge funds would have used their freedom to move across asset classes, which they often tout as their big advantage, to better effect.

Advantage Becomes Handicap?

The problem is that the efficiency of the market, as well as the cost of the effort, can turn that supposed advantage into a handicap. Given the evidence on hedge funds’ underwhelming results, it’s a puzzle why they still manage about $3.2 trillion in assets.

There’s one other point worth discussion. Many articles have claimed that indexing, and passive investing in general, is ruining the market by negatively impacting the price discovery function.

That seems to me a ludicrous belief given that, according to the Investment Company Institute, at the end of 2017, there were 9,356 mutual funds, 530 closed-end funds, 1,897 ETFs and 5,035 UITs for a combined total of more than 16,800 funds all at work at price discovery.

What’s more, according to the Thomson Reuters Lipper second quarter 2018 snapshot of U.S. mutual funds and exchange-traded products, active funds of all kinds, including money market funds, managed about $16.4 trillion.

I’ll report back again on hedge fund performance after the end of the year.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.