The Case For Mutual Fund-To-ETF Conversion: Flow Picture

Mutual fund conversions have become relatively mainstream in the last year or so, but has it been a profitable choice? John Hyland digs into the numbers and the shifting narrative in the mutual fund-to-ETF conversion conversation.

A major business strategy question for the roughly 75% of mutual fund family CEOs who have still not moved to offer their investment strategies in an ETF wrapper is how to make such a move. Mutual funds, particularly active equity funds, have been steadily bleeding assets via outflows for over fifteen years. Mostly to ETFs. Presumably the CEO will feel the need to do something to protect their remaining franchise.

They have three choices. The first is to offer ETFs as separate offerings from your mutual funds, something that issuers have been doing for over thirty years. The second, and newest, approach is to offer ETFs as a share class of your mutual fund. Much like Vanguard has been doing since their beginning and something that anybody can now do. The final approach is to convert your open-ended mutual fund into an ETF. This approach started five years ago in 2021.

Each of the three approaches has pluses and minuses. Doing them as separate class has the lowest odds of achieving needed scale and in any event can likely take years to get anywhere. The multiple share class approach has the greatest unknowns right now, both operational and from a distribution standpoint, and no sure signs it will work any better than the older approach.

However, if you are a $25 or $50 billion AUM mutual fund company, conversions will offer the fastest and surest way to achieve scale in the ETF space. If you convert half of your mutual funds, say ten or twenty with half your AUM, to ETFs you can go from zero AUM in ETFs to billions or tens of billions in ETFs. You are now a legitimate player in the space. Convert all your mutual funds and you could immediately be a major player! This would be true even if during to the conversion process, which requires a shareholder proxy vote, you saw additional outflows from your shareholders. Of course, you likely were already seeing outflows so how much is driven by the conversion process is hard to determine.

How the Flows Stack Up For Mutual Fund Conversions

In Fall of 2024, Bank of America/Merrill Lynch did a detailed study on the results of the initial batch of conversions, then approximately 120, to see what happened to flows and AUM. The data showed that the mutual funds in the years leading up to conversion generally saw outflows even if the fund outperformed its benchmark. After conversion the ETFs tend to see outflows slow and reverse themselves into inflows. This was true for both those ETFs that outperformed their benchmarks and those that did not. The turnup in flows typically took 6 plus months to really take hold.

The study was done fairly early in the process. There is now an additional year and a half plus worth of data and we are taking another look at the flows picture. Our thanks to our friends at FactSet for their help in this matter.

Over 200 funds have been converted to ETFs. These conversions were done by over 70 different mutual fund families. We are going to remove two categories of conversions. The first is conversions where the mutual fund’s AUM was so sub-scale that either as a mutual fund or an ETF it was not really a viable offering. We used $10 million in AUM at conversion as a cut-off although a large number of the removed funds actually had more like $1 million in AUM. Most of those have already closed. However, a few sub-scale conversions did grow AUM and very rapidly. In those cases, it seems the conversion was less about moving assets and more about just using the mutual funds to seed the ETF and then rapidly pour money into them. This is a somewhat different strategy.

The second is conversions where the fund pre-ETF was not actually a mutual fund (think Grayscale’s GBTC for example). These two adjustments bring the number of converted funds to under 200.

[One word of warning is that certain measurement results are skewed by the presence of a few major firms doing conversions on a massive scale. In particular Dimensional Fund Advisors and JP Morgan.]

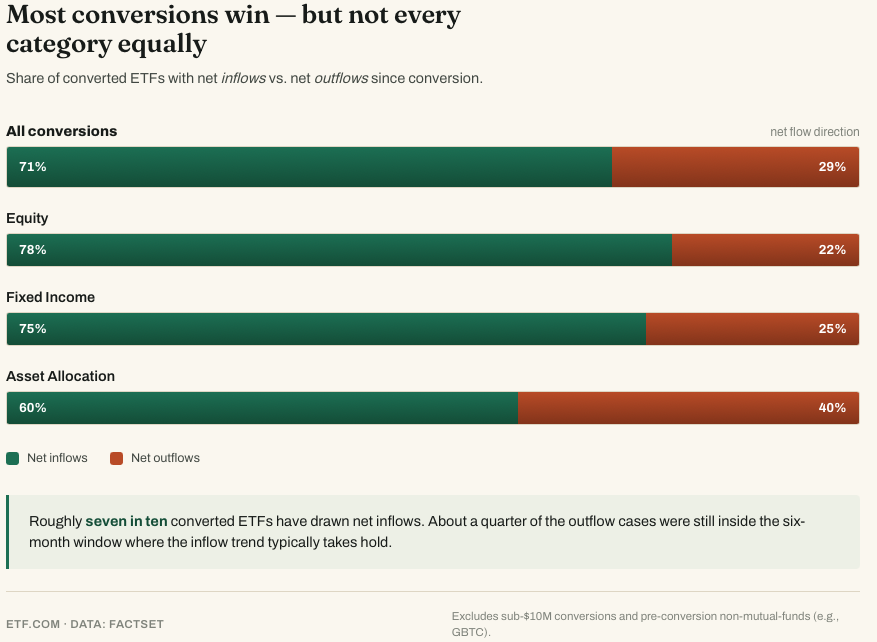

Looking just at flows post-conversion, approximately 71% of the ETFs have had net positive flows while 29% have had net outflows. And of those showing outflows, about a quarter were those still within the 6-month window since conversion, where Merrill Lynch’s study suggested that the inflow trend was still being established.

Looking at the two biggest asset categories, 78% of Equity ETFs had inflows while 75% of Fixed Income ETFs did as well. However, only 60% of Asset Allocation ETFs had inflows.

The total amount of inflows was approximately $120 billion while outflows were around $20 billion. Most of that inflow total belonged to DFA and JP Morgan who also heavily influenced the average figures. However, changing metrics, the median inflow was $125 million per ETF while the median outflow was only $23 million. Alternatively, the median ETF with inflows has seen flows equal to approximate 77% of their starting AUM at conversion while the losers only lost 18%.

Over 30 ETFs had inflows greater than 200% of their starting AUM, including eleven where the inflows were 1,000%+ of the starting AUM, while a dozen ETFs had outflows of between 50%-100%.

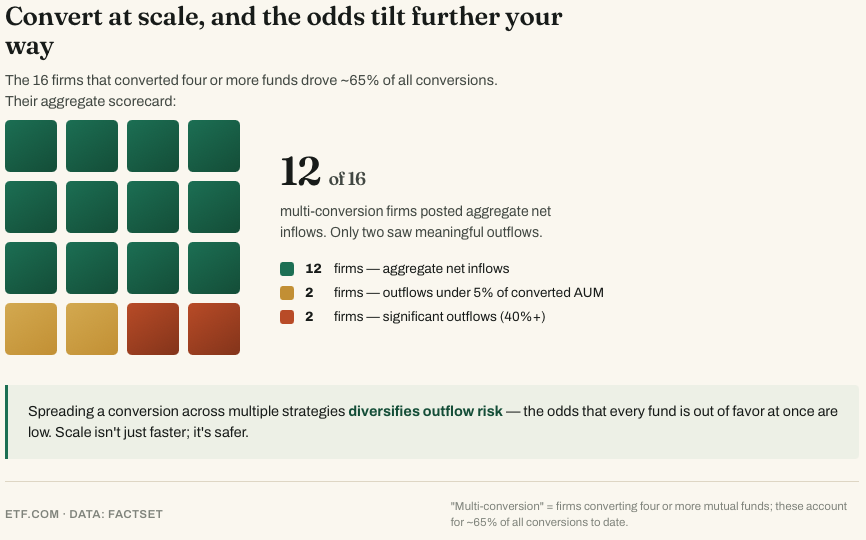

Finally, of the 70+ mutual fund issuers who did conversions, 16 have converted four or more mutual funds. These accounted for approximately 65% of all the conversions. Of the 16 firms 12 have had, in aggregate, inflows. Two had outflows equal to under 5% of their converted AUM. Two had significant outflows, 40%+, compared to the AUM converted.

The Odds Are in Your Favor

Viewing the figures above it suggests that for our hypothetical mutual fund CEO, the odds of succeeding with conversions are in your favor. Most conversions do see inflows and in some cases the flows as a percentage can be very large. Those that have outflows tend to see the losses as a much smaller percentage of their starting AUM. In any event some are likely seeing outflows not because they are now an ETF but because either their relative performance is poor or because their investment segment is out of favor. If they stayed mutual funds, they would still have those two factors and may have still experienced large scale outflows. Finally, converting multiple mutual funds, instead of just one or two, allows you to spread out your outflow risk by offering multiple strategies. Hopefully not all will be out of favor at the same time and so you avoid a concentrated outflow risk.

So, should our CEO do large scale conversions? The data would suggest yes, but there are three other factors to consider.

- The first is if your mutual funds are still bucking the odds and are receiving inflows. In that case you might put off this decision for now.

- The second is if your existing mutual fund has a large percentage of its AUM in 401(k) plans where moving the money might prove difficult. However, most mutual fund families do not have large amounts of 401(k) money.

- The third is that as a general rule you likely will offer the ETF at a lower total expense ratio than the mutual fund. Your gross revenue will go down assuming AUM remains the same. However, the cost of running ETFs can often be a lot cheaper than offering the mutual fund. You typically have much lower back office and record keeping costs. Plus, right now you are likely paying some amount on your mutual fund to the platforms like Charles Schwab or Fidelity. Often 25 basis points. If you have the same fund as an ETF on those platforms you may be paying more like 10-15 basis points. The focus should not be on the impact to your gross revenue as it should be the impact to your net.

Looking at the mutual fund CEO’s choice between the new multiple share class approach versus doing large scale conversions, we asked one of the ETF worlds most knowledgeable veterans, FactSet’s Elisabeth Kashner, their Director of Global Funds Research & Analytics, for her two cents.

“Actively managed equity mutual funds continue to bleed assets. It's quite reasonable to consider pivoting to ETFs rather than taking on the operational burdens of a dual share class structure. That said, a new wrapper can't save a failing strategy. The ETF market remains highly competitive. Moreover, asset managers have flooded into the market since the advent of the ETF Rule and the broadening of custom basket permissions to active products. Products need to compete in terms of pricing, performance, and distribution.”

What all this means is that it is likely that every mutual fund CEO should be getting out their pencils and seeing if conversion is smart thing for them to do. But what has changed from previous years is the way the question should be framed. It is no longer “Should I convert my mutual funds to ETFs? What are the reasons to do so?” The new question is “Should I convert my mutual funds to ETFs? What are the reasons to NOT do the conversion?” The burden of proof has switched sides.