Swedroe: Solid Case For Active Mgmt

Wait! It’s not what you think …

I bet you never thought you would read that particular string of words in anything I wrote, let alone a headline. And, to be clear, I didn’t.

The title of this post was actually part of the concluding statement of a study on which I was recently asked to comment: “Decomposition of Total Volatility: How Important Is Idiosyncratic Risk?” by Indrani De of TIAA and Joshua Nutman of BlackRock. The paper was published in September 2015.

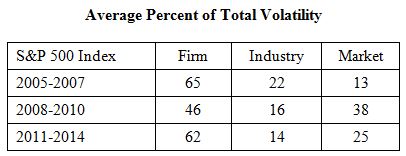

In their study, which covered the period January 2005 through December 2014, incorporating the years prior to, during and after the 2008 financial crisis, De and Nutman broke down the total volatility of stocks in the S&P 500 Index into three components: market, industry and firm (idiosyncratic risk). The authors then analyzed the trends in each component’s share over time.

Following is a summary of their findings:

- Total volatility increased by a factor of about four during the financial crisis, but at the time of their study was lower than it was precrisis.

- Idiosyncratic volatility remained the largest component (more than 60%) of total volatility for an equity investor. Over the decade preceding the study, it declined from about 70% in the late 1990s and dipped sharply during the crisis, but remained the major component.

- The share of market volatility increased by a factor of about four during the crisis to become the largest component. Much lower at the time of the study, it still remained about twice the prerecession average and higher than the long-term average.

- Sector volatility showed a consistent decrease over the period 2005 through 2014, becoming the smallest share of total volatility.

- Average pairwise stock correlation in the S&P 500 increased from an average of 16% from 2005 through 2007 to an average of 42% from 2008 through 2011. It then dropped back down to an average of 22% in the following three years. Thus, the pairwise correlations remained higher than they were precrisis, though they dropped by more than half since their peak in 2010.

- The power of the market model in explaining stock returns, as measured by the R-squared figure (a measure of how well the model explains performance), increased sharply from 22% precrisis to more than 50% in 2010, and then decreased and remained consistent at about 30%.

- There was a strong negative correlation between all components of volatility and contemporaneous GDP growth.

The following table provides the authors’ data on the three components of volatility for the precrisis, crisis and post-crisis periods.

De and Nutman explain: “The more stocks move in lockstep [correlations rise, as they did in the crisis period], the more the companies’ sector classifications, business models, financial status, capital structures and valuations get ignored, leading to greater stock mispricing, in turn creating stock picking opportunities [for astute stock pickers].”

They then state: “Idiosyncratic risk remains the largest share of total U.S. equity returns volatility, and the benefits of stock picking, though lower than pre-crisis levels, are at their highest since the financial crisis. These findings provide a strong justification for stock selection and active management.” The emphasis is mine.

Before examining their conclusion, note that the firms for which both work, TIAA and BlackRock, have actively managed offerings.

Accountability Ruins The Game

We’ll begin our analysis of the authors’ statements by noting that correlations of risky assets do tend to rise toward 1 during crises. Thus, the rise in correlations that we experienced during the financial crisis is neither unprecedented nor unexpected.

But isn’t it during crises (bear markets) that active management is supposed to protect investors? Investors might even be willing to accept below-benchmark returns overall if they experienced lower downside losses. The only problem is that there isn’t any evidence supporting that hypothesis.

Active Management In Bear Markets

In the Spring/Summer 2009 issue of its publication “Investment Perspectives,” Vanguard presented its findings from a study on the performance of active managers in bear markets. Defining a bear market as a loss of at least 10%, the study covered the period 1970 through 2008. The period included seven bear markets in the U.S. and six in Europe.

Once adjusting for risk (exposure to different asset classes), Vanguard reached the conclusion that “whether an active manager is operating in a bear market, a bull market that precedes or follows it, or across longer-term market cycles, the combination of cost, security selection, and market-timing proves a difficult hurdle to overcome.”

They also confirmed that “past success in overcoming this hurdle does not ensure future success.” Vanguard was able to reach this conclusion despite the fact that the data were biased in favor of active managers because it contained survivorship bias.

Now let’s turn to the issue of rising correlations, which has often been used as an excuse for active managers’ failure to outperform.

It’s About Dispersion, Not Correlations

Correlation shows the directional movement of stocks, not the magnitude of their movement. Magnitude is shown by the dispersion of returns (the size of differences in the returns of individual stocks or asset classes).

The greater the dispersion becomes, the greater the opportunity for active management to add value by overweighting the winners and avoiding the losers. Thus, it’s the dispersion of returns that we should examine, not the correlations, to determine how high the hurdle for active management is.

In its May 2012 paper “Dispersion! Not Correlation!” Vanguard showed that while correlations of stocks had increased, the dispersion of returns had remained stable. In each of the five calendar years from 2007 through 2011—which included bull, bear and flat markets—the degree of dispersion was such that at least two-thirds of all stocks either led or trailed the index by more than 10 percentage points—with the range being a low of 67% and a high of 79%.

Clearly, there was plenty of opportunity for active managers to add value. They just didn’t do it with any persistence, as the S&P Dow Jones SPIVA scorecard regularly demonstrates.

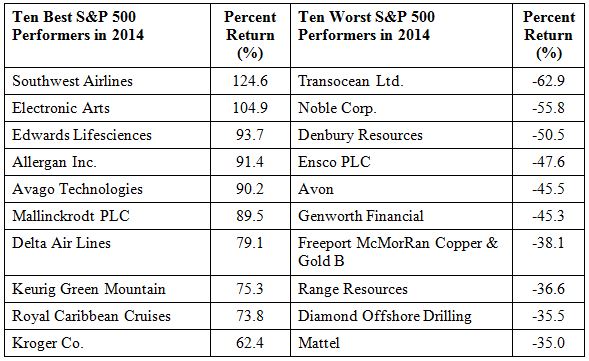

Now let’s look specifically at 2014, the last year that De and Nutman’s study examined. By 2014, the pairwise correlations had fallen to less than half the level it was during the peak of the crisis. In addition, there was plenty of dispersion of returns, as evidenced in the following table, which shows the 10 best and 10 worst performers in the S&P 500 Index in 2014.

Clearly, with correlations haven fallen sharply, and with the wide dispersion of returns seen above—demonstrating that there was a plethora of idiosyncratic risk—there was plenty of opportunity for active managers to generate alpha. As De and Nutman asserted, this type of environment provided “a strong justification for stock selection and active management.”

There’s only one problem. The evidence, as it always does, shows otherwise. The following data is from the 2014 S&P Dow Jones SPIVA scorecard:

- In 2014, 86.4% of large-cap funds underperformed the benchmark S&P 500 Index. Over the five- and 10-year periods, respectively, 88.7% and 82.1% of large-cap funds failed to deliver incremental returns over the benchmark.

- In 2014, 66.2% of midcap funds underperformed the benchmark S&P MidCap 400 Index. Over the five- and 10-year periods, respectively, 85.4% and 89.7% of midcap funds failed to deliver incremental returns over the benchmark.

- In 2014, 67.9% of small-cap funds underperformed the benchmark S&P SmallCap 600 Index. Over the five- and 10-year periods, respectively, 89.3% and 88.1% of funds failed to deliver incremental returns over the benchmark. This data exposes another myth—that active management wins in less informationally efficient markets, like the market for small-cap stocks.

- In 2014, 80.1% of active REIT funds underperformed the benchmark S&P US Real Estate Investment Trust Index. Over the five- and 10-year periods, respectively, 91.5% and 78.1% underperformed the benchmark.

Summary

De and Nutman try to provide a “story” for why active management will succeed. But like all fairy tales, it easily exposed by “pulling back the curtain” the fact that there really isn’t any all-and-powerful wizard behind it.

We have now experienced exactly the types of environments in which active managers are supposed to be “earning their stripes”—bear markets, periods of falling correlations and rising idiosyncratic risks—but active management has persistently failed to deliver on its promise.

While next year is always proclaimed to be a stock picker’s year, it never is. Making matters worse, as my co-author Andrew Berkin and I explain in our book, “The Incredible Shrinking Alpha,” the odds of active managers outperforming have been collapsing. Twenty years ago, about 20% of active managers were generating statistically significant alpha. Today that figure is about 2%.

As sure as the sun rises in the east, Wall Street will keep coming up with stories that attempt to justify the high costs of active management. Fortunately, those stories are easily exposed as nothing more than fairy tales. It’s too bad the financial media virtually never questions the claims of those proposing active management as the winning strategy.

Larry Swedroe is the director of research for The BAM Alliance, a community of more than 140 independent registered investment advisors throughout the country.