MicroStrategy Not A Bitcoin ETF Proxy

Nearly 100 hundred ETFs hold a company that is a poor proxy for physical bitcoin.

Earlier this week, MicroStrategy revealed that it had purchased $177 million worth of bitcoin—3,907 coins at an average price of $45,294—adding to its sizable stock of the cryptocurrency. The firm now owns 108,992 bitcoins, purchased at an average price of $26,769, and with a current market value of $5.1 billion (based on a price of ~$47,000 per bitcoin).

Shares of MicroStrategy are a major holding in several ETFs, and the stock has at least some weighting in 96 ETFs, according to the ETF.com Stock Finder tool.

The Bitwise Crypto Industry Innovators ETF (BITQ) holds the biggest position in the stock, with 13.6% of its portfolio allocated to the name. The Defiance Next Gen Big Data ETF (BIGY), the VanEck Vectors Digital Transformation ETF (DAPP) and the Amplify Transformation Data Sharing ETF (BLOK) are also large holders of MicroStrategy, with weightings of 5-7% in the stock.

MicroStrategy’s bold bets on bitcoin have earned it accolades from many in the cryptocurrency community, but how should investors feel about finding this stock in their ETF?

The First Mover

MicroStrategy’s latest bitcoin purchases hardly raised an eyebrow; however, the company made waves last year when it became the first publicly traded company to purchase bitcoin—a surprising move that was followed by Tesla, Square, MercadoLibre and other public companies.

MicroStrategy’s first purchase, made on Aug. 11, 2020, was made at a bitcoin price of around $11,650. Since then, the company has gone on to add to its bitcoin holdings multiple times, even going as far as to borrow $2.2 billion to fund its acquisitions.

Michael Saylor, founder and CEO of MicroStrategy, has been a staunch proponent of bitcoin. He’s called the cryptocurrency “a moral, economic, and philosophical imperative,” and likened buying bitcoin today to buying Facebook or Amazon in their early days.

Saylor has also expressed his belief that holding bitcoin on MicroStrategy’s balance sheet is superior to holding cash.

He said: “We find the global acceptance, brand recognition, ecosystem vitality, network dominance, architectural resilience, technical utility, and community ethos of bitcoin to be persuasive evidence of its superiority as an asset class for those seeking a long-term store of value. Bitcoin is digital gold – harder, stronger, faster, and smarter than any money that has preceded it.”

“MicroStrategy has recognized Bitcoin as a legitimate investment asset that can be superior to cash and accordingly has made Bitcoin the principal holding in its treasury reserve strategy,” Saylor added.

Major Pivot

With more than $5 billion of bitcoin on its balance sheet, MicroStrategy (MSTR) has become inextricably tied to the cryptocurrency. It’s an amazing turn of events for a company whose primary business is (or used to be) selling business intelligence software.

Founded in 1989 and publicly traded since 1998, MicroStrategy offers companies software for analyzing and visualizing their data. Shares of the company peaked in 2000 during the dot-com boom, fell precipitously and then found equilibrium over the next several years.

But the company’s core business hasn’t seen much growth over these past two decades. Revenues have only grown at a 4% annual rate over the past 20 years, and have been flat over the past 10 years. MicroStrategy’s stock was similarly flat over those periods.

That all changed when the company got into the bitcoin game last year. Suddenly, the firm was a big holder of one of the most coveted assets in the world. After MicroStrategy’s first bitcoin purchase last August, prices for the cryptocurrency rose more than fivefold over the next seven months.

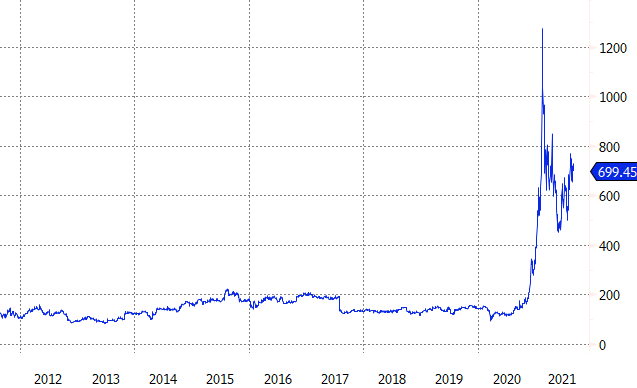

The value of the company’s bitcoin holdings ballooned, and so too did the stock price. After years of stagnation, MSTR surged, rising from $135/share on the day of the company’s first bitcoin purchase last August to as high as $1,315 in February of this year—a nearly tenfold increase.

Currently, with bitcoin off its highs, MicroStrategy stock has also fallen back to last trade around $700, but that’s still far above where it was trading before it got into bitcoin.

MicroStrategy Stock Price

Bitcoin Proxy

With its big treasure trove of bitcoin, MicroStrategy has essentially become a proxy for the cryptocurrency, with all the risks and opportunities that entails.

Prior to buying bitcoin, the company had an enterprise value of less than $900 million. Today its enterprise value is $9.2 billion—including $2.2 billion of debt and an equity market capitalization of $7 billion. The company’s bitcoin holdings being worth $5.1 billion implies a market value of a little less than $2 billion for MicroStrategy’s software business.

In other words, the vast majority of MicroStrategy’s stock price is now tied to bitcoin; the software business is secondary.

Not A Software Stock

Anyone who owned MSTR prior to its pivot into bitcoin has done quite well. There is little doubt that without bitcoin, MicroStrategy stock would be trading much lower than it is.

On the other hand, this is no longer the stock of a software company. This is the stock of a bitcoin holding company that also happens to have a software business on the side.

As can be seen from the chart below, movements in MSTR are closely linked to movements in bitcoin prices:

1-Year Returns For MSTR (Blue) & Bitcoin (Yellow)

With MicroStrategy adding to its bitcoin holdings this week, it’s clear that the company has no plans to unlink itself from bitcoin; quite the contrary, it’s tying itself closer to the cryptocurrency.

If bitcoin continues to rise, that likely bodes well for MSTR. On the other hand, if bitcoin were to fall, it would be a blow to the stock.

On the downside, risks may be exacerbated by the significant amount of debt MicroStrategy has taken on to fund its bitcoin purchases. About $1.7 billion of the company’s debt is in the form of convertible notes, which may be swapped for equity if MSTR share prices are high enough. The other $500 million is in the form of senior secured notes.

If MicroStrategy is unable to refinance or pay off its debt when it comes due, it may be in trouble. Even under more benign scenarios, investors in the stock could face dilution and/or the company could be forced to liquidate some of its bitcoin holdings.

S&P Global Ratings, which has a junk-level CCC+ issuer credit rating on MicroStrategy, warned that the firm could face difficulty addressing its debt if bitcoin prices fell low enough.

Leverage Juiced Returns

Without the ability to buy a bitcoin ETF on U.S. exchanges, some investors have used MicroStrategy to get their cryptocurrency exposure.

Since announcing its bitcoin purchases, shares of MicroStrategy have outperformed the cryptocurrency itself, rising 420% versus 318%. Year-to-date, it’s a similar story, with a gain of 81% for MSTR versus 62% for bitcoin.

The difference may be in part attributed to enthusiasm about MicroStrategy’s foray into bitcoin, which has lifted the company’s valuation multiple. The company’s CEO is a popular figure on Twitter, and the retail-driven meme stock phenomenon may have benefited MSTR to some extent.

But the more decisive factor in MSTR’s outperformance may be the firm’s generous use of debt to purchase bitcoins and juice its returns. Thanks to its debt-fueled purchases, MSTR has earned $2.2 billion of paper profits on its bitcoin—a significant sum for a company whose total enterprise value was less than $900 million a year ago.

Of course, as discussed above, that leverage cuts both ways, and if bitcoin were to fall, MicroStrategy share prices would likely fall even more. And with little room for the company to leverage up further, new investors in the stock probably wouldn’t benefit to the same degree past investors have, even if bitcoin continues to rise.

No Guarantee

It’s also worth noting that even if bitcoin were to rally, there is no ability to predict how much MSTR would rally or if it would follow suit at all. As is the case with closed-end funds and similar products like the Grayscale Bitcoin Trust (GBTC), market value doesn’t always track net asset value.

There is no arbitrage mechanism to ensure MSTR’s share price stays in line with the value of the bitcoin on its balance sheet (not to mention, the value of the company’s software business could fluctuate as well).

For this reason, MSTR may not be the best proxy for bitcoin, and it will likely have a tougher time tracking bitcoin than something like GBTC, let alone a bitcoin ETF, were there one available.

Email Sumit Roy at [email protected] or follow him on Twitter @sumitroy2