Mexico’s Rally Has Nothing to Do With Oil

The country’s emergence as a major export platform is fueling its market’s growth.

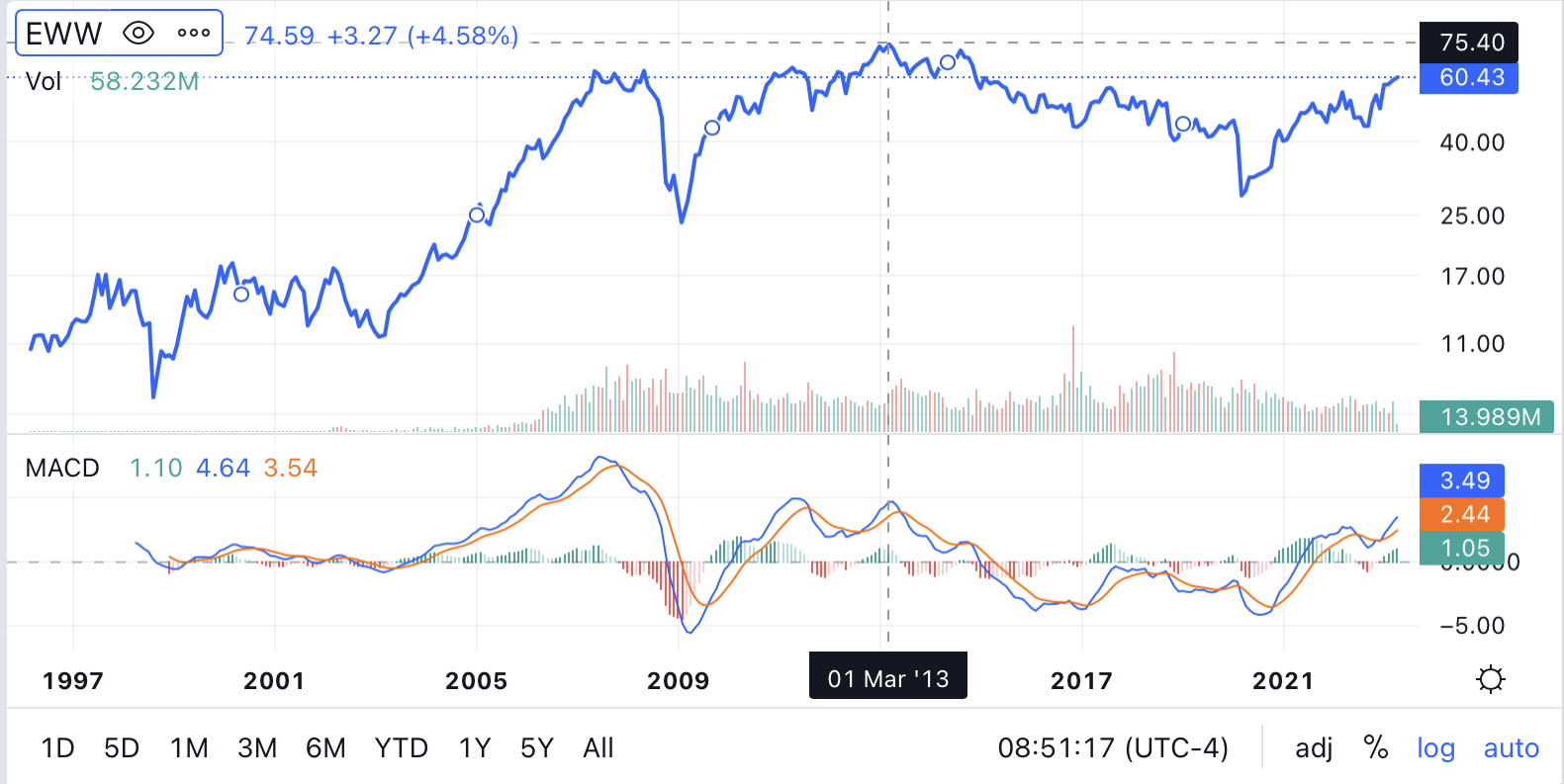

Mexico’s stock market is finally shaking off its lost decade: Up nearly 20% year to date, the iShares MSCI Mexico ETF (EWW) is enjoying a stealth rally that shows no signs of slowing down.

“Nearshoring” is the current buzzword within trade policy circles, and Mexico is experiencing it in spades. Foreign direct investment is pouring in. The industrial park occupancy rate clocked in at 97% last year, a record high, as international companies are feverishly relocating their supply chains.

The Mexican Stock Exchange last reached its peak in 2013, succumbing to a dramatic falloff in oil prices the following year, and then had several years of weak GDP growth. Even after the latest run-up, EWW—which tracks the Mexican IPC index—is just getting to where it was eight years ago.

Emerging Export Platform

Things are very different this time, however. The new rally has nothing to do with oil, but rather a realignment in world trade that is substantive and enduring.

Mexico is being positioned to be a major export platform, one that is even more highly integrated into the global automotive and tech supply chains than it ever has been. Though a pronounced U.S. recession and more structural issues like cartel crime or energy policy could muffle this, most analysts see the economic momentum continuing apace for the next five years.

In other words, we are in the early innings.

Foreign investment into Mexico was torrid in 2022, with the automotive sector absorbing nearly 44% of the recently leased industrial square footage. Just last month Tesla broke ground on a new factory in Monterrey with production expected as early as 2024, but it was Chinese companies that gobbled up 79.5% of the factory space available.

Last year, investors from China, Taiwan, Japan and South Korea moved 44 factories, production lines and distribution centers from Asia to relocate them in 16 industrial parks in Monterrey, Saltillo, Mexico City, Tijuana, Ciudad Juárez and Guadalajara.

The reasons for the shift to Mexico are clear: Multinational companies are seeking to mitigate the kind of supply chain issues and port bottlenecks they endured during the COVID-19 years. They are also more generally seeking to migrate production out of China. Though India and Vietnam are seeing factory relocations from the mainland, Mexico is even more compelling due to its wide-ranging trade agreements, linkages to the U.S. and comparative cost.

As a WTO member, with 13 free trade agreements that cover 50 countries, including the CPTPP and the USMCA, Mexico’s market is a now one of the most open worldwide. It can also take advantage of many aspects of USMCA and the Inflation Reduction Act.

The USMCA, a revision of NAFTA, encourages companies to recircuit supply chains to take advantage of duty-free access, making it possible for North America to compete with China. In addition, the Inflation Reduction Act and CHIPS Act also contains provisions leaning in favor of electric vehicles, batteries and semiconductors made with North American components.

The issue of labor costs is also illuminating. For decades, cheap Chinese labor trumped most of the advantages of moving manufacturing to Mexico. But because China’s “one child policy” was in place from 1979 to 2016, there are now far fewer young people entering its labor force.

Wages on the mainland—particularly in the coastal cities—are significantly up. According to a recent Bank of America report, since 2010, pay for the average Chinese factory worker has tripled to about $6 an hour, while in Mexico the cost has stagnated over the same time period, hovering little over $2 an hour.

All these factors explain the new focus on Mexico. The country’s manufacturing sector increased 6% in 2022 alone. Mexico’s largest bank, Grupo Financiero Banorte, reported that USMCA now accounts for 11.5% of its total loan book.

New construction is running at double the average rate of the past seven years. A central bank survey found that 16% of those companies with more than 100 employees reported they were seeing a direct and positive impact from nearshoring.

The evidence is showing up in the regional economies. In late October, the CEO of Banco del Bajío (BanBajio), a regional bank located within the central manufacturing states of Mexico, noted that nearshoring had recently grown the bank’s credit portfolio that year by $510 million, or about 5% of its portfolio.

Though the eighth largest in the country, this a bank that only finances local suppliers—Mexican companies in the industrial real estate sector—not the multinationals, so their loan growth is an example of a second-order, derivative effect.

ETF Exposure

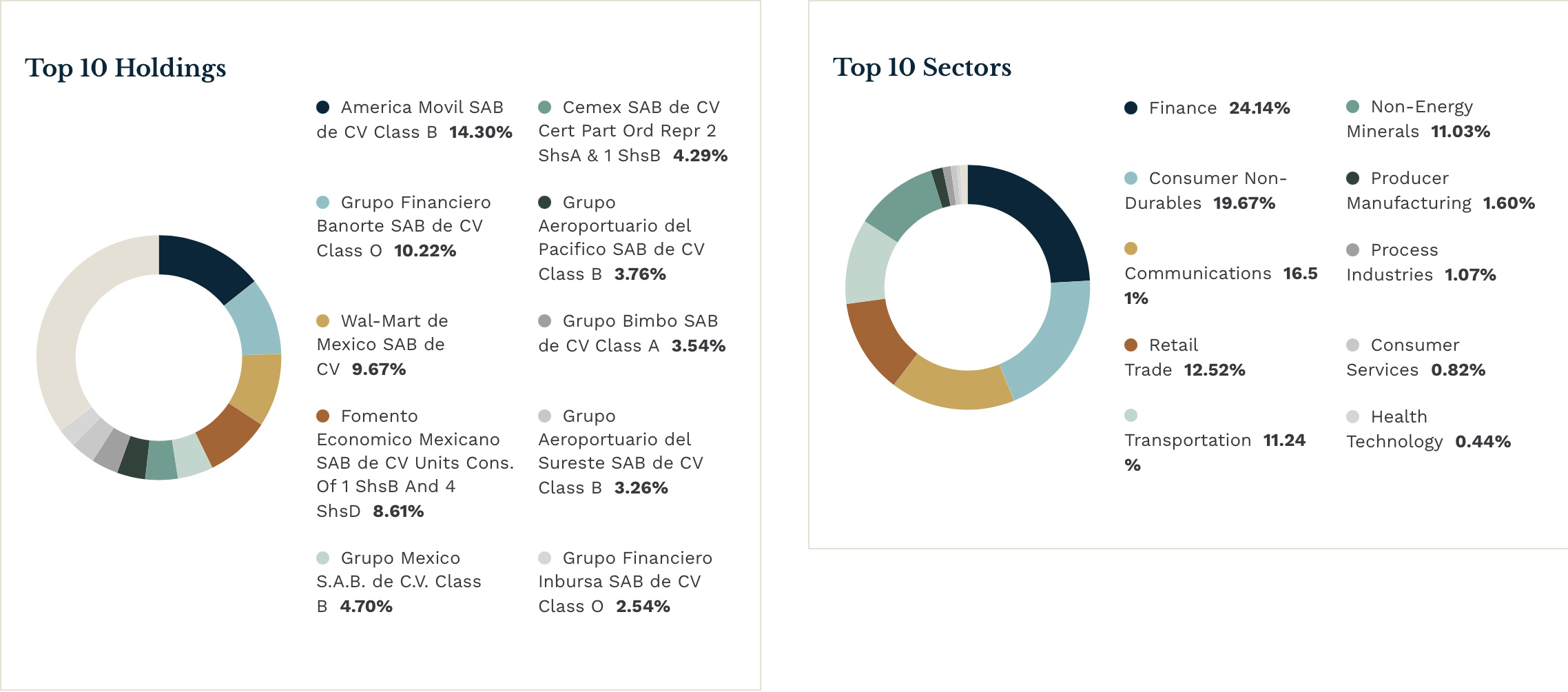

With an expense ratio of 0.50% and a semiannual dividend yield of 3.02%, EWW offers the best way to capture the nearshoring trend in Mexico. The ETF presently has 44 holdings, and though technically diversified across various industries (telecommunications, banking, retail, construction), it is heavily weighted to the nation’s largest companies.

America Movil SAB—the telecom behemoth–is 14% of the index; banking giant Banorte is 10.22%; Walmart of Mexico is 9.67%, Fomento Economico Mexicano SAB de CV Units Cons.—the bottler of Coca Cola and Heineken—is 8.61%.

All this foreign investment, construction, manufacturing and eventual spending power will be good for the Mexican stock market, and the large cap firms that make up a large part of the index.

With a P/E of 15.22, it is not egregiously expensive. Looking at one ratio—the current total market cap/(GDP + total assets of the central bank) ratio—Mexico at 29.64% is fairly or even undervalued.

In comparison, its last 10-year high was 38.71%, while its most recent 10-year low was 21.5%.

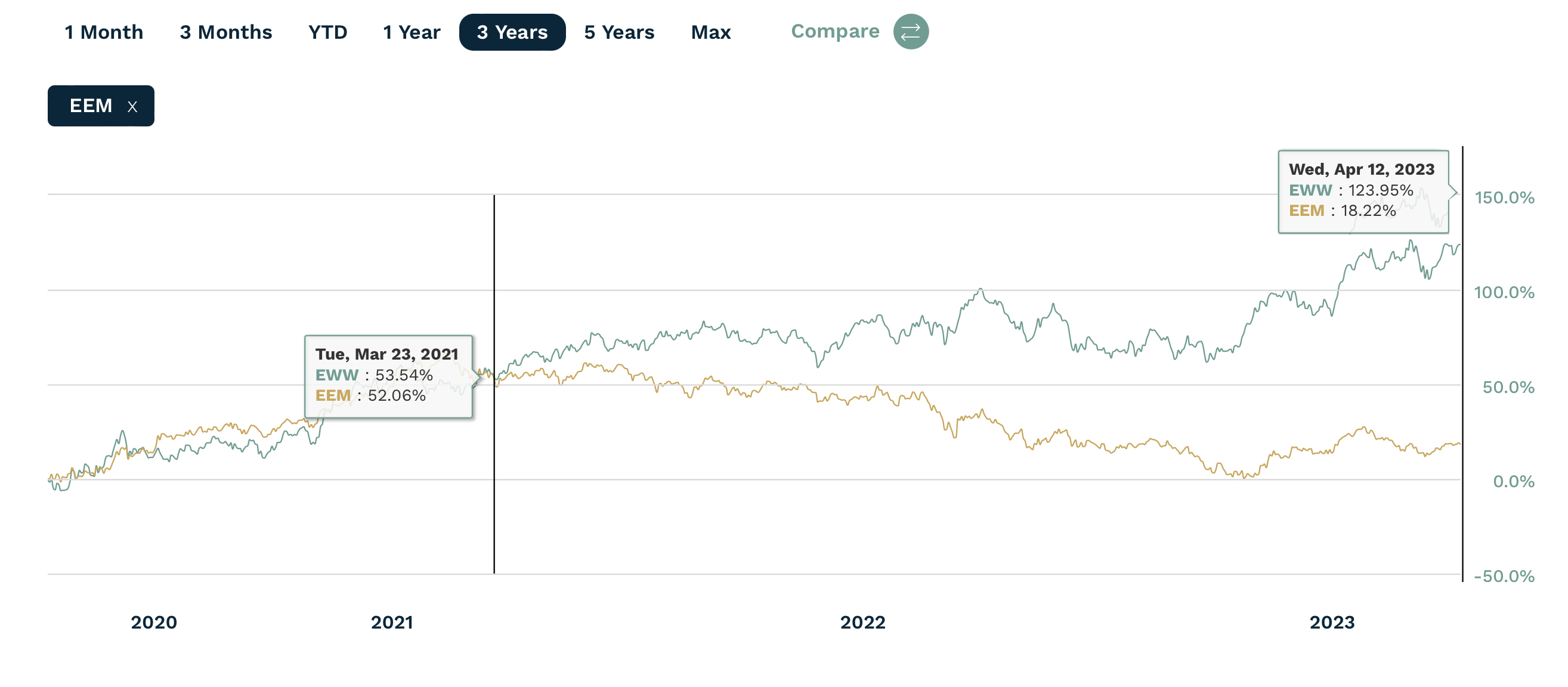

Another interesting distinction: Since March 2021, Mexico has made a decisive break from the broader emerging market ETF. Over a three-year period, EWW is up 123.95%, versus EEM’s 18.22% gain.

For the past 35 years, the bulk of wealth generated by global GDP growth gravitated to Asia, creating an enormous new middle class virtually from scratch.

Mexico might see a comparable development in the coming years, despite its well-known challenges. North American trade now ticks at $3 million a minute. Very small reversals in offshoring could have momentous impacts on the country.

One researcher has suggested that the even if Mexico were to attract just 1% of China’s gross leasable area of factory floor—a strong likelihood—it could result in Mexico needing to increase its GLA by 33%, requiring a $13 billion investment.

2023 is likely the year when Mexico—and EWW—trumps its oil curse and reaches new highs.